Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Quick Answer: What Is Depreciation Recapture on Rental Property?

Depreciation recapture is the tax rule that applies when you sell a rental property after claiming depreciation deductions. While depreciation can lower your taxable rental income during ownership, the IRS generally requires that depreciation to be “recaptured” at sale. For residential rental property, the depreciation portion of your gain is usually taxed as unrecaptured Section 1250 gain, at a maximum 25% federal rate. The rest of the gain is generally taxed under long-term capital gains rules.

A sale can trigger depreciation recapture. A properly structured 1031 exchange can defer it. A DSCR cash-out refinance can help you access equity without selling, which means no sale-side recapture event at the time of refinancing. Before choosing between selling, exchanging, or refinancing, investors should ask their CPA to calculate adjusted basis, depreciation allowed or allowable, and estimated federal and state tax due at sale.

A rental property can look highly profitable until the tax estimate lands. You may have bought the property years ago, claimed depreciation each year, and watched the value climb. Then your certified public accountant (CPA) mentions depreciation recapture, and the sale proceeds look different from what you expected.

Depreciation lowered your taxable rental income while you owned the property. At sale, the IRS does not treat those deductions as permanently forgiven. The depreciation portion of your gain is carved out and taxed separately as unrecaptured Section 1250 gain, at a maximum 25% federal rate. The remaining appreciation gain is generally taxed under long-term capital gains rules, depending on your taxable income.

Selling is not the only path. A 1031 exchange can defer eligible gain and recapture by rolling proceeds into a replacement property. A Debt Service Coverage Ratio (DSCR) cash-out refinance can help you access equity without creating a sale. In some cases, an installment sale may also belong in the CPA conversation, especially when the investor wants to spread payments over time.

Table of Contents

What Depreciation Recapture Actually Is

The number that drives the tax calculation is your adjusted cost basis, not the sale price. For a residential rental property, the building portion is generally depreciated using the straight-line method over 27.5 years under the General Depreciation System. Land is not depreciable, so your purchase price must be split between land and building basis before annual depreciation is calculated.

Adjusted Cost Basis = Purchase Price + Capital Improvements – Total Depreciation Allowed or Allowable

If you bought a rental for $350,000 and claimed $81,455 in depreciation, your basis is no longer $350,000. Assuming no capital improvements or selling-cost adjustments in this simplified example, your adjusted basis is $268,545.

The gap between the sale price and adjusted basis is your total taxable gain. The portion tied to depreciation is separated from the appreciation gain and taxed under recapture rules.

A pattern we see in investor conversations is that owners sometimes compare the sale price with the original purchase price and stop there. That misses the basis reduction created by depreciation. The IRS generally calculates recapture on depreciation that was allowed or allowable, not only depreciation you actually claimed. Skipping depreciation deductions does not automatically protect your basis.

Ziffy’s rental analysis can help you model cash flow, yield, DSCR, and return on investment (ROI) while you hold a rental. The exit-side ROI still needs the tax picture. If you are deciding whether to sell, refinance, or exchange, use your depreciation schedule from your CPA alongside Ziffy’s rental property ROI calculator and rental property calculator guide.

How Is Depreciation Recapture Calculated

Assume you purchased a rental property for $350,000. Your closing documents allocate $70,000 to land and $280,000 to the building. Since land is not depreciable, you depreciate only the $280,000 building basis over 27.5 years. That gives you annual depreciation of roughly $10,182.

After eight years, you have claimed about $81,455 in depreciation. You then sell the property for $480,000. To keep the example clean, these figures do not include capital improvements, depreciation convention adjustments, selling expenses, state taxes, or closing-cost basis adjustments. Your CPA would apply those before filing.

The $81,455 depreciation tranche is the recapture exposure. It is taxed at a maximum 25% federal rate as unrecaptured Section 1250 gain. The remaining $130,000 is generally taxed under long-term capital gains rules, which may be 0%, 15%, or 20% depending on taxable income and filing status.

Higher-income investors may also need to account for the 3.8% Net Investment Income Tax (NIIT). For individual taxpayers, the IRS threshold is $200,000 for single filers and heads of household, $250,000 for married filing jointly and qualifying widow(er) filers, and $125,000 for married filing separately.

In our experience, the surprise is rarely the existence of tax, but at how much of the gain sits in the recapture tranche before the long-term capital gains calculation begins.

