Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Quick Answer: What is a 1031 Exchange?

A 1031 exchange helps real estate investors defer taxes when they sell one qualifying investment property and buy another. The structure can preserve more equity for the replacement property, but the deadlines, qualified intermediary rules, debt replacement, and financing timeline need to be planned before the relinquished property closes.

A 1031 exchange lets investors defer capital gains tax and depreciation recapture when they move from one qualifying investment or business-use real property into another qualifying real property.

The 45-day identification deadline and 180-day closing deadline control the exchange timeline. For some sellers, the tax-return due date can shorten the 180-day window.

The sale proceeds cannot pass through the investor’s hands. A qualified intermediary must be in place before the relinquished property closes.

Boot does not automatically ruin the exchange, but it can make part of the gain taxable. Cash boot and mortgage boot need to be reviewed before the replacement property closes.

Before you list a relinquished property, a 1031 exchange has to answer two questions: how much equity can be preserved for the next acquisition, and whether the replacement property can support the financing structure you plan to use.

When you sell an appreciated rental or business-use property, the tax bill may include depreciation recapture and the 3.8% Net Investment Income Tax for higher earners. State tax can add another layer, depending on where the property is located.

As of June 2026, Section 1031 applies only to qualifying real property held for investment or productive use in a trade or business. Personal property no longer qualifies for 1031 treatment under current rules. The IRS also says real property held primarily for sale does not qualify as a like-kind exchange.

For Ziffy investors, the exchange decision should start before the property is listed. Use Ziffy’s 1031 Exchange Calculator to estimate the replacement target and check possible boot exposure before the 45-day clock starts.

Table of Contents

What Is a 1031 Exchange?

A 1031 exchange, also called a like-kind exchange, is a tax-deferral strategy under Internal Revenue Code Section 1031. It allows an investor to exchange one qualifying real property for another qualifying real property without recognizing gain at the time of the exchange, as long as the IRS rules are followed.

The relinquished property and replacement property must be held for investment or productive use in a trade or business. A primary residence does not qualify. A fix-and-flip property held primarily for resale usually does not qualify either because the IRS may treat it as inventory.

A 1031 exchange defers tax. The deferred gain carries into the replacement property through basis adjustments. For long-hold investors, that basis treatment can affect future sales and estate planning.

- You sell the relinquished property.

- The qualified intermediary holds the proceeds.

- You identify replacement property within 45 calendar days.

- You close on the replacement property within 180 calendar days, subject to the tax-return filing cap.

- You report the exchange on Form 8824.

The IRS uses Form 8824 to report each exchange of business or investment property for property of a like kind.

A 1031 can defer both capital gains tax and depreciation recapture that would otherwise apply on a taxable sale. Review depreciation recapture early, especially on long-held rentals where years of deductions may have built up.

Ziffy’s 1031 Exchange Calculator shows preserved equity and the required replacement value. It also helps you see where boot exposure may appear before the deal is already in motion.

Why Investors Use 1031 Exchanges

Preserve equity and move it into a stronger market

The main appeal of a 1031 exchange is simple: more sale equity can stay available for the next property. That preserved equity may support a larger down payment or a replacement property with better long-term income potential.

For investors financing the replacement property, a Debt-Service Coverage Ratio (DSCR) loan uses the property’s rental income to qualify the deal. When the replacement timeline is tight, that rental-income-based path can be more practical than building the loan around personal tax returns.

Move from scattered rentals into a more efficient property

A 1031 exchange can help an investor move from one single-family rental into a small multifamily property, or from scattered rentals into a tighter operating footprint. The goal is usually simpler management or better rent concentration.

In that situation, the replacement property and the financing have to be evaluated together. Ziffy’s investment property loans guide explains the broader financing options, whereas the DSCR loan guide is the cleaner starting point when rental income will drive the loan file.

Adjust the portfolio without taking the full tax hit immediately

In our experience, investors often outgrow the property mix they started with. One investor may want fewer roofs and more units under one address. Another may want to split one appreciated rental into multiple replacement properties in different markets.

The identification rules can support either direction if the replacement list is structured correctly. The risk is waiting too long to make those choices. Once the relinquished property closes, the investor has 45 calendar days to identify replacements in writing.

Plan for a longer holding strategy

Some investors use 1031 exchanges as part of a long-horizon strategy often called “swap till you drop.” They exchange into stronger assets over time and hold until death, when inherited-property basis rules may reset basis to fair market value.

The exchange structure, debt, estate plan, and state tax exposure should be reviewed together before the investor relies on that strategy.

The Four Types of 1031 Exchanges

1. Delayed exchange

A delayed exchange is the standard structure most investors use. You sell first, the qualified intermediary holds the proceeds, you identify replacement property within 45 days, and you close within 180 days.

