Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Table of Contents

If you are financing an investment property in 2026, the deal has to work on paper before it ever works in a portfolio. The average 30-year fixed mortgage rate was 6.46% as of April 2, 2026. Investor activity still accounted for 30% of all single-family home purchases at the close of 2025, and rental vacancy stood at 7.2% in Q4 2025.

At the same time, our Ziffy reports found that potential rental yields declined in 54.8% of analyzed counties even though rents rose faster than home prices in 55% of them. This combination means there is still investor demand, but it also means sloppy underwriting gets punished fast.

That is exactly why DSCR loans matter. A DSCR loan is not just a way to avoid traditional income documentation. It is an investment mortgage that is built around the income potential of the property itself.

At Ziffy Mortgage, we underwrite DSCR based on the property’s rental income, property cash flow, and investor use cases such as purchases, refinances, and eligible short-term rental scenarios. That is the right lens. The property has to support the debt.

This guide covers what a DSCR loan is, how the ratio is calculated, how Ziffy Mortgage approaches underwriting, when this financing works best, what mistakes can weaken a file, and how Ziffy.ai can help investors analyze deals before they apply.

Quick answers

1. A DSCR loan is an investment loan that qualifies primarily based on rental income.

2. DSCR stands for debt service coverage ratio.

3. The formula is gross monthly rent divided by PITIA.

4. PITIA includes principal, interest, taxes, insurance, and association dues when applicable.

5. A DSCR of 1.00 means the property is covering its monthly debt obligation.

6. At Ziffy Mortgage, a 1.00 or above DSCR usually creates the cleanest path on a standard file.

7. Some eligible files below 1.00 may still work through a No-Ratio DSCR loan.

8. Ziffy Mortgage DSCR loans can be used for purchases, rate-and-term refinances, cash-out refinances, and eligible short-term rental properties.

What is a DSCR Loan?

A DSCR loan is an investment property mortgage that allows you to qualify based mainly on the property’s rental income rather than your personal income.

That is the simplest way to understand it.

With a traditional mortgage, approval is built around your personal finances. The lender wants to see your income, your tax returns, your employment, and your overall debt-to-income ratio. That can work well for many borrowers, but it becomes much less useful when the asset being financed is supposed to function as a rental property.

A DSCR loan shifts the focus back to the deal itself. The question is no longer, “Does the borrower’s W-2 income support this mortgage?” The more relevant question becomes, “Does the property produce enough income to support its own monthly debt?”

That is why DSCR financing is such a practical fit for:

- self-employed investors

- investors who buy through LLCs

- borrowers with multiple financed properties

- investors with significant write-offs on tax returns

- borrowers buying or refinancing long-term rentals

- eligible short-term rental investors

At Ziffy Mortgage, the underwriting process is built around that investor logic. The property’s rent matters first. That does not mean the rest of the file disappears. Credit, leverage, and reserves, along with property type, rent support, and ownership structure still matter.

Steven Glick,

Director of Mortgage Sales

What if the property does not meet a 1.00 DSCR?

A deal is not automatically dead just because it falls below the standard threshold.

At Ziffy Mortgage, eligible properties that do not currently meet a 1.00 DSCR may still qualify through a No-Ratio DSCR loan. In most cases, that means the deal needs stronger structure elsewhere, such as a higher down payment or a more conservative leverage profile.

That matters because not every workable investment property fits perfectly into a neat underwriting box on the first pass.

Why DSCR Matters More in 2026

In 2026, rates are still elevated, acquisition costs remain high, and investor competition has not disappeared. Our survey showed the average 30-year fixed rate at 6.46% on April 2, 2026. Also, investors still represented 30% of all single-family home purchases at the end of 2025, averaging roughly 80,000 to 100,000 monthly purchases through late 2025. That tells you investor demand is still there and that the bar for clean financing has not gone away.

What most guides do not mention is that investor demand is holding up at the same time returns are getting squeezed. ATTOM’s 2026 Single-Family Rental Market Report says the national median sales price hit a record $360,000, and projected rental yields declined in 54.8% of counties with enough year-over-year data to compare. Even where rents are rising, higher home prices are compressing returns.

In other words, rent growth alone is not enough. Your leverage, insurance, taxes, and entry basis matter more than they did in easier cycles.

The other market signal worth paying attention to is negotiation power. At Ziffy, we found that 62.2% of all homebuyers in 2025 paid below the original list price, and the typical buyer who bought below list got a 7.9% discount, the largest since 2012. In Miami, 85.4% of homes sold below original list price. In Fort Lauderdale, that figure was 86.9%. In Dallas, it was 79.4%. That matters for DSCR because deal structure starts at acquisition. A better purchase price can improve leverage, lower PITIA, and help move a borderline file into workable range.

