Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Getting the loan wrong on a fix and flip deal can slow your closing, trigger underwriting conditions you did not plan for, or cause you to lose the property before renovation even starts.

Fix and flip loans do not work like conventional mortgages. At Ziffy, we are not mainly qualifying you through W-2 income, personal tax returns, or debt-to-income ratio. We are looking at the deal itself: the purchase price, renovation scope, after-repair value, timeline, borrower liquidity, and exit strategy.

That changes how borrowers should prepare. Instead of leading with income documents, the file needs to prove that the purchase price, rehab budget, ARV (After-Repair Value), and exit plan hold together. A high credit score will not make an inflated ARV work. What moves the file forward is more practical: sold comps that support the value, a contractor bid that matches the scope, and enough cash to handle the project while draws are processed.

This guide explains the fix and flip loan requirements investors should understand in 2026, including credit score, down payment, LTC (Loan-to-Cost), ARV, rehab draws, experience, documentation, property eligibility, cash reserves, and common mistakes that delay approval.

For a broader overview of how the loan works from application to payoff, start with Ziffy’s Fix and Flip Loan Guide.

Table of Contents

Fix and Flip Loan Requirements at a Glance

As of May 2026, Ziffy’s fix and flip loan program is designed for non-owner-occupied investment properties where the borrower plans to buy, renovate, and either sell or refinance the property after improvements are complete.

Requirement | Ziffy’s 2026 Terms | What It Means |

|---|---|---|

Minimum credit score | 650 | Higher scores may improve pricing and leverage options |

Down payment | 25% to 30% | First-time flippers usually need stronger equity |

Loan-to-cost | Up to 92% | Based on total project cost, including purchase and renovation |

ARV cap | Up to 75% | The total loan cannot exceed 75% of after-repair value |

Rehab cost coverage | Up to 100% | Subject to LTC, ARV, and draw approval |

Loan amount | $100,000 to $5 million | For eligible non-owner-occupied investment properties |

Loan term | 6 to 24 months | Built for short-term acquisition, renovation, and exit |

Prior flip experience | Not required | Strong documentation matters more for first-time flippers |

Approval timeline | Within 15 days | Available when documentation is complete at submission |

Underwriting looks at these requirements together. A 650 credit score does not automatically disqualify a deal, but it can affect pricing, leverage, and how closely the file is reviewed. A 25% down payment may be available, but only when the property, borrower, and ARV (After-Repair Value) support it. The cleanest files usually arrive with the purchase contract, contractor bid, ARV support, borrower liquidity, and exit plan already lined up.

Credit Score Requirements for a Fix and Flip Loan

The minimum credit score for a fix and flip loan at Ziffy is 650.

That threshold is lower than many conventional investment property loans because fix and flip financing is asset-based. Credit still matters because it tells underwriting how the borrower has handled debt in the past. But the loan decision is not driven by personal income in the same way a conventional mortgage is.

Here is how credit score usually affects the file:

Requirement | Ziffy’s 2026 Terms |

|---|---|

650 to 679 | Eligible, but the renovation plan, exit strategy, and ARV support need to be especially clear |

680 to 719 | Standard qualification range with stronger access to normal leverage and pricing |

720+ | Stronger position for pricing, leverage, and overall file strength |

Based on hundreds of fix and flip loans closed by Ziffy till date, the strongest files were not always the highest-credit-score borrowers. The files that moved fastest usually had the basics ready before submission: sold comps for the ARV, a line-item contractor bid, and enough liquidity to cover carrying costs while draws were pending.

First-time borrowers often spend too much time worrying about the credit score and not enough time tightening the deal package. A 720 score does not fix an inflated ARV or vague rehab scope. A 655 score can still work when the property has a strong spread, the contractor bid is detailed, and the exit plan is realistic.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

Down Payment Requirements for Fix and Flip Loans

Fix and flip loans at Ziffy usually require 25% down. That down payment is only one part of the cash requirement. Underwriting also looks at whether the borrower has enough money to close, start the rehab, cover carrying costs, and stay inside the LTC (Loan-to-Cost) and ARV limits. Ziffy can finance up to 100% of verified renovation costs when the deal fits within the total leverage limits, but the loan still has to stay within both the LTC limit and the ARV cap.

Before applying, run the numbers through Ziffy’s Fix & Flip Calculator so you can test the purchase price, rehab budget, ARV, financing costs, and projected profit in one place.

In our experience, most first-time fix and flip borrowers do not underestimate the down payment itself. They underestimate the full cash required after closing, including interest payments, insurance, taxes, contractor deposits, materials timing, and the gap between completed work and rehab draw releases.