2. Reverse exchange

A reverse exchange flips the order. You acquire the replacement property first, then sell the relinquished property.

The safe-harbor structure comes from Rev. Proc. 2000-37, which allows an Exchange Accommodation Titleholder, or EAT, to park property during the exchange period. The IRS revenue procedure explains the safe harbor for certain arrangements between taxpayers and exchange accommodation titleholders.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

When clients ask which exchange type fits, timing usually answers the question. If the replacement property shows up first, a reverse exchange can keep the deal alive. The financing and title structure need to be planned before the buyer moves.

Reverse exchanges often need short-term capital because the investor buys before selling. Bridge loans can cover that timing gap when the replacement must close before the relinquished sale proceeds are available. In many files, the bridge loan is later paid off or refinanced once the sale side is complete.

3. Simultaneous exchange

A simultaneous exchange closes the sale and purchase on the same day. It still exists, but it is much less common now because most real estate transactions do not line up that neatly.

4. Improvement exchange

An improvement exchange, sometimes called a construction exchange, lets exchange proceeds go toward improvements on the replacement property during the exchange period.

The value the investor wants counted generally must be completed within the same 180-day window. These transactions require tight coordination because the intermediary, lender, title team, and contractor are all working inside the same exchange deadline.

The right 1031 exchange structure depends on timing. A delayed exchange is the standard path when the investor sells first and then buys the replacement property. A reverse exchange is more complex because the replacement property is purchased before the relinquished property is sold. Simultaneous exchanges work only when both closings line up on the same day, while improvement exchanges are better suited for value-add replacement strategies where exchange proceeds are used toward qualifying improvements.

The 1031 Exchange Timeline

1. Confirm eligibility before listing

Start with the relinquished property. It should be held for investment or productive business use. If the facts involve personal use or resale intent, get tax advice before listing. Mixed-use properties also need review before the sale process begins.

2. Engage the qualified intermediary before closing

A qualified intermediary must be in place before the relinquished property closes. If the sale closes and you receive or control the proceeds, the exchange is usually lost. This exchange is one of the IRS safe harbors designed to prevent the seller from being treated as having received the funds.

A pattern we’ve noticed is that first-time 1031 investors sometimes treat the intermediary as paperwork. The exchange structure has to be right before closing. If the proceeds are handled incorrectly, the replacement search may never matter.

3. Close the relinquished sale

Day 0 starts when the relinquished property transfers. The 45-day identification period and 180-day exchange period begin on that date. Both deadlines use calendar days.

4. Identify replacement property by Day 45

Sign the identification notice and deliver it in writing to the qualified intermediary or another permitted party by the deadline. The notice should be specific enough to satisfy the rule; a rough note will not protect the exchange.

Treat the identification notice as a closing document with specific property details and delivery proof.

5. Start financing before the sale closes

Financing pressure often starts earlier than investors expect. If the replacement loan conversation starts only after the relinquished property has already closed, the back half of the exchange becomes harder.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

In our experience, 1031 replacement files move better when financing starts while the relinquished property is still under contract. At that point, the investor still has room to adjust the target property, loan structure, and closing timeline.

For many investors, a DSCR loan is the cleanest fit for a 1031 replacement property because the loan qualifies the rental income instead of relying heavily on personal-income documentation. On the core DSCR path, Ziffy does not require W-2 employment documents or personal tax returns.

That product fit does not mean every replacement property will qualify. DSCR loans commonly require a meaningful down payment and reserves. The rental income must also support the payment. Review Ziffy’s DSCR loan requirements before the replacement search gets serious.

DSCR rates can price higher than some conventional investor loans. The tradeoff is documentation flexibility and a rental-income-based underwriting path, which can be valuable when the 1031 deadline is driving the file.

6. Complete due diligence without losing time

Inspection, appraisal, title review, insurance, lease review, and lender conditions still need full attention. A tight exchange timeline makes early underwriting more valuable, especially when the replacement property has insurance issues or appraisal questions.

7. Close by Day 180

The replacement property must be received by the earlier of 180 days after the relinquished property transfers or the due date of the tax return, including extensions, for the year of the transfer.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

When the file gets tight, investors usually lose time in ordinary places: appraisal, title, insurance, entity paperwork, or lender conditions. Ten lost days near the end of a 1031 exchange can change the whole deal.

8. Report the exchange on Form 8824

Form 8824 is required for reporting the exchange. Keep the qualified intermediary agreement, identification notice, closing statements, replacement-property documents, and financing records in the permanent file.

What Qualifies as Like-Kind Property?

For real estate, like-kind is broad. One qualifying US real property held for investment or business use can generally be exchanged for another qualifying US real property held for investment or business use.

The asset classes do not need to match. A single-family rental can be exchanged for multifamily, raw land, retail, industrial, or another commercial property. The use and tax treatment drive eligibility. IRS guidance says real properties are generally like-kind even when one is improved and the other is unimproved, but US real property and foreign real property are not like-kind to each other.