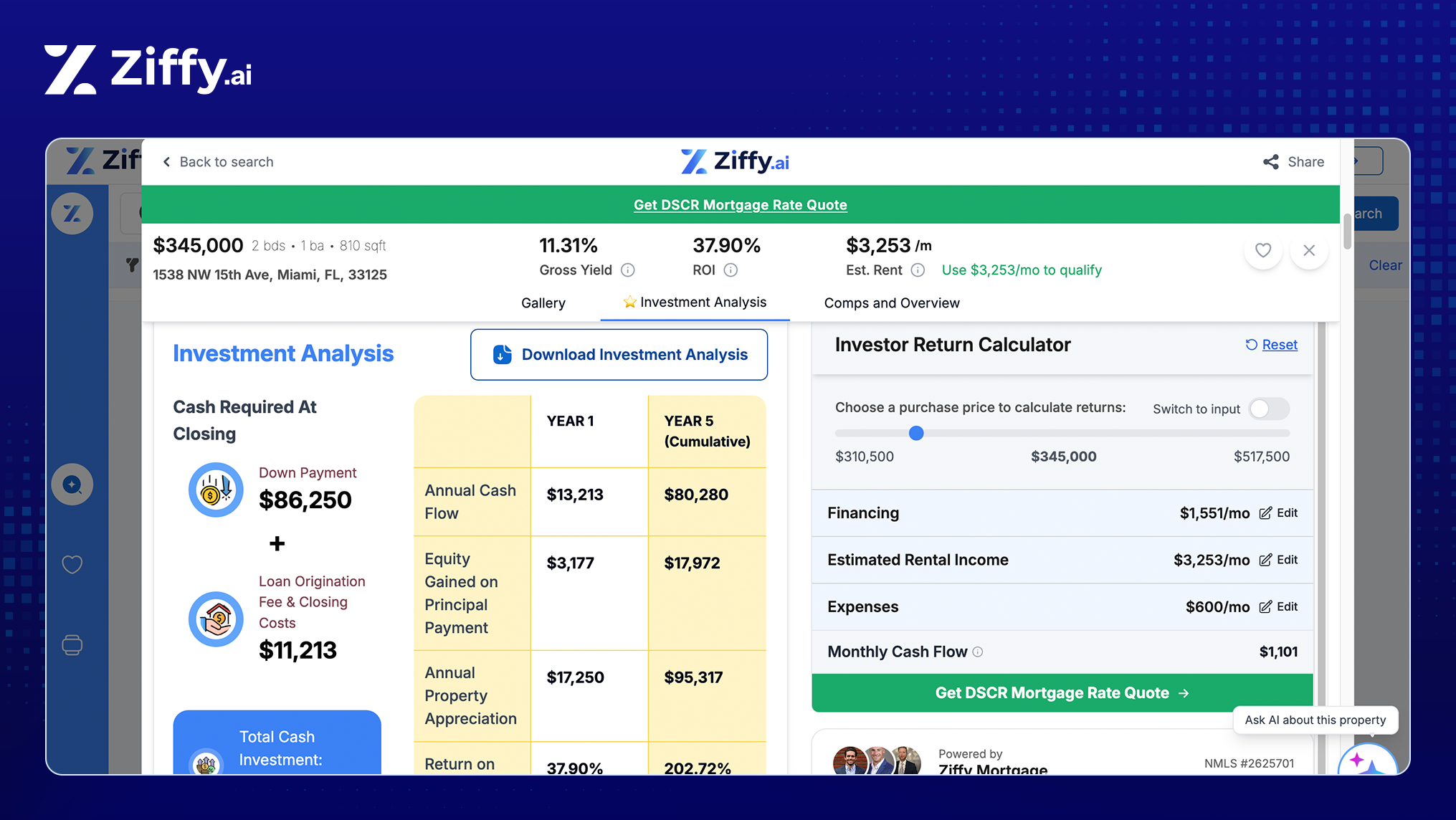

How is DSCR calculated? [Or Skip the Math with Ziffy.ai’s In-built DSCR Loan Calculator]

When you apply for a DSCR Loan, the first thing that matters is the DSCR itself. This ratio tells us whether your property can cover its monthly loan payments using the rent it brings in.

The formula is pretty straightforward:

DSCR = Gross Rental Income / PITIA

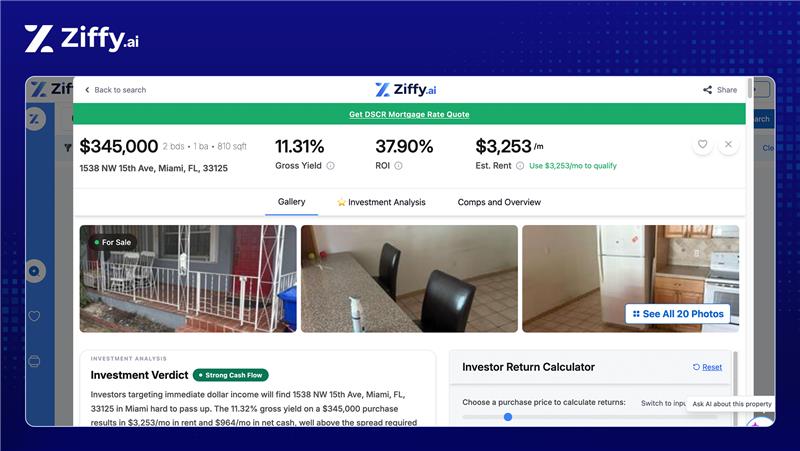

Let’s understand this with a simple example using this property in Miami, Florida listed on our Ziffy.ai platform:

- Estimated Monthly Rent: $3,376

- PITIA: $2,451

Now, DSCR for this property would be: $3,376 ÷ $2,451 = 1.38

This means the property earns 38% more than it needs to cover the full monthly payment.

