Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Quick Answer: Hard Money vs. DSCR Loan

Hard money loans are for short-term deals that need to close fast, including flips, auctions, and distressed properties. DSCR loans are for long-term holds where the property’s rental income supports the financing. The right choice depends on your exit strategy, not just your timeline.

Choose a hard money loan if the property needs repairs, the seller needs a fast close, or your plan is to renovate and sell or refinance within 6 to 24 months. Choose a DSCR loan if the property is rent-ready, the numbers work as a long-term rental, and you want financing based on property income instead of personal income documents.

At Ziffy Mortgage, we finance investor deals across DSCR loans, bridge loans, fix and flip loans, and other investment property loans. The goal is not to force every property into one product. The goal is to match the loan to the property’s condition, cash flow, closing timeline, and exit plan.

As of May 2026, eligible DSCR purchase files at Ziffy may qualify for up to 85% LTV, which can bring the minimum down payment to 15%. Most DSCR files still close on a more standard mortgage timeline, usually around 21 to 30 days. Fix-and-flip financing is built for a different moment in the deal cycle: faster acquisition, short-term ownership, and properties that still need work before they can support permanent financing.

A lot of investors eventually use both. Hard money can fund the acquisition and rehab. A DSCR loan can replace it once the property is stabilized and rented. That is especially common in the BRRRR method, where the financing strategy changes as the property changes.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

Table of Contents

Hard Money vs. DSCR Loan: Side-by-Side Comparison

Feature | Hard Money Loan | DSCR Loan |

|---|---|---|

Loan purpose | Short-term acquisition, rehab, or flip | Long-term rental hold |

Typical term | 6 to 24 months | 30 years, fixed or ARM options |

Typical pricing | Higher short-term rates and points because speed and property risk are priced in | Long-term investor-loan pricing based on credit, leverage, DSCR, property type, and market conditions |

Qualification basis | Property value, after-repair value, rehab scope, and exit plan | Property rental income and DSCR ratio |

Income verification | None or minimal, depending on lender | No W-2s, pay stubs, tax returns, or DTI checks on the core DSCR path |

Down payment | 25% | Ziffy DSCR purchase terms can go up to 85% LTV, meaning 15% minimum down for eligible files |

Closing speed | Often 5 to 15 days | Usually 21 to 30 days |

Prepayment penalty | Rare or deal-specific | Often 3 to 5 years, depending on structure |

Best for | Fix-and-flip, auction purchases, distressed properties, BRRRR acquisition phase | Buy-and-hold rentals, portfolio scaling, stabilized investment properties |

Credit score | More flexible because the deal is asset-based | Ziffy DSCR terms currently start at 620 minimum credit score |

Property condition | Distressed properties can work | Property should be rent-ready or stabilized |

Refinance path | Refinance into DSCR after rehab and stabilization | Refinance later through a DSCR cash-out refinance |

Rates, terms, credit requirements, down payment requirements, reserves, LTV, and timelines are subject to change. Contact Ziffy Mortgage for current pricing and eligibility before making an offer or structuring a deal.

What Is a Hard Money Loan and When Does It Make Sense?

A hard money loan is short-term, asset-based financing for investment properties. Instead of underwriting mainly around your personal income, the lender focuses on the property, the purchase price, the after-repair value, the rehab scope, and the exit plan.

The distinction here is between ARV-based underwriting and rent-based underwriting. Hard money lenders usually care most about whether the property has enough equity potential to support the loan. A DSCR lender cares more about whether the finished property can support the monthly payment through rent.

What most guides do not mention is that hard money can work even when the property currently produces zero rent. That is the point. If the property is distressed, vacant, outdated, or not ready for a tenant, the loan is usually built around what the property can become after the rehab, not what it is producing today.

Hard money is usually funded by private capital sources rather than traditional banks. That is why terms can vary widely by lender, property, market, borrower experience, and renovation plan. It is also why hard money can move quickly when a conventional or DSCR loan would be too slow.