Form 4797 is the IRS form used to report sales of business property, including the sale or exchange of property and certain depreciation recapture items. Investors should not try to complete that reporting based on a rough sale estimate. Your CPA needs the depreciation schedule, closing statement, improvement history, and ownership structure before the final tax number is reliable.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

Investors sometimes tell us they never claimed depreciation, so they assume there is nothing to recapture. That is usually not how the IRS looks at it. The question is what depreciation was allowed or allowable. Before you list the property, get the depreciation schedule from your CPA so the sale estimate is based on the real adjusted basis.

How Cost Segregation Changes Your Recapture Estimate

Cost segregation moves depreciation into earlier years. It can increase the tax benefit during the hold period, and it can also raise the recapture calculation at sale.

Instead of depreciating the entire building structure over the standard residential rental schedule, a cost segregation study may identify shorter-life components, such as certain personal property or land improvements. Those categories can create larger deductions earlier in the ownership period. When the property is sold, the earlier deductions need to be reviewed by category.

Section 1250 generally applies to depreciable real property. Unrecaptured Section 1250 gain is taxed at a maximum 25% federal rate. Section 1245 property, often tied to personal property categories, can be recaptured as ordinary income. IRS Publication 544 explains the tax rules that apply when property is sold, exchanged, or otherwise disposed of.

If a cost segregation report moved part of the property into personal property categories, your CPA may need to separate the recapture estimate between Section 1250 and Section 1245 treatment. A simple “25% on all depreciation” estimate may understate the exposure.

The IRS states that for most qualifying business property bought and put into use after January 19, 2025, businesses can deduct 100% of the cost in the first year. That makes accelerated depreciation more powerful for eligible assets, but it also increases the need for pre-sale tax modeling.

The first-year tax savings from a cost segregation study can be real, especially when bonus depreciation applies. The issue is what happens at sale. If a large part of the deduction came from personal property categories, the recapture estimate can look very different from the simple 25% number investors hear online.

If most of your exposure falls under Section 1245, the exit strategy may change. You may decide to hold longer, plan a 1031 exchange, or compare the original tax savings against the ordinary-income recapture exposure before selling. Cost segregation works best when the exit math is built into the original strategy before the study is commissioned.

For a broader tax planning view before you list, read Ziffy’s guide to real estate taxes investors need to plan before buying.