Short-Term Rentals, Vacation Homes, and DSTs

Short-term rentals need careful documentation. Rev. Proc. 2008-16 provides a safe harbor for dwelling units used as rental property and also used personally by the owner. The IRS describes the safe harbor as applying to rental property that is occasionally used for personal purposes and may qualify under Section 1031 when the safe-harbor requirements are met.

One thing that surprises investors is that an Airbnb can qualify, while a personal-use vacation property usually will not unless the rental history and personal-use records support the exchange. The 14-day and 10% limits need to be documented.

For short-term rental investors, the records need to support the tax position. The property may look like an investment, but the rental history and personal-use records still need to align with the safe-harbor standards.

A Delaware Statutory Trust, or DST, can be a passive 1031 replacement option in certain structures. Rev. Rul. 2004-86 explains how a Delaware Statutory Trust described in the ruling is classified for federal tax purposes and whether a taxpayer may acquire an interest in that trust without recognizing gain or loss under Section 1031.

A DST can fit investors who want passive exposure, but the trust structure must match the ruling. Tax counsel should review the structure before the investor assumes the DST qualifies.

The 45-Day and 180-Day Rules

The 45-day identification rule gives investors 45 calendar days from the transfer of the relinquished property to identify replacement property in writing. Weekends and holidays count.

Most investors use the three-property rule. Larger backup lists usually rely on the 200% rule. The 95% rule is rare because the acquisition requirement is strict.

The 180-day rule requires the investor to receive the replacement property by the earlier of 180 days after the relinquished property transfers or the due date of the tax return, including extensions, for the year of the transfer. Rev. Proc. 2000-37 also describes the 45-day identification deadline and the 180-day receipt deadline in the exchange context.

The year-end trap

A late-year sale can create a shorter exchange window than the calendar suggests.

Event | Date |

|---|---|

Relinquished property sold | December 15, 2026 |

Day 180 | Mid-June 2027 |

2026 tax return generally due | April 15, 2027 |

Without an extension, the exchange window can shrink to about 121 days instead of the full 180.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

Year-end files are where investors get blindsided. They remember the 180-day rule and forget the tax-return cap. That filing date can remove weeks from the exchange timeline.

7 Mistakes That Can Break a 1031 Exchange

- Receiving or controlling the proceeds. If the investor takes control of the money, the exchange can fail.

- Missing the 45-day identification deadline. There is no routine grace period. Late identification is usually fatal.

- Naming replacement properties too quickly. Weak backup choices can leave the investor with no workable replacement.

- Taking cash boot without planning for tax. Cash returned to the investor can be taxable.

- Under-replacing debt. If the debt side is not handled correctly, mortgage boot can create taxable exposure.

- Changing taxpayer or title structure too late. The taxpayer selling generally needs to be the taxpayer buying.

- Buying property that looks like resale inventory. If the facts point to a quick resale plan rather than investment intent, the exchange position becomes weaker.

A pattern we’ve noticed is that investors focus heavily on replacing equity and give less attention to the debt side. A clean 1031 file needs both parts of the capital stack planned before closing.

Boot and How to Avoid It

Boot is value received in an exchange that does not qualify as like-kind replacement value. It can make part of the gain taxable.

Cash boot

Cash boot is cash or other non-like-kind value received from the exchange. If you take money out instead of reinvesting it, that portion is generally taxable up to the amount of realized gain.