Hard money is temporary by design. You use it to buy the property, complete repairs, and then either sell the property or refinance into long-term financing. The cost reflects that speed and flexibility. Investors should expect higher rates, points, lender fees, and a shorter payoff window than they would see on a permanent rental loan.

For a flipping-specific breakdown, see Ziffy’s fix and flip loan guide and our guide on how to flip a house. Before committing to a short-term loan, run the rehab math in Ziffy’s Fix & Flip Calculator so the purchase price, repair budget, ARV, holding costs, financing cost, and resale assumptions are tested together.

Hard Money Loan Pros and Cons

Pros | Cons |

|---|---|

Fast closing. Hard money can often close in days rather than weeks, which matters for auction purchases, wholesale deals, foreclosure timelines, and sellers who value certainty. | The cost is high. Hard money rates can make sense for short holds, but they can damage cash flow if you hold the loan too long. |

Distressed properties can qualify. DSCR loans usually require a property that is rent-ready or already stabilized. Hard money can work when the property needs repairs before it can qualify for permanent financing. | The payoff window is short. Many hard money loans are structured around a defined exit. If the rehab runs long or the resale timeline slips, the loan can become expensive quickly. |

Less personal income friction. The underwriting focus is usually the deal, not your W-2 income, tax returns, or personal debt-to-income ratio. | Points and fees change your real basis. Upfront lender fees, origination points, extension fees, inspection fees, and interest reserves can change the true cost of the deal. A flip that looks profitable before financing costs can tighten fast once the full capital stack is modeled. |

Flexible structure. Private lenders may adjust terms based on experience, leverage, rehab budget, ARV, interest reserves, and exit plan. | There is no long-term stability. Hard money is not meant to be your permanent rental loan. If the market softens or the refinance takes longer than planned, the financing can become the pressure point. |

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

“A lot of investors assume hard money is only for flippers. It is really the right tool any time you need speed or the property cannot qualify for permanent financing yet, like a distressed rental you plan to stabilize. The key is simple: know your exit before you take the money, not after.”

What Is a DSCR Loan and Who Is It Built For?

A DSCR loan is an investment property loan that qualifies primarily based on the property’s rental income, not the borrower’s personal income. DSCR stands for debt service coverage ratio. The formula is:

DSCR = Gross Monthly Rent ÷ PITIAPITIA means principal, interest, taxes, insurance, and association dues when applicable.

Technically speaking, a DSCR of 1.00 is mathematical break-even. The rent covers PITIA to the dollar, but it does not leave much cushion for vacancy, maintenance, tax changes, insurance increases, HOA dues, or repair reserves. A DSCR above 1.00 means the rent exceeds the monthly housing payment.

At Ziffy, a 1.00 or above DSCR usually creates the cleanest path on a standard file, while eligible properties below 1.00 may still work through Ziffy’s No-Ratio DSCR option.

The underlying mechanics explain why DSCR loans do not require the same income package as a conventional investor loan. The property is doing the qualifying. We still review the full file, including credit, leverage, reserves, property type, rent support, and ownership structure, but the loan is not built around W-2s, pay stubs, tax returns, or DTI.

That makes DSCR a strong fit for investors who:

- are self-employed

- buy through an LLC

- own multiple rental properties

- write off aggressively on tax returns

- want to scale without conventional DTI limits

- are buying or refinancing long-term rentals

- want rental-income-based financing for eligible investment properties

If your main financing challenge is that your tax returns do not show the full strength of your rental strategy, Ziffy’s guide to getting a rental property loan without tax returns explains why DSCR is often the cleaner path.

For qualifying DSCR purchase files, Ziffy can finance up to 85% LTV, with down payments starting at 15%. Current DSCR guidelines also start at a 620 minimum credit score, with loan amounts from $100,000 to $10 million, rate-and-term refinance options up to 80% LTV, cash-out refinance options up to 75% LTV, and reserve requirements starting at 2 months. Final terms depend on the full file, including credit profile, property type, leverage, rent support, reserves, and current program guidelines.