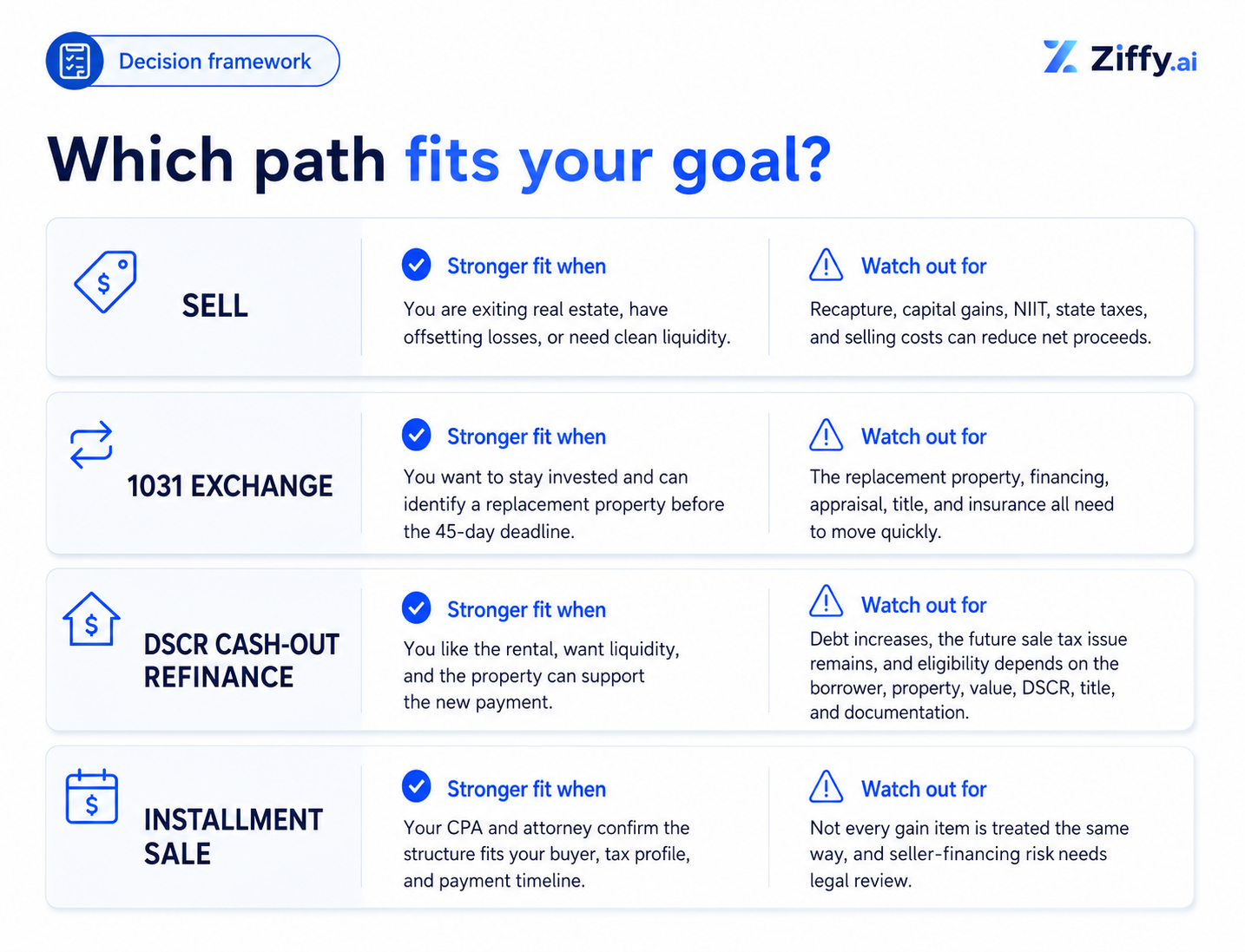

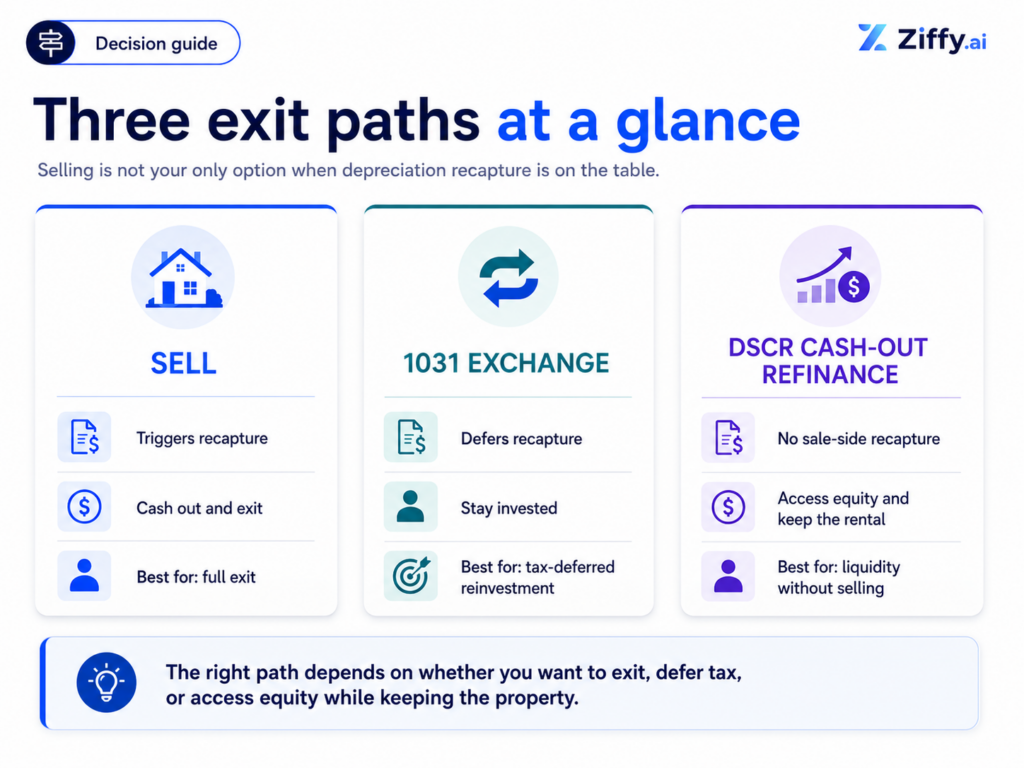

The Main Exit Paths When Recapture Is Looming

A property with a large built-in gain does not automatically need to be sold. Most investors compare three primary paths: sell, exchange, or refinance. An installment sale can also be reviewed with a CPA and attorney, but it sits outside the main financing decision because it depends heavily on buyer terms, seller-financing risk, payment timing, and legal structure.

