Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

ARV is one of the first numbers an investor should estimate before buying a property that needs repairs. It tells you what the property could be worth after renovation, but the real purpose is more practical: ARV helps you decide whether the deal has enough room for repairs, financing costs, holding costs, resale costs, and profit.

Unlike a generic ARV explainer, this guide looks at ARV through the financing review lens: how a lender, appraiser, and investor may each treat the finished value differently before a fix-and-flip, BRRRR, or rental-hold strategy moves forward.

A strong ARV estimate starts with closed comparable sales, not a hopeful resale price. The cleaner your comps, the cleaner your offer strategy becomes. That matters whether you plan to flip the property, refinance after rehab, or keep it as a rental.

This guide explains how ARV works, how to estimate it before making an offer, how the 70% rule fits into the analysis, and how investors can use ARV with Ziffy’s Fix and Flip Calculator, Cap Rate Calculator, Cash-on-Cash Calculator, and investor-focused mortgage options.

Table of Contents

Key Takeaways:

1. ARV, or after-repair value, is the estimated market value of a property after renovations are complete.

2. For a fix-and-flip deal, ARV helps determine the resale target, maximum allowable offer, repair spread, and whether the project has enough margin to justify the risk.

3. For a BRRRR strategy, ARV can affect the refinance value and how much capital you may be able to recover after the rehab.

4. For a rental hold, ARV still matters, but the final decision should also account for rent potential, cap rate, cash-on-cash return, DSCR, and the property’s ability to support financing after it is repaired and stabilized.

5. The strongest ARV estimates are based on recently sold, renovated comparable properties in the same buyer pool. Active listings can support your research, but closed sales should carry more weight.

What Is ARV in Real Estate?

ARV stands for after-repair value. It is the estimated market value of a property after the planned renovation is complete. For a flipper, ARV is not just the price you hope to sell for. It controls the entire deal.

If ARV is too high, you may overpay. If the repair budget is too low, your margin can disappear. If the comps do not support the projected resale price, your lender, appraiser, buyer, or end investor may not agree with your exit value.

In fix-and-flip financing, ARV also affects how much capital the project can support. When you apply for a fix and flip loan, the file is not built only around what the property is worth today. The completed value matters because the exit has to be realistic.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Why ARV Matters Before You Make an Offer

ARV should be part of the offer decision, not something you calculate after the property is under contract. A rehab deal has several moving parts:

- Purchase price

- Repair budget

- Permits and inspection costs

- Holding period

- Financing costs

- Resale costs

- Market risk

- Profit target

ARV tells you whether all those pieces have enough room to fit. A property may look discounted compared with nearby renovated homes, but that does not automatically make it a good flip. The deal still has to survive the full cost stack. That is true whether the investor plans to follow a house-flipping strategy, use the BRRRR method, or hold the property as a rental. If the finished value is not high enough after repairs, financing, holding costs, and selling costs, the discount can disappear quickly.

What we see often is that investors start with the resale number they want and work backward. A better approach is to start with supported comps, build a realistic repair budget, and only then decide whether the offer price makes sense.

How to Estimate ARV

The basic ARV formula is simple:

ARV = Estimated market value after renovationThe work is in proving the estimate. A practical ARV process looks like this:

Step | What to do |

|---|---|

1. Define the finished product | Know exactly what the property should look like after renovation |

2. Find renovated comps | Use recently sold properties that resemble the finished version of your subject property |

3. Adjust for differences | Account for size, layout, bed/bath count, property type, garage, lot, condition, and location |

4. Review buyer pool | Compare properties that would attract the same buyer or investor |

5. Use a conservative ARV | Leave room for appraisal, buyer negotiation, and market movement |

According to Fannie Mae’s comparable-sales guidance, the sales comparison approach should report at least three closed comparable sales. Current listings and contract offerings may help support the analysis, but they do not replace closed sales. Fannie Mae also says comparable sales from the last 12 months are generally preferred, although older sales may be used when they are the best available indicator and the appraiser explains why.