What Your DSCR Results Mean

You can use the ranges below to interpret your DSCR result in plain terms.

- POOR (below 0.75):

If your DSCR is under 0.75, the rent is covering less than three-quarters of the PITIA payment. In most DSCR programs, this is not approvable without major changes to leverage, structure, or rent.

- FAIR (0.75 to 1.0):

If your DSCR is between 0.75 and 1.0, the rent is close, but still not fully covering PITIA. This usually indicates the loan amount is too high for the rent level, or taxes and insurance are compressing coverage.

- GOOD (1.0 to 1.25):

If your DSCR is between 1.0 and 1.25, the rent covers PITIA with a modest cushion. Many programs treat 1.0 as a minimum pass, while 1.25 or higher is often preferred for stronger terms.

- EXCELLENT (above 1.25):

If your DSCR is above 1.25, the rent supports PITIA with a stronger buffer. This tends to be more resilient to realistic shifts in expenses or rent documentation.

Steven Glick,

Director of Mortgage Sales

Hate doing the math?

Ziffy.ai’s built-in DSCR calculator does the work for you. Our platform automatically checks your qualification based on rental income estimates, financing terms, and expense breakdowns.

You can even adjust your property price, down payment, interest rate, or expenses to see how the ratio shifts before you move forward.

What Can Change the DSCR Quickly?

The biggest trap is assuming rent is the only number that matters. In actual underwriting, a file can look strong at a glance and then weaken once full PITIA is built correctly. Taxes, insurance, HOA dues, and final leverage are usually what move the ratio the most.

Property taxes are a major example. Tax Foundation’s current state rankings show effective property tax rates of 1.83% in Illinois, 1.36% in Texas, 0.74% in Florida, and 0.70% in California on owner-occupied housing value. Those are statewide averages, not deal-level underwriting numbers, but they show why two properties with similar purchase prices can produce very different DSCR outcomes once taxes are fully loaded.

Insurance is now just as important. Treasury’s Federal Insurance Office reported that average homeowners insurance premiums increased 8.7% faster than inflation between 2018 and 2022. In the highest-risk ZIP codes, homeowners paid $2,321 on average, which was 82% more than homeowners in the lowest-risk ZIP codes, and non-renewal rates in those high-risk ZIP codes were about 80% higher. Florida’s Office of Insurance Regulation says the average homeowner’s premium in the admitted market is approximately $3,600.

Texas’ Department of Insurance says the state had 8,233,096 active homeowners policies in 2025 and an average annual homeowners premium of $3,291 in 2024. If an investor is still using a placeholder insurance number early in the process, the DSCR may not be telling the truth yet.

Steven Glick,

Director of Mortgage Sales

Ziffy Mortgage DSCR Loan Program Terms

Feature | Ziffy DSCR Loan |

|---|---|

DSCR Ratio |

|

Credit Score | Minimum 620 |

Loan Amount | $100K – $10M |

Down Payment | 20% |

LTV | Up to 80% (Purchase) |

Cash Reserves | 2 months |

Property Use | Investment properties (residential and commercial) |

These terms are useful as a starting point, but they should not be treated like a simple checklist. A file does not become strong just because it technically hits one number. The overall structure still matters. That includes the quality of the rent support, the leverage, the borrower’s reserves, and whether the property type and ownership structure make sense for the strategy.

How Ziffy Mortgage DSCR Loans Fit Real Investor Scenarios

A Ziffy Mortgage DSCR loan is usually the right conversation when the property’s income tells a stronger story than the borrower’s personal tax returns.

That happens more often than people think.

A borrower may be self-employed, hold multiple rentals, write off aggressively, or buy through an LLC. On a conventional file, those details can create more friction than the property deserves. On a DSCR file, the focus shifts back to the deal itself.

In our experience, that is why DSCR financing tends to appeal most to investors buying long-term rentals with supportable market rent, investors refinancing stabilized properties into a cleaner long-term structure, and investors scaling a portfolio who no longer want every new purchase judged mainly through personal DTI logic.

Financing should match the investment strategy. When the loan structure fits the way you actually buy and hold property, the process gets more efficient and the next deal becomes easier to plan.

Ziffy Mortgage’s DSCR Loan vs. Traditional Mortgage: Why Investors Choose DSCR Loans?