If you are done with the asset and want clean liquidity, selling is the most direct answer. You pay the recapture tax, pay capital gains on the appreciation, and walk away with net proceeds. This can be the right move if you are leaving real estate, have offsetting losses, or no longer want to manage the property.

A 1031 exchange defers eligible tax by rolling proceeds into a replacement property, as long as the exchange is structured correctly. The replacement property must be identified within 45 days after transferring the relinquished property, and it must generally be received within 180 days or by the tax return due date with extensions, whichever comes first.

The option many tax articles skip is the one where you never leave the asset. If your real goal is liquidity, not a full exit, a DSCR cash-out refinance can help you access equity without creating a sale. You still own the property, carry the debt, and need the rental to support the payment, which is exactly what DSCR qualification analyzes.

Ziffy’s DSCR cash-out refinance can go up to 75% loan-to-value (LTV) on eligible files. LTV means the loan amount as a percentage of the property’s value. Using the $480,000 value from the earlier example, 75% LTV would support a maximum total loan amount of $360,000 before subtracting the existing loan payoff, closing costs, and any program-specific adjustments.

If you sell later, your CPA will still calculate the tax impact using the property’s basis, depreciation history, sale price, and transaction details. The refinance simply avoids creating a sale-side recapture event at the time you access equity.

Ziffy’s DSCR cash-out refinance is built around the rental property’s income, not a W-2 income file. That helps investors whose tax returns do not fully reflect the property’s rental strength. Review Ziffy’s DSCR loan requirements and broader investment property financing options before making a sell-or-refinance decision.

This decision also affects long-term return planning. If the refinance proceeds are used to improve the property, buy another rental, or continue a BRRRR-style reinvestment strategy, compare the new debt payment against projected rent, cash flow, reserves, and cash-on-cash return.

When an investor says they want to sell because they need cash, I like to separate the two decisions. Do they want out of the property, or do they want the equity? If they still like the rental, a DSCR cash-out refinance can be the cleaner conversation.