Whether the down payment is closer to 25% or 30% usually comes down to credit, deal margin, and experience.

1. Credit score

Borrowers closer to the 650 minimum should plan for stronger equity. A score in the 700s can support better terms, assuming the deal itself also works.

2. Deal margin

A wider spread between total cost and ARV gives underwriting more room to get comfortable with the deal. If the ARV is tight, the down payment requirement can move higher because the lender has less room if costs increase or the sale price comes in lower than expected.

3. Investor experience

First-time flippers should usually expect 30% down. Experienced investors with documented completed flips may qualify closer to 25%, especially when the property has clean valuation support and the renovation budget is well documented.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

“For first-time flippers, I usually tell borrowers to plan around 30% down rather than building the deal around the most aggressive leverage available. That extra equity can make the file cleaner, reduce back-and-forth, and show the underwriter that the borrower has enough room to handle normal project surprises.”

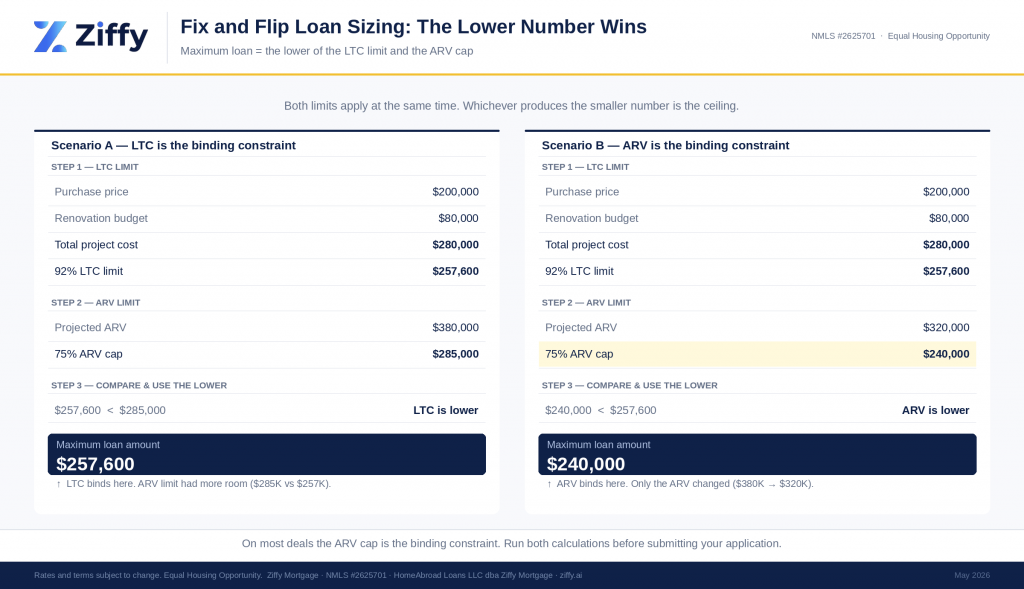

How LTC and ARV Control Your Maximum Loan Amount

Fix and flip loan sizing is governed by two limits at the same time:

- Loan-to-cost, or LTC

- After-repair value, or ARV

Both limits apply at the same time, and the lower number controls the maximum loan amount.

– LTC: Up to 92% of Total Project Cost

Loan-to-cost compares the loan amount to your total project cost.

Total project cost = purchase price + renovation budget

If a deal has a $200,000 purchase price and an $80,000 renovation budget, the total project cost is $280,000. At 92% LTC, the maximum loan supported by cost would be:

- $280,000 × 92% = $257,600

That means the investor would need to bring at least $22,400 before accounting for closing costs, interest, reserves, or any other required contributions.

– ARV Cap: Up to 75% of After-Repair Value

The ARV cap compares the loan amount to the property’s expected value after renovation. If the same property has a projected ARV of $380,000, the ARV-based maximum loan would be:

- $380,000 × 75% = $285,000

In this example, the 92% LTC limit is lower than the ARV cap, so LTC is the binding constraint. The loan would be capped at $257,600, not $285,000.

The result changes if the ARV comes in lower. If the projected ARV is $320,000 instead of $380,000, the ARV-based maximum loan becomes:

- $320,000 × 75% = $240,000

Now the ARV cap is lower than the LTC limit, so ARV becomes the binding constraint.