Traditional mortgages were built for homeowners, not investors. They’re tied to your personal income, tax history, and employment status. DSCR Loans, on the other hand, qualify you for the loan based on your property’s income.

Here’s a quick comparison between the two loan types:

Feature | Ziffy Mortgage DSCR Loan | Traditional Mortgage |

|---|---|---|

Approval Based On | Property’s rental income (DSCR) | Your personal income, W-2s, and DTI |

Tax Returns Required | Not required | Typically required for 2 years |

Employment Verification | Not required | Always required |

DTI (Debt-to-Income) | Not considered | Key approval factor |

Entity Type | Ideal for LLCs and business use | Personal use only |

Speed of Approval | Faster, fewer documents | Slower due to full underwriting |

Investor Flexibility | High; scale faster, even with multiple properties | Low; limited by income and property count |

DSCR loans are not popular because they sound different. They are popular because they solve a real problem for rental investors.

They fit how investors actually buy and hold property

Most active investors are not financing one house to live in. They are buying income-producing assets. They may be self-employed. They may own through an LLC. They may already have multiple financed properties. They may have tax returns shaped by depreciation and write-offs.

A conventional file often treats all of that as friction. A DSCR file is usually better aligned with what the borrower is actually doing.

They can work better when tax returns are not the full story

This is a big reason DSCR financing becomes useful for self-employed borrowers and experienced investors. Someone may have strong liquidity and solid rental performance, but tax returns still make a conventional file look tighter than it should.

With DSCR, the property itself carries more of the qualification burden.

They are often easier to structure for LLC ownership

Many investors want to hold rental property in an LLC for asset protection, accounting, and portfolio structure reasons. DSCR loans tend to fit that ownership approach more naturally than conventional financing.

At Ziffy, that is part of the conversation early because entity structure affects the contract, title, and closing flow.

They support scaling differently than conventional financing

This matters more as an investor grows.

Fannie Mae’s current selling guide still limits borrowers to ten financed one-to four-unit residential properties and also applies additional reserve requirements when borrowers have multiple financed properties tied to second-home or investment-property transactions.

That does not mean every investor hits that wall in the same way. But it does explain why conventional financing becomes less flexible as financed properties accumulate. For active investors, DSCR often becomes the more practical structure because it evaluates the next deal more on its own rental strength.

Steven Glick,

Director of Mortgage Sales

They work for more than just purchases

DSCR loans are not only for buying a new rental. Investors also use them to refinance stabilized properties, pull equity through a cash-out refinance, move out of short-term financing into permanent debt, and finance eligible short-term rental properties.

That range matters because an investor’s financing needs change as the portfolio changes.

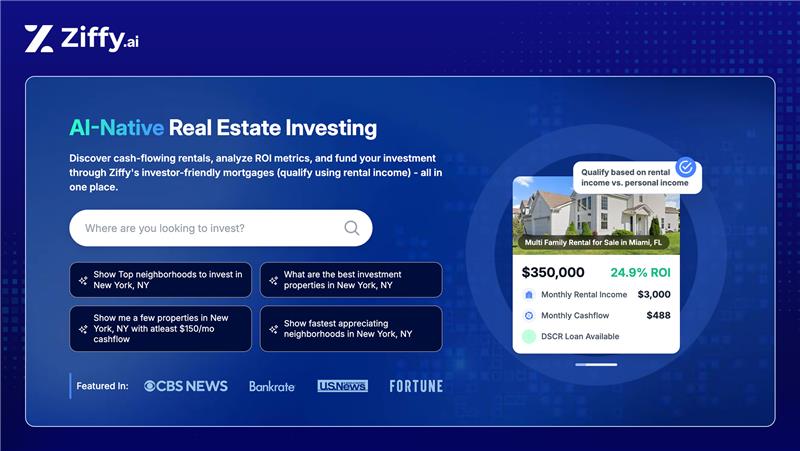

With Ziffy.ai, you can browse cash-flowing rental properties, analyze your DSCR and ROI metrics in real time, and finance your rentals, all in one place. There’s no back-and-forth with personal documentation, and no bottlenecks when your portfolio grows.

If you’re investing for cash flow and long-term equity, DSCR loans are often the financing solution that actually matches your strategy.

Types of DSCR Loans Investors Use Most

A lot of articles talk about DSCR as if it is one product. It is better to think of it as a category of investor financing with several common use cases.

Standard DSCR purchase loan

This is the most common version. You are buying a rental property and qualifying based on the property’s income rather than personal income documentation. This structure is often used for single-family rentals, condos, townhomes, 2 to 4 unit residential properties, and other eligible non-owner-occupied property types.

A standard DSCR purchase loan is usually the cleanest fit when the property already works as a rental and the rent supports the debt well enough.

DSCR rate-and-term refinance

This is commonly used when an investor wants to replace an existing loan with a more stable long-term structure without pulling cash out.