You can review the full DSCR loan requirements or run the numbers with Ziffy’s DSCR loan calculator before applying.

DSCR Loan Pros and Cons

Pros | Cons |

|---|---|

Long-term financing. DSCR loans are built for stabilized rental holds, not short-term exits. A 30-year structure can create a more predictable payment profile than temporary private capital. | The property needs to be ready. Distressed properties usually do not work for DSCR financing until they are repaired, rentable, and supportable through lease or market rent. |

No personal income verification on the core DSCR path. The file is not centered on W-2s, tax returns, pay stubs, or personal DTI. | The ratio can block weak deals. If rent does not support PITIA, the property may need a lower purchase price, higher down payment, stronger rent support, or a No-Ratio structure if eligible. |

Portfolio scaling is cleaner. Because the property’s rent is the main qualifying engine, DSCR can work better for investors whose personal income file does not reflect the strength of their rental portfolio. | Prepayment penalties can affect exit flexibility. A DSCR loan can be the wrong structure if you plan to sell quickly and the prepayment penalty period creates a meaningful cost. |

Cash-out refinance options. After equity builds, a DSCR cash-out refinance can help investors access capital without switching back into a tax-return-heavy underwriting path. | Rates are usually higher than conventional investor loans. DSCR loans reduce income-documentation friction, but that flexibility is priced into the loan. |

Based on DSCR files we review, the most common early underwriting surprise is not the rent number. It is PITIA. Investors often use the seller’s current tax bill, a rough insurance estimate, or an incomplete HOA figure when they run the first pass. Once the full PITIA is built correctly, a property that looked like a 1.05 DSCR can fall below break-even.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

Which Loan Fits Your Strategy? 5 Investor Scenarios

The best way to compare hard money vs DSCR loans is by strategy. A loan that works perfectly for one deal can be a poor fit for another.

1. The House Flipper

If you are buying a distressed property at a discount, renovating it, and planning to resell within 6 to 9 months, use hard money.

A distressed property usually will not qualify for DSCR financing because the income is not stabilized yet. The property may need repairs before it can be rented, appraised cleanly, or supported by a lease. A fix and flip loan is built for that kind of project because the loan is tied to the acquisition, rehab plan, and resale strategy.

The key risk is time. Every extra month of interest, utilities, insurance, taxes, contractor delays, and carrying costs eats into the spread. Hard money can be the right tool, but only if the exit is realistic.

2. The Buy-and-Hold Investor

If you are purchasing a turnkey single-family rental in a market where rent supports the payment. The property does not need major repairs, and your plan is to hold it for 5 to 10 years or longer, use DSCR loan.

The property is already in rental condition, the income can be measured, and the financing can be structured around the deal instead of your personal tax return.

Hard money would be too expensive for this scenario. Paying short-term private-money rates on a stable long-term rental usually weakens cash flow without adding much benefit.

3. The BRRRR Investor

If you are buying a distressed property, rehabbing it, placing a tenant, and refinancing to pull equity back out, use hard money first, then refinance into DSCR.

This is the cleanest example of how both products work together. Hard money funds the acquisition and rehab because the property is not ready for permanent financing yet. Once the rehab is complete and the property is rented, DSCR financing can replace the short-term loan.

In our experience, the BRRRR method is the most common reason investors use both products in sequence. The hard money loan gets the property under control. The DSCR loan turns it into a long-term rental asset.

We often see investors get into trouble when they treat the refinance as a future problem. The better approach is to estimate the post-rehab rent, likely PITIA, appraised value, DSCR, and refinance proceeds before closing the hard money loan.

4. The Auction or Off-Market Buyer

If you found a deal through a wholesaler, courthouse auction, or off-market seller. The seller needs certainty, and you may have only 10 days to close, use hard money.

A DSCR loan is rarely the right tool when the close timeline is extremely short. DSCR files still need underwriting, appraisal, title, insurance, rent support, and closing coordination. Ziffy’s DSCR loan timeline is usually closer to 21 to 30 days.