Deal Input | Stronger ARV Example | Tighter ARV Example |

|---|---|---|

Purchase price | $200,000 | $200,000 |

Renovation budget | $80,000 | $80,000 |

Total project cost | $280,000 | $280,000 |

92% LTC limit | $257,600 | $257,600 |

Projected ARV | $380,000 | $320,000 |

75% ARV cap | $285,000 | $240,000 |

Maximum loan amount | $257,600 | $240,000 |

Binding constraint | LTC | ARV |

This is where many fix and flip budgets break down. The maximum loan amount is not whichever number looks best. It is the lower of the allowed LTC amount and the allowed ARV amount.

For a deeper breakdown of valuation math, read Ziffy’s guide to ARV in real estate.

Example From a Ziffy Fix and Flip File

A recent Ziffy fix and flip scenario involved a borrower purchasing a non-owner-occupied investment property for $200,000 with a planned renovation budget of $80,000 and a projected ARV of $380,000. The file moved cleanly because the borrower submitted a detailed scope of work, contractor bid, and comparable sold properties that supported the ARV. The final loan structure stayed within both Ziffy’s LTC and ARV limits, which made the approval path much clearer.

Deal Input | Amount |

|---|---|

Purchase price | $200,000 |

Renovation budget | $80,000 |

Total project cost | $280,000 |

Projected ARV | $380,000 |

92% LTC limit | $257,600 |

75% ARV cap | $285,000 |

Maximum loan amount | $257,600 |

Binding constraint | LTC |

The takeaway: underwriting does not need a perfect project. It needs numbers that can be verified. When the ARV, scope, and exit strategy all point in the same direction, underwriting has fewer open questions to resolve.

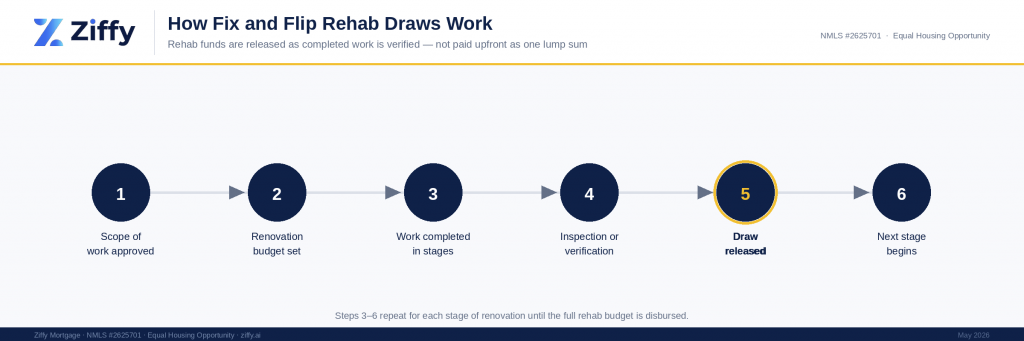

Rehab Cost Coverage and Draw Requirements

Ziffy can finance up to 100% of verified renovation costs when the deal stays within the approved leverage structure. That does not mean the full renovation budget is handed over at closing. Rehab funds are released through draws as work is completed and verified. That draw structure keeps the loan tied to completed work instead of releasing the full rehab budget before the project begins.

A typical rehab draw process includes:

- A line-item scope of work before closing

- Contractor bid review

- Approved renovation budget

- Work completed in stages

- Inspection or verification

- Draw release after completed work is approved

You need enough liquidity to manage timing gaps. Contractors may ask for deposits. Materials may need to be purchased before a draw is released. Inspections can take time. Even when the loan covers the rehab budget, you should not assume the project will require zero cash management after closing.

Draw timing matters more than new investors expect. Even if rehab funds are approved, the borrower may still need cash upfront for deposits, materials, and work completed before the next draw is released. A profitable flip can still become stressful if you underbudget working capital.

Experience Requirements: Can First-Time Flippers Qualify?

Yes. Ziffy does not require prior flipping experience. Where some private lenders want to see one to three completed flips before approving a borrower, we do not treat lack of experience as an automatic blocker. But first-time flippers need to make the deal easier to underwrite.

A first-time flipper should expect to provide:

- A line-item renovation budget

- A licensed contractor bid

- Contractor background or project history

- Comparable sold properties supporting ARV

- A realistic timeline

- A clear exit strategy

- Enough liquidity for carrying costs and project gaps

Experience helps, but a first-time flipper can still reduce underwriting friction by showing who is doing the work, what it will cost, how long it will take, and how the property will exit. If you have not completed a flip before, the underwriter needs confidence that the project can still be completed on time and on budget.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

If you are still learning the execution side of the strategy, read Ziffy’s guide on how to flip a house before submitting your first deal.