A typical use case is a borrower who bought or renovated a property with another loan, stabilized the asset, then wants to move into DSCR financing once the property is rent-ready and performing.

DSCR cash-out refinance

A cash-out refinance gives an investor a way to tap equity from a stabilized property while still qualifying based on rental performance.

This can be useful for funding another down payment, pulling capital for renovations, restructuring portfolio liquidity, or redeploying equity instead of leaving it trapped in the property.

This is also where structure matters. Pulling cash out changes the loan amount. That changes the payment. That changes the ratio. A property that looked comfortable before the cash-out may tighten more than expected after the refinance.

No-ratio DSCR loans

At Ziffy, eligible properties may still fit through a no-ratio DSCR option when the ratio falls between 0 and 1. That does not mean every below-1.0 deal works. It means some files can still be structured when leverage is lower or the overall file is stronger.

That matters because real investing does not always happen in a neat box. Some properties are in early lease-up. Some markets are stronger long-term holds than they are immediate cash flow plays. Some borrowers are willing to bring in more equity to keep the deal workable.

DSCR for eligible short-term rentals

Short-term rental DSCR financing can work well in the right market, but it is also where discipline matters most.

The property may be in a great location. The nightly rate may look strong in peak season. But short-term rental income can be uneven, seasonal, and easy to overstate.

That is why Ziffy looks closely at how the income story is being supported. Investors who treat STR income conservatively tend to build stronger files. Investors who model only best-case occupancy usually create avoidable problems.

What Ziffy is Really Reviewing on a DSCR File

One of the biggest misconceptions about DSCR loans is that they are easy because they do not require full personal income documentation. That is too simplistic.

They are usually cleaner than conventional loans for the right borrower, but they still involve real underwriting. Ziffy is not just checking whether the property hits one number and moving on.

The ratio is the first screen

A DSCR of 1.00 or above usually creates the cleanest path for a standard file because the property is covering its monthly debt obligation. However, at Ziffy Mortgage, we also offer No-Ratio DSCR Loans for properties with DSCR between 0 – 1.

The amount of equity changes the file

The amount of money the borrower is putting in affects the loan amount, which affects the payment, which affects the ratio. That is why equity matters so much. More money down can turn a marginal file into a workable one very quickly.

Credit still matters

Credit also matters because it influences pricing and flexibility. A lower score does not always kill the file, but it often means the structure needs to be stronger elsewhere.

Reserves matter more than many investors expect

A borrower who has enough cash to close but no real post-closing liquidity is running a much thinner file than the numbers may suggest at first glance.

Property type and property use change the risk profile

A leased single-family rental is not the same file as a condo with heavy HOA dues. A short-term rental is not the same file as a year-long lease. A vacant fix-up is not the same file as a stabilized hold.

Ownership structure should be handled early

Ownership structure matters too. If the borrower wants to close in an LLC, that should be built into the file from the beginning. Too many deals get delayed because the contract, entity documents, and loan structure are not lined up early.

Steven Glick,

Director of Mortgage Sales

From Property to Pre-Approval: Apply for DSCR Loan

One of the more useful angles on the live page is that Ziffy does not present financing as an isolated final step. The platform connects property search, rent and ROI analysis, and mortgage education in one investor workflow. That matters because financing becomes more useful when it is connected to the investment decision from the start. The investor is not just asking, “Can I get a loan?” The investor is asking, “Is this a property worth financing at all?”

Here’s how you can do it yourself in a few quick steps:

