Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

On paper, a Debt Service Coverage Ratio (DSCR) loan looks like one clean calculation: rental income divided by the property’s monthly payment. In practice, the lender’s review starts well before that number reaches underwriting.

The right DSCR lender reviews rent, projected housing costs, reserves, leverage, property use, ownership structure, and loan fit before the file gets expensive.

DSCR lending centers on the property’s income, so the analysis has to start with the property. A low advertised rate or flexible credit score minimum will not help much if the rent support comes in lower than expected, the insurance quote changes the payment, or the property falls below the lender’s DSCR threshold with no backup path.

At Ziffy, investors can search rental properties, review projected income, compare return on investment (ROI), and evaluate cash flow before moving into financing. Ziffy is built around one step: use the property numbers to determine whether the deal deserves a loan file.

Table of Contents

What Makes a DSCR Lender the Best Fit?

The best DSCR lender should help you answer three questions early:

- Can the rent support the monthly housing expense?

- Is there a financing path if the DSCR is below 1.00?

- Can the lender close the file with your timeline, reserves, and ownership structure?

Most lender comparison pages focus on minimum down payments and advertised rates, but neither number tells you whether the rent supports the payment.

For investors, the more useful questions are about rent support, taxes, insurance, homeowners association (HOA) dues, reserves, limited liability company (LLC) ownership, short-term rental income, and no-ratio DSCR options.

How DSCR Lenders Review a Rental Property

DSCR compares a rental property’s gross monthly rent to its monthly housing payment.

DSCR = Gross Monthly Rent ÷ Monthly PITIA

PITIA includes principal, interest, taxes, insurance, and association dues when applicable.

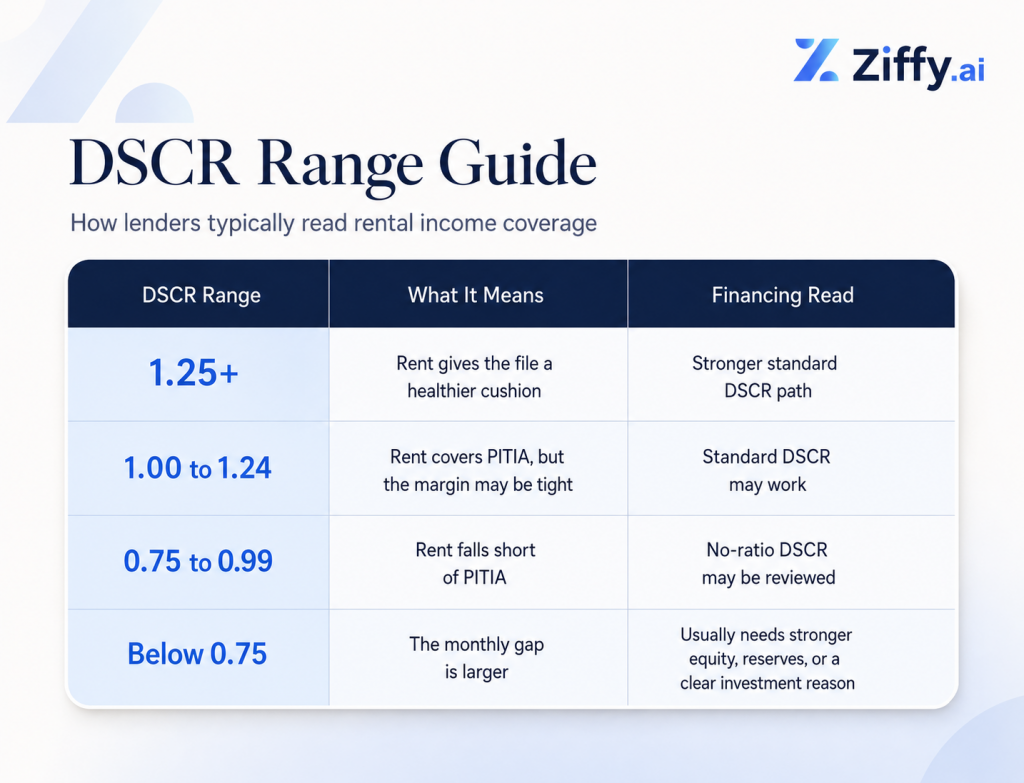

A 1.00 DSCR means the rent equals the monthly PITIA. A 1.25 DSCR means the property brings in 25% more rent than the monthly PITIA. A 0.85 DSCR means the rent covers 85% of the monthly payment.