Hard money wins on speed. That speed is expensive, so it should be used for deals where the discount, rehab plan, or exit strategy justifies the cost.

5. The Portfolio Scaler

If you already own multiple rentals and want to keep adding properties without conventional DTI limits becoming the bottleneck, use DSCR.

This is where DSCR becomes one of the strongest investment property loans for rental investors. Each property is evaluated largely on its own income, so your personal income file does not have to carry every new acquisition the way it would in a conventional structure.

That does not mean the rest of the file is ignored. Credit, reserves, leverage, rent support, entity documents, and property type still matter. But the loan logic is aligned with how rental portfolios actually grow.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

Hard Money Into DSCR: How Investors Use Both

Hard money and DSCR loans are not always competing products. For BRRRR investors, they are often sequential products. The hard money loan is the acquisition and rehab tool. The DSCR loan is the permanent financing tool.

Here is how the handoff usually works:

- Buy a distressed property with hard money.

- Complete the rehab.

- Place a tenant or support market rent with an appraisal.

- Order the refinance appraisal based on the improved property.

- Use the new value and rent support to qualify for DSCR.

- Pay off the hard money loan with the DSCR refinance.

- Reinvest returned capital into the next deal.

The critical point is that the DSCR refinance is not based on what you paid for the property. It is based on the improved value, the new rent support, and the finished property condition. That is why the refinance can look very different from the purchase.

A DSCR cash-out refinance can also help return original capital if the value, leverage, and DSCR support the loan. Timing matters, though. Many lenders require seasoning before refinancing out of short-term acquisition debt. Investors commonly plan around a 6 to 12 month window, depending on program rules, documentation, property history, and file strength.

A bridge loan can also sit between these two categories. Bridge financing can make sense when the property is not a full rehab project but still needs temporary financing before a sale, refinance, or stabilization event.

What we see often is investors taking hard money on a deal they originally intended to flip, then realizing the finished property cash flows well enough to hold. That can be a strong pivot, but only if the DSCR refinance math works before the hard money timeline becomes a problem.

One downside to consider: most DSCR loans carry prepayment penalties for 3 to 5 years after closing. If you think you may sell or refinance again during that window, factor the penalty into your exit math before you commit.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

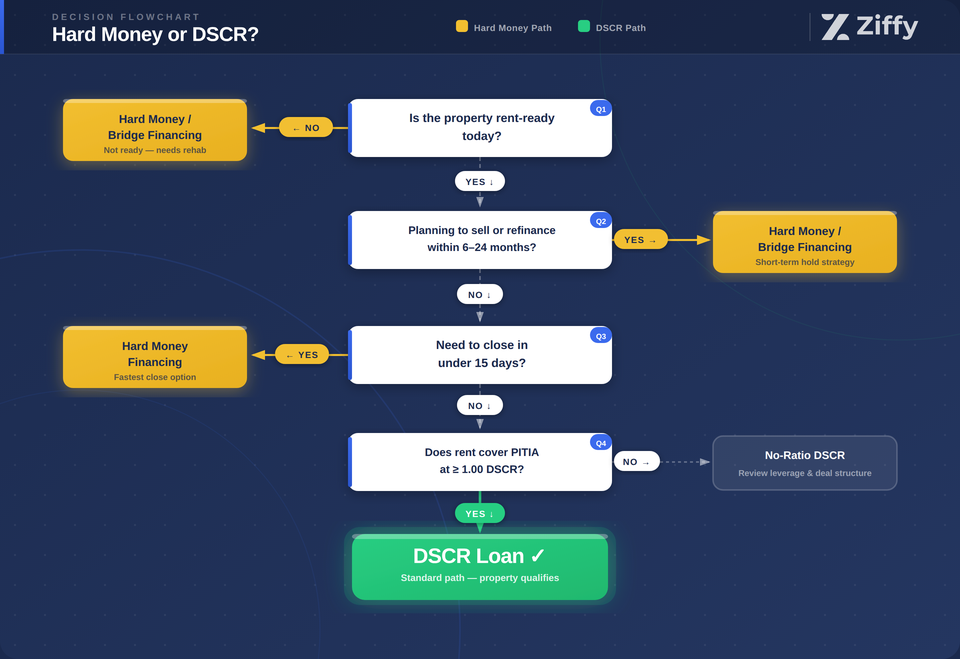

3 Questions to Pick the Right Loan

1. Is the property move-in ready?

- If no, hard money is usually the better fit.