That point matters for investors. Active listings can show competition. Closed sales show what buyers actually paid. What most guides do not mention is that the investor’s comp set and the appraisal comp set may not match. An investor may focus on upside and renovation potential, while the appraisal has to stay tied to supported market evidence, property similarity, proximity, and closed-sale reliability. That difference can create a gap between the investor’s target ARV and the value used in the financing review.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

What Makes a Good ARV Comp?

A strong ARV comp should look like the finished version of your subject property. Use comps that match:

- Same property type

- Same or similar neighborhood

- Similar square footage

- Similar bedroom and bathroom count

- Similar renovation quality

- Similar lot size and parking

- Similar school zone or demand area

- Similar buyer pool

- Recent closed sale, preferably within the last 6 to 12 months

A renovated 5-bedroom multifamily property is not automatically a clean comp for a dated single-family home just because both sit in the same ZIP code. A property across a major road, in a different school district, near a different commercial corridor, or serving a different buyer pool can trade differently.

The practical test is this:

Would the same buyer realistically compare these two properties before making an offer?

If the answer is no, the comp is weak.

Ziffy Deal Screen: Estimating ARV Before You Make an Offer

As of May 2026, Ziffy’s 141 Main St listing gives us a practical way to show what investors should collect before estimating ARV. The property is listed at $289,000, and Ziffy’s property data identifies it as a 5-bedroom, 2-bath, 2,333 sq. ft. multifamily property built in 1920 in Castalia, OH.

Those details are useful because ARV analysis starts with the subject property. Before an investor can estimate the finished value, they need to understand the property type, size, likely buyer pool, renovation scope, and whether the finished asset should be compared against renovated multifamily sales, single-family conversions, or other income-producing properties in the same market.

At this stage, the listing price is not the ARV. It is the starting point for the analysis. The investor still needs closed renovated comps, inspection findings, contractor pricing, permit review, holding-cost estimates, resale assumptions, and lender review before deciding whether the deal has enough spread.

That gives the investor a cleaner question:

If this property is renovated to the right condition for the local market, does the finished value leave enough room after repairs, financing, selling costs, and profit?

For the calculation below, we are using a separate hypothetical rehab scenario to show how the ARV screen works. These numbers are not a valuation of the 141 Main St listing.