Conventional loans usually focus on the borrower’s personal income and debt-to-income ratio (DTI). The CFPB defines DTI as monthly debt payments divided by gross monthly income. DSCR loans shift the primary income test to the rental property instead, which means that when we underwrite your DSCR loan, we check if the property can pay for itself.

Credit, reserves, down payment, documentation, and property eligibility still matter, but the difference is that a core DSCR file usually does not require W-2s, pay stubs, personal tax returns, or a personal DTI calculation.

For self-employed investors, borrowers with multiple financed properties, and buyers using an LLC, that structure can be much cleaner than trying to qualify an investment property through a conventional loan.

Standard DSCR vs. No-Ratio DSCR

Many DSCR lenders prefer a ratio of 1.00 or higher because the rent covers PITIA, but a property below that threshold can still have a financing conversation when the file has enough strength elsewhere.

At Ziffy, eligible properties below 1.00 may still be reviewed through no-ratio DSCR program. It means that even if the property does not meet the standard rent-coverage threshold (DSCR more than or equal to 1), the file may still be considered if the overall structure is strong enough.

No-ratio DSCR is a different review path for eligible investment properties where the rent does not fully cover PITIA, not a structure that glosses over weak income. In many cases, the file needs strength elsewhere, such as a higher down payment, lower loan-to-value ratio, stronger reserves, or a credible plan for the asset.

A 0.92 DSCR property and a 0.52 DSCR property are both below 1.00, but they do not tell the same story. One may be close enough to review with adjusted leverage. The other may require a much stronger reason to move forward.

The first thing we look at is not whether the DSCR is perfect. We look at what is driving the number. If insurance, taxes, or leverage are pushing the property below 1.00, there may still be a way to structure it. If the rent is simply too weak for the price, the investor needs to know that early.

What to Compare Before Choosing a DSCR Lender

A DSCR lender should not enter the process only after you have already chosen a property. By then, your inspection window may be moving, your earnest money may be committed, and the appraisal may become the first real test of whether the loan works.

1. Can the lender estimate DSCR before the full application?

A strong lender should help you review the property before you pay for an appraisal. That means looking at estimated rent, PITIA, cash flow, and likely DSCR before the file moves too far.

That is exactly what our AI-native investment search platform is built for. At Ziffy.ai, you can search rental properties, review projected income, compare cash flow, and use the DSCR loan calculator to test whether the property appears to support the financing.

Investment Properties on Sale Today

Powerful tools to help you identify the most profitable investment opportunities

2. Does the lender offer both standard DSCR and no-ratio DSCR?

A lender with one DSCR box may work for clean files, but real rental deals are not always clean.

Insurance premiums, property tax resets after purchase, and HOA dues can each pull down the DSCR independently. A property in a strong appreciation market may still land below 1.00 at current financing costs, even when the rent looks reasonable at first review.

No-ratio DSCR gives eligible below-1.00 properties a review path instead of ending the conversation at the threshold.

3. How does the lender verify rent?

The rent number drives the DSCR calculation, so it has to be supportable. Investors often begin with online estimates, seller projections, or expected future rent. Underwriting usually needs documented market rent support, not a borrower’s best-case projection.

A good lender should explain whether rent will be reviewed using a lease, market rent analysis, short-term rental history, appraiser-supported rent, or the more conservative figure available.

4. Are PITIA assumptions realistic?

A property can look strong until the full monthly cost is added.

Taxes, insurance, and association dues can move the DSCR quickly, especially in markets where insurance premiums are high or HOA dues are common. A lender that reviews PITIA carefully before application can catch problems earlier, including reserve pressure after closing. Reviewing cash reserves after closing before underwriting helps investors understand how much liquidity they may need after the down payment and closing costs are paid.

5. Can the lender support LLC ownership and portfolio growth?

Many rental investors prefer to buy through an LLC or another eligible entity structure. The lender should understand entity documents, signer authority, vesting, and how ownership is reviewed.

A lender that can only support single-purchase borrowers creates friction the moment you start building a portfolio.