- If yes, DSCR is in play.

A property that needs major repairs generally cannot support a rental-income-based loan yet. Stabilize it first, then refinance.

2. What is your exit strategy?

- If you plan to sell or refinance within 12 to 24 months, hard money may fit.

- If you plan to hold the property long term, DSCR is usually the better structure.

The loan should match the investment plan. A temporary loan on a long-term rental becomes expensive. A long-term loan on a short-term flip can create avoidable friction.

3. Do you need to close in under 15 days?

- If yes, hard money is usually the practical option.

- If no, DSCR wins on long-term cost and payment stability when the property qualifies.

The timeline question is often the easiest filter. Fast capital has a price. Permanent financing takes more documentation and coordination, but it usually makes more sense once the property is stabilized.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

Bottom Line: Hard Money Is for the Setup, DSCR Is for the Hold

Hard money is best when the property is not ready for permanent financing, the closing timeline is tight, or the plan is to renovate and exit quickly.

DSCR is best when the property is ready to rent, the income supports the payment, and the investor wants long-term financing without relying on personal income documentation.

For many investors, the strongest strategy is not hard money or DSCR. It is hard money first, DSCR later. That is the financing rhythm behind many BRRRR deals: acquire, improve, stabilize, refinance, repeat.

Before choosing either loan, run the DSCR math, estimate the real holding period, and build the exit before the offer is signed.

If you are not sure which structure fits your deal, talk to a Ziffy loan specialist. You can also run the property through the DSCR loan calculator or review Ziffy’s DSCR loan requirements before applying.

FAQs

Is a hard money loan better than a DSCR loan?

A hard money loan is better for short-term deals, distressed properties, fast closings, auctions, and flips. A DSCR loan is better for stabilized rental properties that you plan to hold long term. The better loan depends on the property’s condition and your exit strategy.

When should I use hard money instead of DSCR?

Use hard money when the property is not rent-ready, needs rehab, must close quickly, or will be sold or refinanced within a short window. DSCR usually works after the property is stabilized and the rent can support the payment.

When should I use a DSCR loan instead of hard money?

Use a DSCR loan when the property is move-in ready, rental income supports PITIA, and your plan is to hold the property as a rental. DSCR is usually the stronger long-term structure because it is built around property income rather than personal income documents.

Can I refinance from hard money into a DSCR loan?

Yes, that is a common investor strategy. After the property is repaired, rented, and appraised at its improved value, a DSCR refinance can replace the hard money loan. This is especially common in BRRRR deals.

Can I use a DSCR loan for a fix-and-flip property?

Usually no. A fix-and-flip property often needs repairs and does not have stable rent support. A fix-and-flip loan or hard money loan is usually the better fit during the rehab phase. DSCR becomes relevant if you decide to hold the property as a rental after the rehab.

What if my property does not meet a 1.00 DSCR?

A property below 1.00 does not automatically fail. At Ziffy, eligible properties that do not meet the standard DSCR threshold may still qualify through a No-Ratio DSCR option. The file may need stronger structure elsewhere, such as lower leverage, stronger credit, or more reserves.

Are hard money loans more expensive than DSCR loans?

Yes, hard money is usually more expensive because it is short-term, faster, and tied to higher-risk situations such as distressed properties or rehab projects. DSCR loans are generally better suited for long-term rental holds.

Does Ziffy offer both hard money and DSCR financing?

Ziffy offers investor-focused financing options, including DSCR loans, bridge loans, and fix-and-flip financing. The right product depends on the property condition, timeline, leverage, rent support, and exit strategy.