Documentation Required for a Fix and Flip Loan

A clean fix and flip file starts with complete documentation. Missing documents do not just delay approval. They can also change how the underwriter views the risk of the project.

You should be ready with:

- Purchase contract

- Property address and basic property details

- Scope of work

- Contractor bid

- Renovation timeline

- ARV support with comparable sales

- Borrower credit authorization

- Entity documents, if purchasing through an LLC

- Liquidity documentation

- Exit strategy

In our experience, incomplete contractor bids are one of the most common causes of underwriting delays. The bid does not need to be fancy, but it does need to be specific enough for the underwriter to understand what work is being done, what it costs, and who is responsible for completing it.

The renovation plan is usually the biggest documentation issue. “Kitchen and bathroom updates” is not enough. Underwriting needs the actual scope: cabinets, countertops, flooring, plumbing, electrical, roof, HVAC, fixtures, permits, labor, materials, and contingency. A detailed scope cuts down the back-and-forth because underwriting can see exactly how the rehab budget was built.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

Exit Strategy Requirements

Fix and flip loans are short-term loans. The lender needs to see how the loan will be paid off before the loan is approved. There are two common exit strategies.

Exit 1: Sell the Property After Renovation

This is the standard fix and flip exit. Your ARV should be supported by comparable sold properties, not only active listings or automated online estimates.

The best comps are:

- Recently sold

- Close to the subject property

- Similar in size and layout

- Similar in bedroom and bathroom count

- Similar to the expected post-renovation condition

A listing plan also helps. If you know the target resale price, likely buyer profile, estimated days on market, and agent strategy, the file is stronger.

Exit 2: Refinance Into a DSCR Loan

Some investors use a fix and flip loan to acquire and renovate the property, then refinance into a rental loan and hold it.

This can work when the renovated property qualifies based on rental income. If that is your plan, review Ziffy’s DSCR Loan Requirements before relying on this exit. The property needs to support the new loan after renovation.

In our experience, the strongest exit plans are built before the loan is submitted, not after the renovation is complete. A borrower planning to sell should know the resale comps. A borrower planning to refinance into DSCR should already know whether the expected rent can support the next loan.

A fix-and-flip-to-DSCR strategy is strongest when you model both loans before closing on the acquisition. Do not wait until the renovation is finished to find out whether the rental numbers support the refinance.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

Property Requirements

Fix and flip loans are for non-owner-occupied investment properties. Standard eligible properties include:

- Single-family residences

- 2 to 4 unit residential properties

- Eligible townhomes

- Eligible condos, when the project and property meet requirements

Property condition affects how deeply the file gets reviewed. Cosmetic rehabs are easier to underwrite than projects with structural issues, environmental concerns, unresolved title problems, or unclear permits.

Heavy rehab can work, but the file needs more support: a detailed scope, realistic timeline, experienced contractor, permit plan, and ARV that still leaves enough room after renovation. If the project includes foundation work, major structural repairs, fire damage restoration, or full system replacement, expect a deeper review.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Cash Reserve Expectations

Fix and flip loans do not work exactly like DSCR loans when it comes to reserves, but liquidity still matters. We like to see enough cash to handle:

- Interest payments

- Property taxes

- Insurance

- Utility costs

- Contractor deposits

- Materials timing

- Permit delays

- Inspection and draw gaps

- Cost overruns

A practical target is 2 to 6 months of carrying costs, plus a renovation contingency. That liquidity can be the difference between a project that keeps moving and a project that stalls because the next draw has not been released yet.

Higher leverage can help at closing, but it gives the borrower less room if the project runs long. If the project runs 60 days longer than expected, the investor still has to cover carrying costs, utilities, taxes, insurance, and any timing gaps in the draw process.

For a broader explanation of how reserves affect investor loan files, read Ziffy’s guide on cash reserves for investment property loans.

Common Mistakes That Delay or Sink Fix and Flip Applications

Mistake 1: Using Online Estimates as ARV

Online estimates can be useful for a quick screen, but they are not enough for underwriting. The ARV needs to be supported by comparable sold properties.

Many first-time files start with an online estimate as the resale target. That creates problems when the appraisal relies on actual sold comps instead. Build your ARV the way an appraiser would: recent sold comps, similar property type, similar condition, and close location.

Mistake 2: Submitting a Vague Contractor Bid

A vague bid creates underwriting friction.

A bid that only says “Renovate kitchen and bathrooms: $45,000” usually creates more questions than answers. A better bid breaks the work into actual line items: cabinets, countertops, flooring, plumbing fixtures, electrical updates, labor, materials, permits, and contingency.