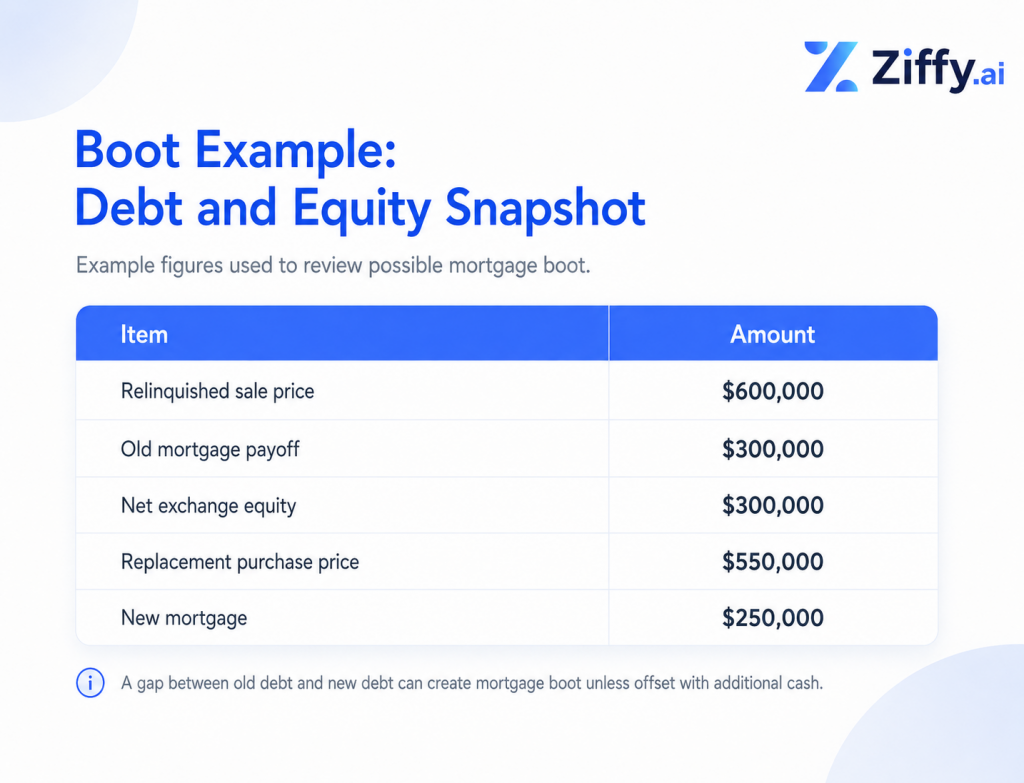

Mortgage boot

Mortgage boot can arise when debt on the relinquished property is not replaced on the acquisition side, unless the investor offsets the gap with additional cash.

In this example, the investor paid off $300,000 in old debt and replaced only $250,000 with new debt. The $50,000 gap can create mortgage boot unless the investor offsets it with additional cash or moves into a higher-value replacement structure that supports full deferral.

What we see often is that investors notice the equity target first and the debt-replacement issue later. That sequence can create avoidable boot exposure, especially when the replacement purchase price is lower than expected or the new loan amount comes in smaller after underwriting.

In our experience, full-deferral files are often easier when the investor trades up. A larger replacement property, planned early, gives the borrower more room to manage equity, debt, reserves, and closing costs.

Example Using Ziffy 1031 Calculator and Market Data

Ziffy’s 1031 Exchange Calculator helps estimate the replacement value needed for full deferral. It also shows how boot exposure can appear when equity or debt is not replaced correctly.

Investment Properties on Sale Today

What to Do Before You Start a 1031 Exchange

Before listing the relinquished property, open the 1031 calculator and test the replacement target. At that point, evaluate whether the replacement property can support the loan payment and post-closing cash needs.

Start with Ziffy’s 1031 Exchange Calculator to estimate the replacement value and review possible boot exposure. Then speak with your CPA and qualified intermediary before the sale closes.

If the replacement property needs long-term investor financing, begin the DSCR loan conversation while the relinquished property is still under contract. If the replacement needs to be purchased before the sale is complete, review bridge loan planning before committing to a reverse exchange.

FAQs

Can I do a 1031 exchange on a property I have owned for only six months?

There is no bright-line IRS holding-period rule that says six months always fails or always works. The IRS looks at investment intent and actual use. Documentation can make the position cleaner, especially when the holding period is short.

Do I need to reinvest 100% of the proceeds?

For full deferral, investors usually reinvest all exchange proceeds and replace the debt correctly. Taking cash out or under-replacing debt can create taxable boot.

Can I exchange one property for multiple properties?

Yes. A properly structured 1031 exchange can involve one relinquished property and more than one replacement property, as long as the identification and acquisition rules are followed.

Can I do a 1031 exchange into a property I already own?

Generally, no. A 1031 exchange is built around acquiring replacement property as part of the exchange. Property the investor already owns usually does not work as the replacement property.

What happens if I miss the 45-day deadline?

The exchange generally fails for tax-deferral purposes if the 45-day identification deadline is missed. The investor may still buy another property, but the sale of the relinquished property is likely treated as taxable.

Can DSCR financing be used for a 1031 replacement property?

Yes. DSCR financing can work well for a 1031 replacement property when the property is expected to generate rental income. Ziffy’s DSCR loan path focuses on rental income rather than building the file around personal tax returns.

Are DSCR loan rates higher than conventional loan rates?

DSCR loans can price higher than some conventional investor loans because they use a different underwriting structure. The tradeoff is often worth reviewing for 1031 investors who need a rental-income-based loan structure and a cleaner replacement-property timeline.

How much down payment do I need for a DSCR loan in a 1031 exchange?

Many DSCR investment-property loans require 20% to 25% down, depending on the property, borrower profile, loan amount, and DSCR. Check the exact requirement before the relinquished property closes because the down payment affects both financing approval and boot planning.

Does boot ruin the entire exchange?

Boot does not always ruin the entire exchange. It can make part of the gain taxable. Investors who want full deferral need to plan both equity replacement and debt replacement before closing.