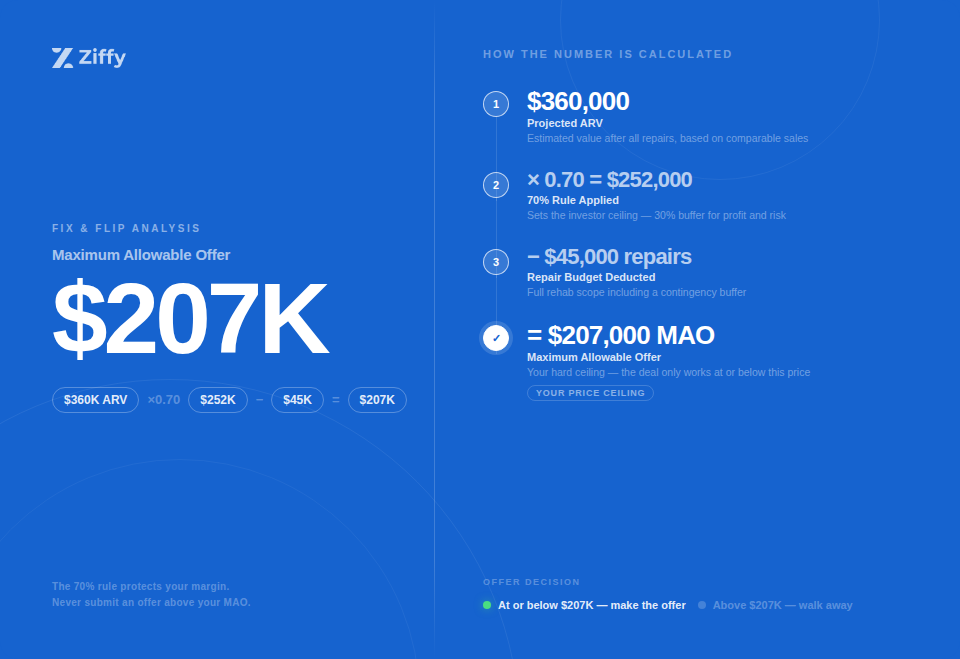

Suppose an investor is reviewing a rehab property where three closed renovated comps support a conservative finished value of $360,000. The contractor bid is $45,000. Before making the offer, the investor uses the 70% rule as a first-pass screen.

Input | What to do |

|---|---|

Projected ARV | $360,000 |

70% of ARV | $252,000 |

Estimated repairs | $45,000 |

Maximum allowable offer | $207,000 |

In this simplified screen, the maximum allowable offer would be $207,000 using the 70% rule.

That does not automatically mean the property is a bad deal. It means the investor needs a stronger reason to go above the 70% rule, such as lower actual repairs, stronger comps, a rental-hold exit, seller concessions, a faster resale timeline, or a value-add plan that materially changes the income and value profile.

The goal is not to force every property into the 70% rule. The goal is to avoid treating ARV like a hopeful resale price.

This example is for educational purposes only and is not a recommendation to buy this property. Final ARV depends on closed comparable sales, verified renovation scope, contractor pricing, inspection findings, market conditions, and lender review.

The 70% Rule for ARV

The 70% rule is a fast screening tool used by many flippers.

Maximum Allowable Offer = 70% of ARV minus repair costsFor example:

Item | Amount |

|---|---|

Estimated ARV | $360,000 |

70% of ARV | $252,000 |

Estimated repairs | $45,000 |

Maximum allowable offer | $207,000 |

The 30% cushion is not pure profit. It has to absorb several costs that can move quickly during a rehab project:

- Selling costs: Agent commissions, transfer costs, and seller-paid concessions reduce net proceeds

- Financing costs: Interest, points, and fees reduce the final return

- Holding costs: Taxes, insurance, utilities, and maintenance continue during the project

- Repair contingency: Older properties often produce scope changes after inspection or demolition

- Profit margin: The investor still needs enough return to justify the project risk

This is why a deal can look strong on the purchase price and still fail the ARV screen. The spread has to survive the full project, not just the acquisition.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

How ARV Affects Fix-and-Flip Financing

ARV is one of the most important numbers in a flip loan file.

When you apply for a fix and flip loan, Ziffy reviews the property, purchase price, renovation plan, borrower profile, exit strategy, and projected finished value. ARV helps determine whether the requested loan amount makes sense against the completed asset.

Loan amounts, rates, leverage, fees, and terms are subject to change and depend on borrower qualifications, property eligibility, project scope, after-repair value, market conditions, and underwriting review.

A stronger ARV can support a cleaner file, but only when the repair budget and comps are credible.

A weak ARV creates three problems:

- The loan amount may come in lower than expected.

- The required cash contribution may increase.

- The exit strategy may look less reliable.

To be clear, a higher investor-estimated ARV does not automatically create a higher loan amount. The file still has to work on supported value, renovation scope, borrower liquidity, property eligibility, and exit strategy. If the appraisal or review process supports a lower finished value, the loan structure may need to change.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

That is also where liquidity matters. Investors should review cash reserves for investment property loans before assuming the repair budget and loan proceeds will cover every project cost.

ARV vs As-Is Value

As-is value is what the property is worth in its current condition. ARV is what the property may be worth after the planned renovation is complete.

Metric | Meaning | Used for |

|---|---|---|

As-is value | Current market value before improvements | Purchase review and current collateral valued |

Repair budget | Cost to bring the property to the target condition | Rehab planning and financing review |

ARV | Estimated value after repairs | Flip analysis, resale planning, loan sizing |

Net profit | ARV minus all project costs | Investor return analysis |

The distinction here is that as-is value and ARV answer two different questions. As-is value helps frame the current collateral position. ARV helps frame the completed-value and exit conversation. A deal can look reasonable against the as-is price and still fail if the completed value does not support the repair budget, financing structure, and exit plan.