“Kitchen cabinets, quartz countertops, tile backsplash, appliance installation, two bathroom vanities, tub surround, LVP flooring, interior paint, electrical fixture replacement, plumbing fixture replacement, labor, materials, permits, and contingency.”

A clear bid makes the project easier to approve because it shows exactly where the money is going.

Mistake 3: Forgetting Carrying Costs

Purchase price and rehab budget are not the whole deal. You also need to model:

- Loan interest

- Taxes

- Insurance

- Utilities

- Maintenance

- HOA dues, if applicable

- Selling costs

- Closing costs

- Contingency

A deal that looks profitable before financing and carrying costs may look much thinner after the full hold period is modeled.

Mistake 4: Overestimating the Exit Price

The resale price should be based on evidence, not optimism. If every profit assumption depends on selling above the strongest comp in the neighborhood, the deal is fragile. That kind of aggressive resale assumption usually shows up during appraisal review, underwriting, or the listing process.

Mistake 5: Applying Before the File Is Ready

Speed matters, but a rushed file usually closes slower.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Fix and Flip Loan vs Bridge Loan vs DSCR Loan

Fix and flip loans are not the only investment property financing option. The loan choice should match what is actually happening with the property. A full rehab needs different financing than a quick acquisition or a stabilized rental refinance.

Loan Type | Best Use Case | Key Underwriting Focus |

|---|---|---|

Fix and flip loan | Buy, renovate, and sell | ARV, rehab budget, scope of work, exit strategy |

Bridge loan | Short-term acquisition or transition financing | Property value, equity, exit plan |

DSCR loan | Buy or refinance a rental property | Rental income, PITIA, DSCR ratio |

- Use a fix and flip loan when the plan is to buy, renovate, and repay the loan through a sale or refinance after improvements are complete.

- A bridge loan may fit better when you need short-term capital but the property does not require a major rehab draw structure.

- A DSCR loan is the better long-term rental financing option once the property is stabilized and producing enough rent to support the loan.

You can also compare investor loan structures in Ziffy’s guides to hard money vs DSCR loans and investment property loans.

Next Steps

The main qualification question is not complicated: does the deal support the loan request?

At Ziffy, the core requirements are a 650+ credit score, 25% down, a loan structure that fits within up to 92% LTC and up to 75% ARV, a credible renovation plan, and a clear exit strategy.

Before submitting a file, test the purchase price, rehab budget, ARV, financing costs, and exit plan in Ziffy’s Fix & Flip Calculator. Use Ziffy’s Fix & Flip Calculator to test the purchase price, renovation budget, ARV, financing costs, and projected profit. If the numbers work, get pre-approved for a fix and flip loan with Ziffy Mortgage. No W-2s. No personal tax returns. Approval within 15 days when documentation is complete.

FAQs

What credit score do I need for a fix and flip loan?

Ziffy requires a minimum credit score of 650 for fix and flip loans. Higher scores can support better pricing and stronger leverage, but approval still depends heavily on the property, ARV, renovation plan, and exit strategy.

How much down payment do I need for a fix and flip loan?

Most Ziffy fix and flip loans require 25% down. First-time flippers should usually plan for the higher end. Experienced investors with strong credit, clean documentation, and a well-supported ARV may qualify closer to 25%.

Does Ziffy require prior flipping experience?

No. First-time flippers can qualify. Without prior flip experience, the file needs stronger documentation, including a detailed scope of work, licensed contractor bid, comparable sales, and a clear exit plan.

Can renovation costs be included in the loan?

Yes. Ziffy can finance up to 100% of verified renovation costs when the deal stays within the approved LTC and ARV limits. Rehab funds are usually released through draws as completed work is verified.

What is the difference between LTC and ARV?

LTC measures the loan against total project cost, including purchase price and renovation budget. ARV measures the loan against the property’s projected value after renovation. Both limits apply, and the maximum loan amount is based on the lower allowable number.

Can I refinance a fix and flip loan into a DSCR loan?

Yes, if the renovated property qualifies as a rental based on DSCR requirements. This works best when you model the DSCR exit before buying the property, not after the renovation is complete.

How fast can Ziffy approve a fix and flip loan?

Ziffy can approve fix and flip loans within 15 days when the file is complete at submission. The most common delays come from incomplete contractor bids, appraisal issues, missing documents, or unsupported ARV assumptions.

What property types are eligible?

Eligible properties generally include non-owner-occupied single-family residences, townhomes, eligible condos, and 2 to 4 unit residential properties. Properties with structural, title, environmental, or permit issues may require additional review.