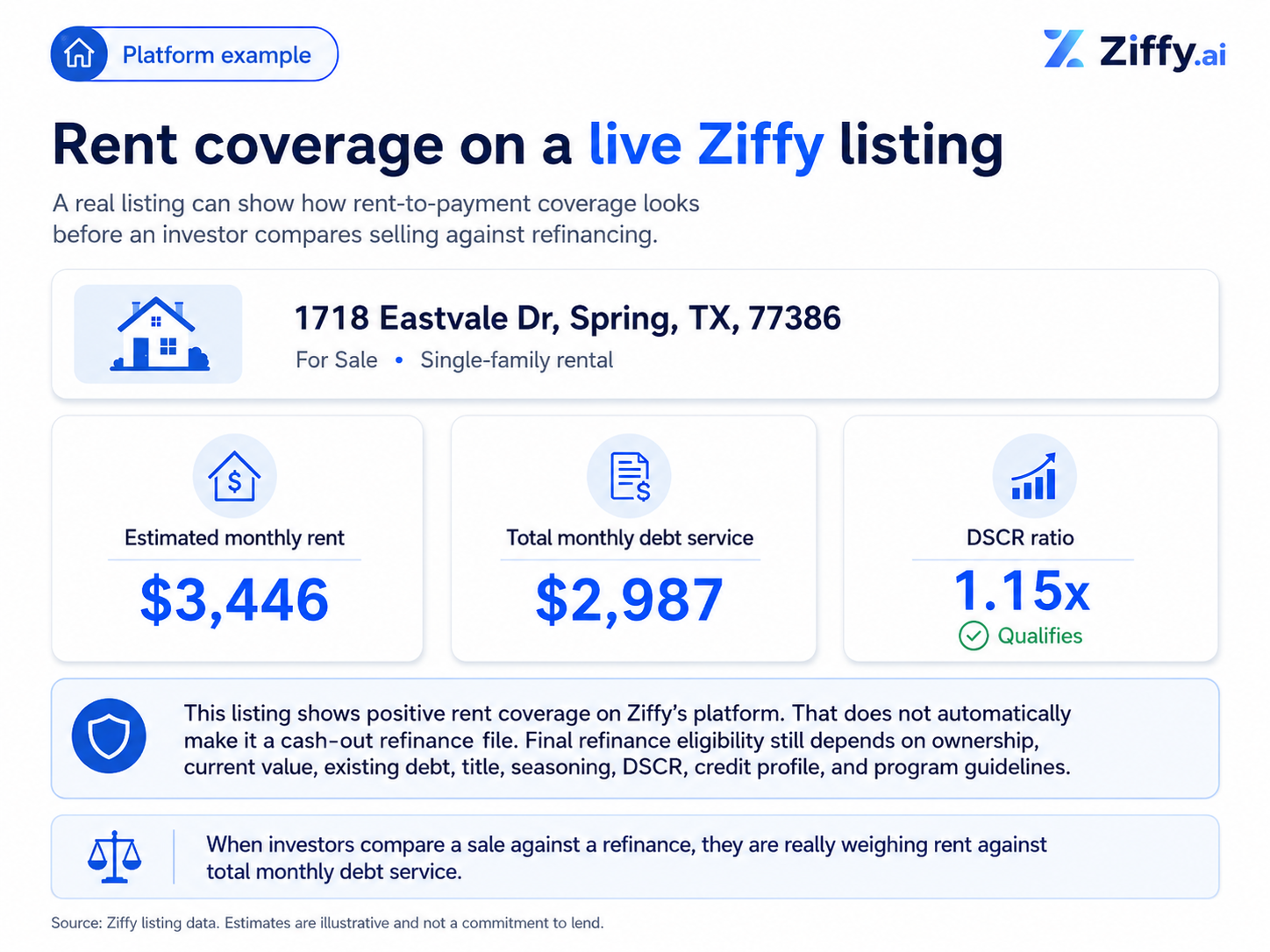

What Rent Coverage Looks Like on a Live Property

To understand the sell-versus-refinance decision, take 1718 Eastvale Dr in Spring, TX, a single-family rental listed on Ziffy. The property shows $3,446 in estimated monthly rent against $2,987 in total monthly debt service, producing a 1.15x DSCR.

That rental coverage is useful context for investors comparing a taxable sale against a refinance. It shows how the property’s income lines up against the projected payment, which is the core question in DSCR underwriting, but that does not make it automatically eligible for a cash-out refinance.

A cash-out refinance would still depend on the investor already owning the property, current value, existing debt, title, seasoning, DSCR, credit profile, and program eligibility. But the rent-to-payment relationship shows the real comparison investors are making: whether the rental can support new debt well enough to justify keeping the asset instead of selling it.

A fourth option may also belong in the tax discussion: an installment sale under IRC Section 453. This can spread certain gain recognition over time when the buyer pays in installments. It is not a mortgage product and it requires CPA and legal review, but investors with large gains should know it exists before assuming the choice is only sell, exchange, or refinance.

When a 1031 Exchange Is the Right Move

A 1031 exchange works best when you want to stay invested and already have a credible replacement-property plan. Two common examples are upgrading into a larger rental that supports stronger cash flow, or consolidating two smaller rentals into one property that is easier to manage from a distance.

It is a bad fit when you need the cash personally. In a proper deferred exchange, the sale proceeds are handled through a qualified intermediary. Touching the proceeds can damage the exchange. It also becomes risky when the investor starts too late. The financing review, appraisal, title, insurance, and rental-income analysis all have to fit inside a deadline-driven transaction.

Financing readiness should start before the exchange clock begins. A DSCR loan is often the best-fit option for the replacement property because the underwriting is tied to rental income instead of a personal debt-to-income file. Ziffy’s DSCR process is built for investor purchases, including limited liability company (LLC) borrowers and rental-income-based qualification. Read our 1031 exchange rules and deadlines guide and use the 1031 exchange calculator before the sale contract is signed.

For investors working under the 1031 deadline, the cleaner path is usually to discuss financing before the relinquished property closes. Once the 45-day identification period begins, the investor has less room to solve appraisal issues, insurance delays, title problems, rental income qualification gaps, or property eligibility concerns.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

The financing conversation should happen before the exchange starts. If an investor waits until after the sale agreement is signed, the 45-day clock is already moving. Getting DSCR pre-qualified early gives them a cleaner path when the replacement property is identified.

Common Mistakes That Make Recapture More Expensive

The most expensive mistake is modeling sale proceeds from the purchase price and expected sale price without pulling the depreciation schedule first. The taxable calculation starts with adjusted basis. Without the depreciation schedule, capital improvement history, and estimated selling costs in hand, after-tax proceeds are still a guess.