ARV vs Cap Rate vs Cash Flow

ARV is mainly a renovation and exit-value metric. It tells you what a property may be worth after the planned improvement work is complete. Cap rate and cash flow are hold metrics. They tell you how the asset performs as a rental.

Use the right metric for the strategy:

Strategy | Primary metrics |

|---|---|

Fix and flip | ARV, repair budget, maximum allowable offer, profit margin |

BRRRR | ARV, refinance value, DSCR, capital left in the deal |

Long-term rental | Cash flow, DSCR, cap rate, financing structure |

Short-term rental | Revenue stability, local rules, DSCR, operating margin |

For a flip, start with a conservative ARV estimate and then use Ziffy’s Fix and Flip Calculator to see what the project may actually return after repairs, holding costs, financing costs, and selling costs.

For a rental hold, ARV still matters, but it should not be the only number driving the decision. Once the property is repaired and stabilized, use Ziffy’s Cap Rate Calculator to check the property’s unlevered return and Ziffy’s Cash-on-Cash Calculator to see how the deal performs against the actual cash invested. You can also use Ziffy’s guide to cash-on-cash return in real estate to understand how leverage changes the return picture.

For a BRRRR strategy, ARV matters because it can affect the refinance value and how much capital you may be able to recover after the rehab. The rental side still has to work, especially if the exit plan is refinancing an investment property into a DSCR loan after the property is leased. Investors should also review DSCR loan requirements before assuming the refinance will qualify.

If the investor wants to refinance and pull capital back out after the rehab, the exit may also involve a DSCR cash-out refinance. In that case, ARV still matters, but the refinance also depends on rental income, PITIA, leverage, borrower profile, reserves, and property eligibility.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

Common ARV Mistakes That Can Break a Rehab Deal

Mistake 1: Using Active Listings as Proof of Value

Active listings show seller expectations. Closed sales show buyer behavior. You can use active listings to understand competition, but they should not carry the final ARV estimate.

Mistake 2: Comparing the Property in the Wrong Condition

ARV should be based on the finished version of your property, not its current condition. If your renovation plan is cosmetic, do not compare it to a fully rebuilt home with new systems, new layout, premium finishes, and a different buyer pool.

Mistake 3: Overvaluing High-End Finishes

Luxury finishes do not always create luxury resale value. In many mid-market neighborhoods, buyers will pay for clean, functional, move-in-ready condition. They may not pay enough extra for premium tile, custom cabinetry, or designer lighting to justify the cost. The finished product should match the market, not your personal taste.

Mistake 4: Ignoring Square Footage Differences

A 2,900-square-foot comp can make a 2,100-square-foot subject look better than it is. Price per square foot can help you screen, but it should not replace a full comp review. Layout, bedroom count, lot size, parking, condition, and buyer demand can move value significantly.

Mistake 5: Using Comps From the Wrong Buyer Pool

Investor-heavy areas and owner-occupant-heavy areas can price differently. A landlord buying for yield and a family buying a renovated home may not value the same features equally. This is especially important when your exit is resale instead of refinance.

Mistake 6: Treating ARV Like a Fixed Number

ARV can move during the project. Rates can change. Buyer demand can soften. Inventory can rise. Insurance costs can shift buyer affordability. A six-month renovation in a changing market needs more cushion than a light cosmetic project with a quick resale timeline.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

Quick ARV Checklist Before You Make an Offer

Before submitting an offer on a rehab property, confirm these items:

Question | Why it matters |

|---|---|

Do I have three closed renovated comps? | ARV needs market proof |

Are the comps similar in size, layout, property type, and condition? | Weak comps inflate value |

Is the renovation budget based on a contractor bid? | Guessing repairs can destroy margin |

Have I included permits, inspections, and contingency? | Small misses add up fast |