Discover High-Yield Investment Properties

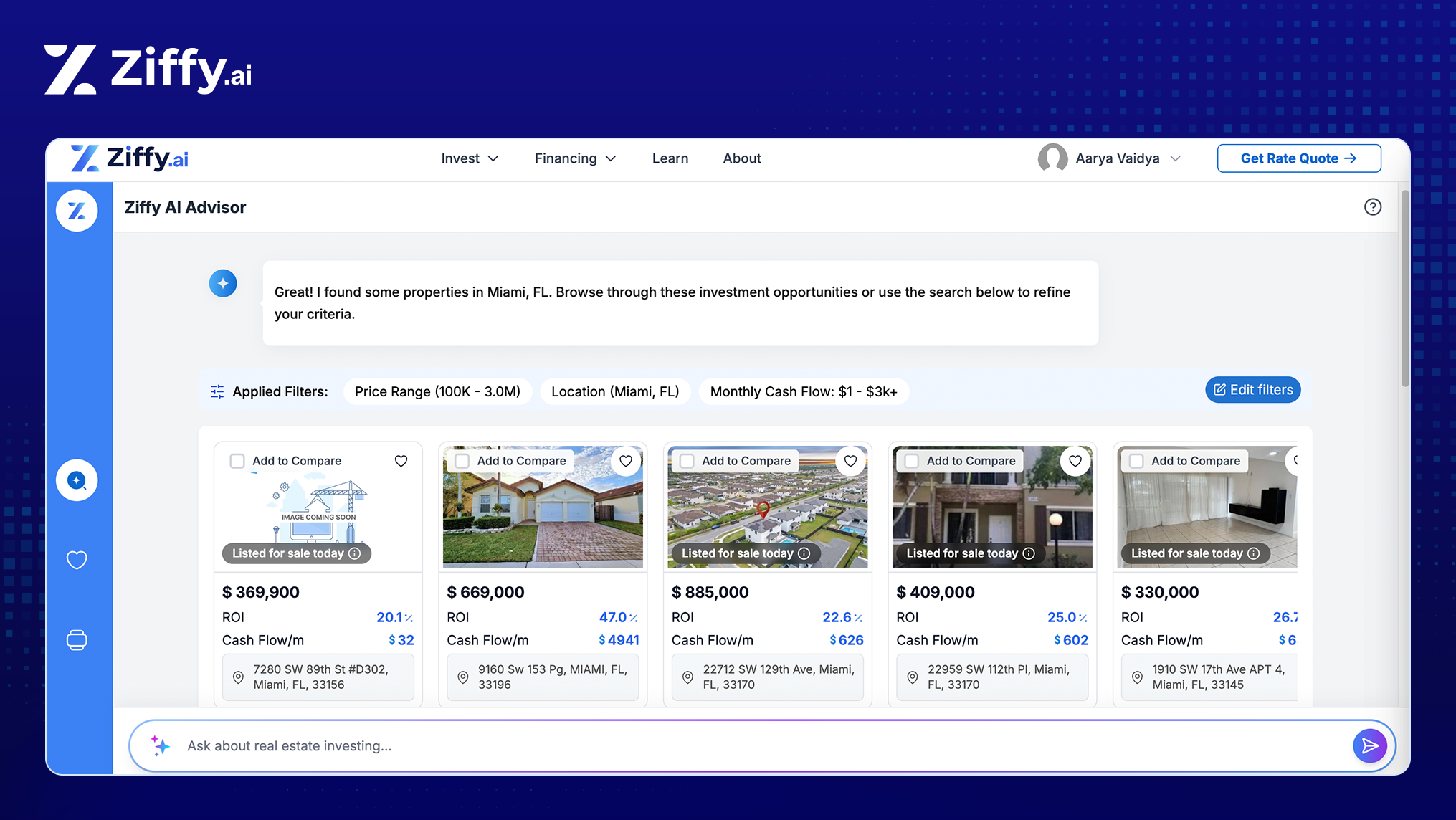

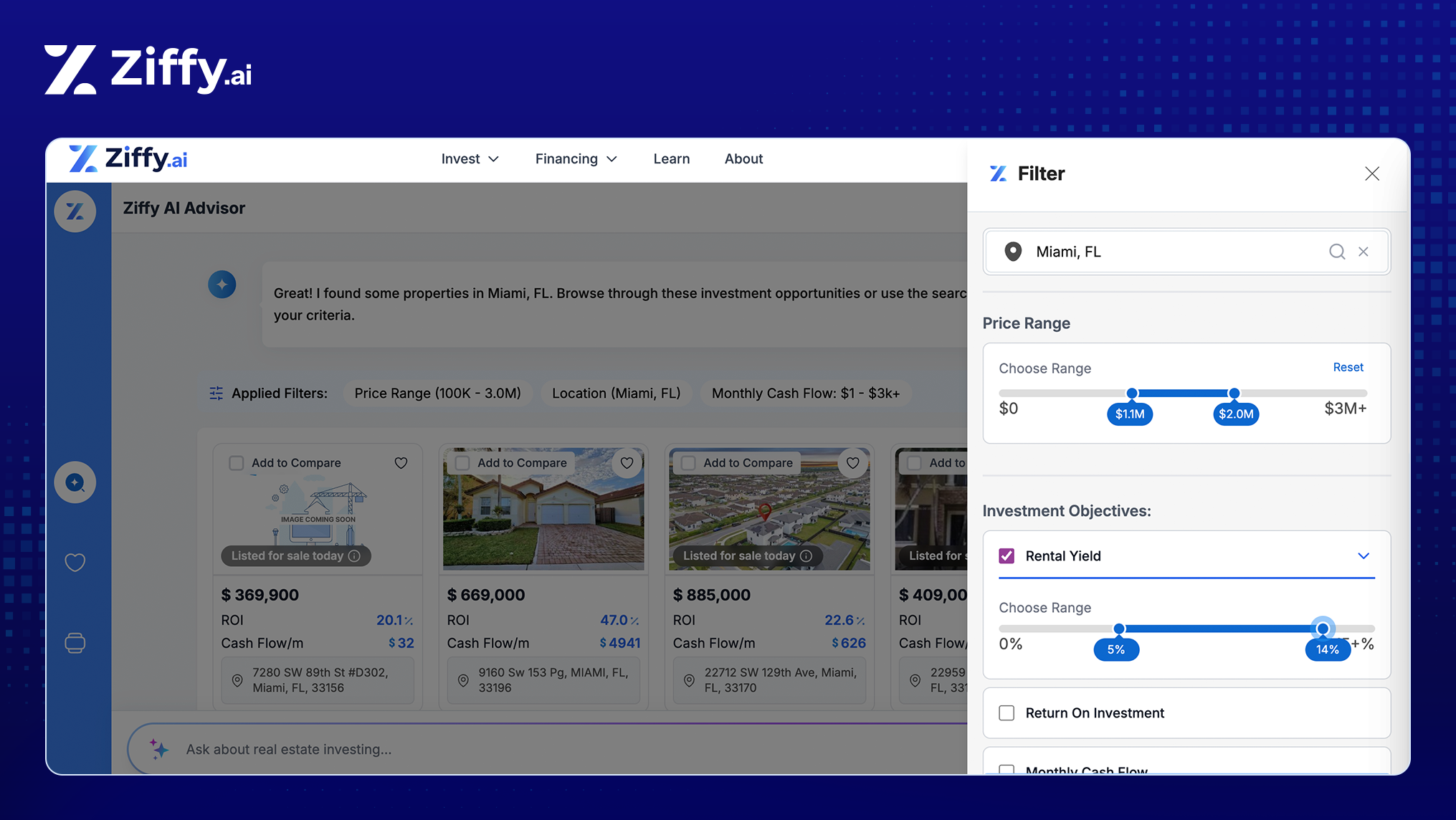

Start by entering your desired location, as soon as you do, ZiffyAI activates instantly to guide your search in real time.

You’ll see personalized property results based on your price range, home type, and cash flow goals. The AI automatically applies filters like monthly cash flow and ROI, helping you surface listings aligned with your investment strategy.

And not only that, ZiffyAI doesn’t only show listings; it identifies markets with strong rental demand, limited inventory, and solid appreciation potential.

Whether you’re targeting consistent monthly cash flow or long-term equity growth, our data-backed suggestions help you focus on locations that support your goals.

Analyze Financial Metrics Instantly

Click into any listing to access a full financial breakdown and analysis. You can check projected rent, expenses, ROI, and more. To check whether you qualify, you can tweak metrics like estimated rental income and expenses to check your cash flow and see how the deal holds up.

Save and Compare Investment Properties the Smart Way

Like the property you see? Save properties to your shortlist for later.

Ziffy.ai lets you compare key metrics like ROI and cash flow side by side. With our AI-native real estate investing technology, you are not only browsing listings, you are building a data-backed investment strategy.

Pre-Qualify Using Property Income

Once you have checked the numbers and are happy with it, pre-qualify for a DSCR loan directly from the listing. Ziffy doesn’t require tax returns or income docs.

We qualify you based solely on the property’s ability to cover the mortgage.

Connect with Investor-Friendly Agents

We also connect you with experienced agents who will help you with your investment.

Initiate the Loan Process and Close the Deal

Upload your documents to the portal. We’ll handle underwriting, appraisal, title, and closing. You can track all this through your Ziffy.ai dashboard. No back-and-forth or surprises.

Expand Your Portfolio

Once your loan is in place, you can track performance, explore refinance options, and roll equity into your next deal, all with the help of your Ziffy.ai dashboard.