The number I want investors to know before they list is not just the sale price. It is the adjusted cost basis. Once you know that, the rest of the decision gets much clearer because you can compare selling, exchanging, and refinancing with real numbers.

Skipped depreciation creates another problem as some owners assume they avoided recapture because they never claimed the deduction but the allowed-or-allowable rule usually prevents that. The investor may have missed the annual tax benefit and still face the sale-side basis adjustment.

Rushed 1031 exchanges create avoidable pressure. Selling first and then looking for the replacement property puts the entire transaction under the 45-day identification clock. If the investor identifies a property that cannot be financed, needs repairs that do not fit the loan file, or fails the rental-income test, the exchange can become a scramble.

Capital gains and recapture also get mixed together too often. The 0%, 15%, and 20% long-term capital gains rates apply to the appreciation tranche based on taxable income. The depreciation tranche is separate and can be taxed at a maximum 25% federal rate as unrecaptured Section 1250 gain. Higher-income taxpayers may also need to account for NIIT.

Use This Decision Framework Before You List – The Main Exit Paths

A large recapture estimate does not automatically mean you have to sell and absorb the tax bill right away. It means the sale has to be compared against the other ways an investor can move capital, reduce management burden, or access equity.

If you are done with the property, need liquidity, or want to step away from real estate altogether, selling may still be the right decision. The tradeoff is that the sale creates the taxable event. Depreciation recapture, capital gains, state taxes, NIIT, selling costs, and loan payoff all reduce the amount you actually keep.

A 1031 exchange is usually a better fit when you still want to own investment real estate but no longer want this specific property. Instead of taking the proceeds personally, the sale funds move through a qualified intermediary and into a replacement property. That can defer eligible recapture and capital gains, but the timeline is tight. The replacement property has to be identified within 45 days, and the purchase generally has to close within 180 days. That is why financing should be discussed before the relinquished property closes, not after the clock starts.

A DSCR cash-out refinance is a different conversation because there is no sale. If you still like the rental but want to access equity, refinancing can help you pull cash out while keeping the property in your portfolio. There is no sale-side depreciation recapture at the time of refinance, but the property has to support the new payment. The loan review still depends on the property’s value, existing debt, title, seasoning, DSCR, credit profile, and program eligibility.

Ziffy can help you review DSCR financing for both cash-out refinances and 1031 replacement-property purchases. Read the full DSCR loan guide or request a DSCR rate quote to compare the financing path against your after-tax sale estimate.

FAQs

What is the depreciation recapture tax rate for rental property?

Unrecaptured Section 1250 gain from selling depreciable real property is taxed at a maximum 25% federal rate. The remaining long-term capital gain is generally taxed under the 0%, 15%, or 20% capital gains structure, depending on taxable income. This is general information only. Your CPA can determine how the rules apply to your property, filing status, income, and ownership structure.

Can I avoid depreciation recapture entirely?

Usually, you cannot make recapture disappear after a taxable sale. You may be able to defer it through a properly structured 1031 exchange. If you keep the property and use a DSCR cash-out refinance instead of selling, you avoid triggering sale-side recapture at that time. This does not eliminate future tax exposure if you sell later without another deferral strategy. Review the structure with a CPA before making a tax-driven decision.

What happens if I never claimed depreciation on my rental?

The IRS generally considers depreciation that was allowed or allowable. That means skipped depreciation may still reduce basis at sale. Ask your CPA whether you need to correct prior depreciation treatment before selling.

Does a 1031 exchange eliminate depreciation recapture?

No. A 1031 exchange generally defers eligible gain and recapture. The deferred tax carries into the replacement property’s basis and becomes relevant again when the replacement property is sold without another deferral strategy. This is general information only. Your CPA can confirm how the deferred gain carries into your replacement property.

Is a DSCR cash-out refinance taxable?

A DSCR cash-out refinance is not a sale, so it does not trigger depreciation recapture by itself. The investor is borrowing against equity and must repay the loan. The tax treatment of interest, proceeds, and future sale gain should still be reviewed with a CPA. This is general information only.

Does the recapture rate change based on my income?

The maximum federal rate for unrecaptured Section 1250 gain is 25%, but the rest of your gain may be taxed at long-term capital gains rates based on taxable income. Higher-income taxpayers may also owe the 3.8% Net Investment Income Tax. For individual taxpayers, the IRS threshold is $200,000 for single filers and heads of household, $250,000 for married filing jointly and qualifying widow(er) filers, and $125,000 for married filing separately. Your CPA can calculate whether NIIT applies to your sale.