6. Does the lender offer more than one investor loan product?

A stabilized rental may fit a DSCR loan. A property that needs repairs before it can rent may need bridge or fix-and-flip financing first. A borrower with stronger documentation may compare DSCR against a full-documentation investor loan.

Ziffy’s loan products include DSCR, no-ratio DSCR, bridge, fix-and-flip, and full-documentation investment property loan options. Investors with different deal types on the same calendar should not have to choose a different lender for each one.

Ziffy Property Analysis Snapshot

Early DSCR review becomes more useful when you compare property-level numbers. A lender should help you see whether a property is likely to start as a standard DSCR file, a no-ratio DSCR discussion, or a deal where the income simply does not support the price.

The Grovetown example has healthier rent coverage. The Atlanta example is below 1.00, but close enough that leverage, reserves, and pricing deserve a closer look. The Palm Harbor example has a larger gap, so the investor needs a stronger reason to use more equity or accept a different return profile.

Disclaimer: Property figures are estimate-based as of June 2026 and subject to change. Rates, terms, and eligibility depend on borrower qualifications, property eligibility, documentation, and underwriting review. For informational purposes only.

How Ziffy Approaches DSCR Lending

At Ziffy, the loan conversation starts with the property because the property determines whether a DSCR file makes sense.

Investors can find cash-flowing rentals, review rent and cash flow assumptions, analyze ROI metrics, and finance rentals using the property’s income in one place. As of March 2026, Ziffy tracked over 964,000 active US listings, up 23.5% year over year. For investors comparing deals across markets, that inventory depth helps them decide before they commit to a loan path.

For a deeper look at how Ziffy structures this loan type, read our DSCR loan guide and DSCR loan requirements guide.

Dorian Adams-Walker

Mortgage Loan Originator · Ziffy Mortgage

The cleanest DSCR files usually come from investors who understand the numbers before they apply,” says Dorian Adams-Walker, Mortgage Loan Originator at Ziffy (NMLS #2442830). “If the rent is short, we look at leverage, reserves, liquidity after closing, and whether the investor has a realistic plan for the property.

Questions to Ask Before Choosing a DSCR Lender

Rate matters less than how the lender handles the file when the numbers are tight. These questions help separate a lender that only quotes DSCR loans from one that understands how rental property files actually move.

Start with the property analysis:

- What DSCR do you prefer for standard pricing?

- Do you use lease income, market rent, or the more conservative figure?

- Can you help me review the property before I pay for the appraisal?

Loan structure and execution:

- How much should I expect in reserves after closing?

- Can I buy through an LLC or entity structure?

A lender that fumbles those questions in a pre-application conversation will create bigger problems once the file reaches underwriting. The strongest conversations happen before underwriting, not after a conservative rent schedule or higher insurance quote has already changed the deal.

Start With the Property, Then Choose the Loan

The right DSCR lender helps you avoid preventable problems before they become expensive.

The rent schedule may come back conservative and the final insurance quote may push PITIA above the original estimate. A lender with no no-ratio path may decline a file that another investor-focused lender could have reviewed differently. All three are predictable problems that belong in the lender conversation before the file opens, not discoveries at underwriting.

Ziffy starts with property-level analysis because the loan conversation should not begin in the dark. Early review can move a clean file forward, surface the leverage and reserve adjustments a borderline property needs, or save the investor from forcing a deal the income cannot support.

The investors who avoid expensive surprises are usually the ones who checked the rent, reviewed the full PITIA, and tested the DSCR before they committed to the deal, not after the appraisal.

Ready to review your numbers? Use Ziffy’s DSCR loan calculator to test the property, then get pre-qualified with Ziffy when the deal is ready.

FAQs

Can I get a DSCR loan if the property is below 1.00 DSCR?

Yes, eligible properties below 1.00 DSCR may still be reviewed through no-ratio DSCR. The file usually needs strength elsewhere, such as a larger down payment, lower leverage, stronger reserves, or a clear investment reason.

What does a DSCR between 0 and 1 mean?

A DSCR between 0 and 1 means the property’s rent does not fully cover PITIA. A 0.85 DSCR means the property generates 85 cents in rent for every $1 of monthly housing expense.

Can I use a DSCR loan through an LLC?

Yes, DSCR loans can often support eligible LLC or entity ownership, subject to lender guidelines and documentation review. Investors should confirm entity requirements early so the file does not slow down close to closing.