The Common Mistakes That Most Often Kill DSCR Deals

Not using full PITIA

A property may look strong when rent is compared only with principal and interest. But that is not how DSCR is actually judged. Taxes, insurance, and HOA dues all count toward the monthly payment. Once those costs are added in, the ratio can shift fast.

Using optimistic rent

Some deals only work because the rent assumption is too aggressive. That happens when investors rely on the highest asking rents in the area, assume immediate top-market performance, or project short-term rental income based on peak-season numbers. A DSCR loan needs supportable rent, not best-case rent.

Choosing the loan by rate alone

The lowest rate is not always the best loan. A quote can look cheaper upfront but still be the weaker option if leverage is too high, reserves are thin, or prepayment terms do not fit the hold plan. The right loan has to match the deal, not just win on rate.

Setting up the contract the wrong way

If the property is meant to close in an LLC, that should be handled early. Writing the contract one way and trying to switch the ownership structure later can create delays that were easy to avoid.

Bringing enough money to close, but not enough to hold

Some investors plan well for the down payment and closing costs but leave themselves too little room after closing. A property may qualify on paper and still feel tight in real life if reserves are weak. A cleaner file usually gives the borrower room for vacancies, repairs, and normal surprises.

Using DSCR too early in the property’s life cycle

DSCR financing works best when the property is already functioning, or is close to functioning, as a real income-producing asset. If the property is still vacant, under renovation, or not yet rent-ready, bridge financing may be the better first step, with DSCR coming later once the asset is stabilized.

Case Study: How a Ziffy Mortgage DSCR Loan Can Work

An investor is buying a single-family rental in the Dallas-Fort Worth area and wants financing through an LLC. The property is listed at $359,000, but after reviewing comparable sales, projected rent, taxes, insurance, and the likely monthly payment, the investor decides the deal only works at a lower basis. After a short negotiation, the purchase price is reduced to $342,000.