Does the 70% rule leave enough room? | Thin deals break quickly |

Have I included holding and selling costs? | Profit is not just resale price minus purchase price |

Is my exit a flip, refinance, or rental hold? | The metric stack changes by strategy |

Can the property qualify for financing? | Strong ARV does not fix a weak file |

Does the deal still work if ARV comes in lower? | Downside cushion protects the project |

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

When ARV Supports the Deal

A strong ARV is useful only when the rest of the deal supports it. A project becomes more financeable when:

- The purchase price is meaningfully below supported ARV

- Renovation costs are documented and realistic

- The scope matches the target resale market

- The exit timeline is practical

- The borrower has enough liquidity for overruns

- Comparable sales support the finished value

- The deal still works if ARV comes in lower than expected

If those pieces line up, the next step is to run the full cost stack in Ziffy’s Fix and Flip Calculator.

If the project still works after repair costs, financing costs, holding costs, and selling costs, review Ziffy’s fix and flip loan options before making the offer.

Final Thoughts

ARV is not a perfect prediction of what a property will sell for after renovation. It is a disciplined estimate that helps you decide whether the risk, repair budget, financing cost, and exit plan make sense before you commit to the deal.

The strongest ARV analysis starts with recently sold renovated comps, not active listings or best-case resale assumptions. From there, the deal needs to leave enough room for repairs, holding costs, selling costs, financing costs, and a profit margin that still works if the final value comes in lower than expected.

For a flip, ARV helps you decide whether the purchase price leaves enough spread after renovation. For a BRRRR or rental-hold strategy, ARV still matters, but it should be reviewed alongside rent potential, cap rate, cash-on-cash return, DSCR, reserves, and the refinance path.

The practical takeaway is simple: do not use ARV to justify a deal you already want to buy. Use it to test whether the deal deserves the offer in the first place. If the comps, repair budget, and exit plan all support the number, the next step is deeper analysis through Ziffy’s Fix and Flip Calculator, Cap Rate Calculator, Cash-on-Cash Calculator, or financing review for a fix and flip loan.

FAQs

What does ARV mean in real estate?

ARV means after-repair value. It is the estimated market value of a property after renovations are completed.

How do you calculate ARV?

You calculate ARV by reviewing comparable renovated properties that recently sold near the subject property, adjusting for differences like size, condition, layout, lot, property type, and location, then estimating where your completed property would likely sell.

What is the 70% rule in flipping?

The 70% rule says a flipper should generally pay no more than 70% of ARV minus repair costs. It is a screening rule, not a guarantee of profit.

Is ARV the same as appraisal value?

No. ARV is your estimate of the finished property value. The appraisal is a third-party valuation completed during the lending process. If the appraisal comes in lower than your ARV estimate, your loan amount, cash requirement, or profit assumptions may change.

Can I use active listings to estimate ARV?

You can use active listings as supporting context, but they should not drive your final ARV. Closed comparable sales are stronger because they show completed buyer behavior.

Does ARV matter for DSCR loans?

ARV matters most for flip and BRRRR strategies. For a stabilized rental purchase, DSCR matters more because the loan is based on the property’s rental income relative to PITIA. If you plan to renovate and then refinance into a DSCR loan, ARV becomes important because it can affect the refinance value.

What is a good ARV spread?

A good ARV spread gives you enough room for repairs, financing costs, holding costs, selling costs, price reductions, and profit. Many investors use the 70% rule as a first screen, but the right spread depends on the project, market, exit timeline, renovation risk, and financing structure.

Should I review ARV before applying for an investment property loan?

Yes, if the property needs repairs or the exit depends on a higher post-renovation value. For stabilized rentals, the financing review usually leans more heavily on income, DSCR, borrower profile, and property eligibility. For rehab-heavy deals, ARV becomes more important because it can affect the exit plan, refinance value, or fix-and-flip loan structure. Investors comparing financing paths can also review Ziffy’s investment property loans guide before choosing a loan type.