The investor plans to use the home as a long-term rental. A market rent analysis supports $2,950 per month. The borrower chooses a 25% down payment, bringing the loan amount to $256,500. Once taxes, insurance, principal, interest, and estimated monthly housing costs are fully loaded, the projected PITIA comes to $2,305 per month. That puts the property’s DSCR at 1.28.

What makes this a good example is that the deal looked cleaner on the first pass than it did a week later. Early on, the investor used a softer insurance estimate and assumed a lower tax burden. Once the file was reviewed more carefully, the monthly expense picture tightened. The deal still worked, but the margin was smaller than the investor first expected. That is common in DSCR underwriting. The formula is simple. The real work is making sure the inputs are realistic.

DSCR Loan Details

Item | Details |

|---|---|

Market | Dallas-Fort Worth, Texas |

Property type | Single-family rental |

Purchase price | $342,000 |

Original list price | $359,000 |

Down payment | 25% |

Loan amount | $256,500 |

Estimated monthly rent | $2,950 |

Monthly PITIA | $2,305 |

DSCR | 1.28 |

Borrower structure | LLC |

Loan purpose | Purchase |

Timeline from search to closing

Day 1: The investor identifies the property and runs the initial numbers, focusing on expected rent, taxes, insurance, and cash flow.

Day 3: A pre-approval request is started after the investor confirms the target purchase range and cash-to-close comfort level.

Day 6: The offer is submitted below list price after the investor sees that the original price leaves too little room once full PITIA is modeled.

Day 8: The seller counters. The investor holds firm on economics and the parties agree at $342,000.

Day 11: The LLC documents, bank statements, and property details are submitted for full review.

Day 15: The rent support comes back in line with the original projection, but the insurance quote is higher than the investor used in the first draft analysis.

Day 18: The payment is reworked using the updated insurance figure. The DSCR drops from the investor’s early estimate, but still remains above 1.20, which keeps the deal in a comfortable range.

Day 22: Final underwriting questions focus on reserves, LLC documentation, and confirming the property’s rent strategy.

Day 27: The file is cleared to close.

Day 30: The transaction closes.

“I liked that my conversation with Steve was focused on whether the property actually made sense, not just whether I could get approved. We worked through the rent, taxes, insurance, and reserves early, and that helped me move forward with a property that felt solid instead of stretched.”

Investor, SFR (Dallas-Fort Worth Area)

Investment Properties on Sale in Dallas-Fort Worth

Why this matters

The biggest lesson here is not that the property “qualified.” It is that the investor adjusted the acquisition price before locking into a weak structure. A lot of buyers try to solve a thin deal with loan shopping after the fact. In practice, stronger DSCR files usually come from better purchase discipline, cleaner expense assumptions, and enough liquidity left after closing.

That is also why Ziffy’s investor workflow matters. The financing decision becomes more useful when it starts with property analysis, not just a rate request.

Steven Glick,

Director of Mortgage Sales

Ready to Qualify Based on Your Investment Property’s Cash Flow?

The smartest investors know that good financing is just as important as a good deal. At Ziffy, we’ve built a platform that works the way you invest. From AI-native real estate investment property search to analysis to funding, everything happens in one place. No delays, no unnecessary documents, and no second guessing.

If you’re ready to scale your portfolio with confidence, Ziffy can help you take the first step toward closing your next cash-flowing investment.

FAQs

Who can qualify for a DSCR Loan at Ziffy Mortgage?

Any real estate investor buying or refinancing an income-generating property can qualify for a DSCR loan. Unlike traditional loans, you don’t need to show tax returns, paystubs, or employment proof. If your property’s rental income the monthly mortgage payment, you’re already in a strong position to qualify.

What does a “good” DSCR ratio look like?

A DSCR of 1 or higher means your property earns enough rent to cover its monthly payment. For example, a DSCR of 1.25 means your property makes 25% more income than needed to pay the mortgage. The higher your DSCR, the more comfortably your rental income supports the loan.

Can I get a DSCR loan if my property doesn’t meet the 1.0 ratio?

Yes. Ziffy Mortgage offers a No-Ratio DSCR Loan for properties that may not meet the standard ratio but still have strong potential. These loans may require a higher down payment or additional reserves, but they allow investors to move forward even when the property’s cash flow is still growing.

How is a DSCR Loan different from a traditional mortgage?

Traditional mortgages are based on your personal income and debt history. DSCR loans, however, focus on the property’s income. You won’t need to show W-2s or tax returns, and approval tends to be much faster. This makes them ideal for investors managing multiple properties through an LLC or business entity.

How do I check my DSCR before applying?

You can use Ziffy.ai’s DSCR calculator to see if your property qualifies. Just enter the estimated rent, purchase price, and loan details. The platform automatically calculates your ratio and even shows how changes in down payment or interest rate can affect your qualification.