Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Qualifying for a DSCR loan is less about proving personal income and more about showing that the investment property can carry its own payment. That is what makes the process different from a conventional investment property loan. The lender is still reviewing credit, reserves, documentation, title, and property details, but the central question is simpler: does the rent support the debt?

For investors, a DSCR file usually moves more smoothly when the loan structure is confirmed before the property search gets serious, the DSCR is tested before the offer is submitted, and the documentation is ready before underwriting starts. This walkthrough shows how that process works at Ziffy, from pre-qualification to funding.

Table of Contents

How to Qualify for a DSCR Loan

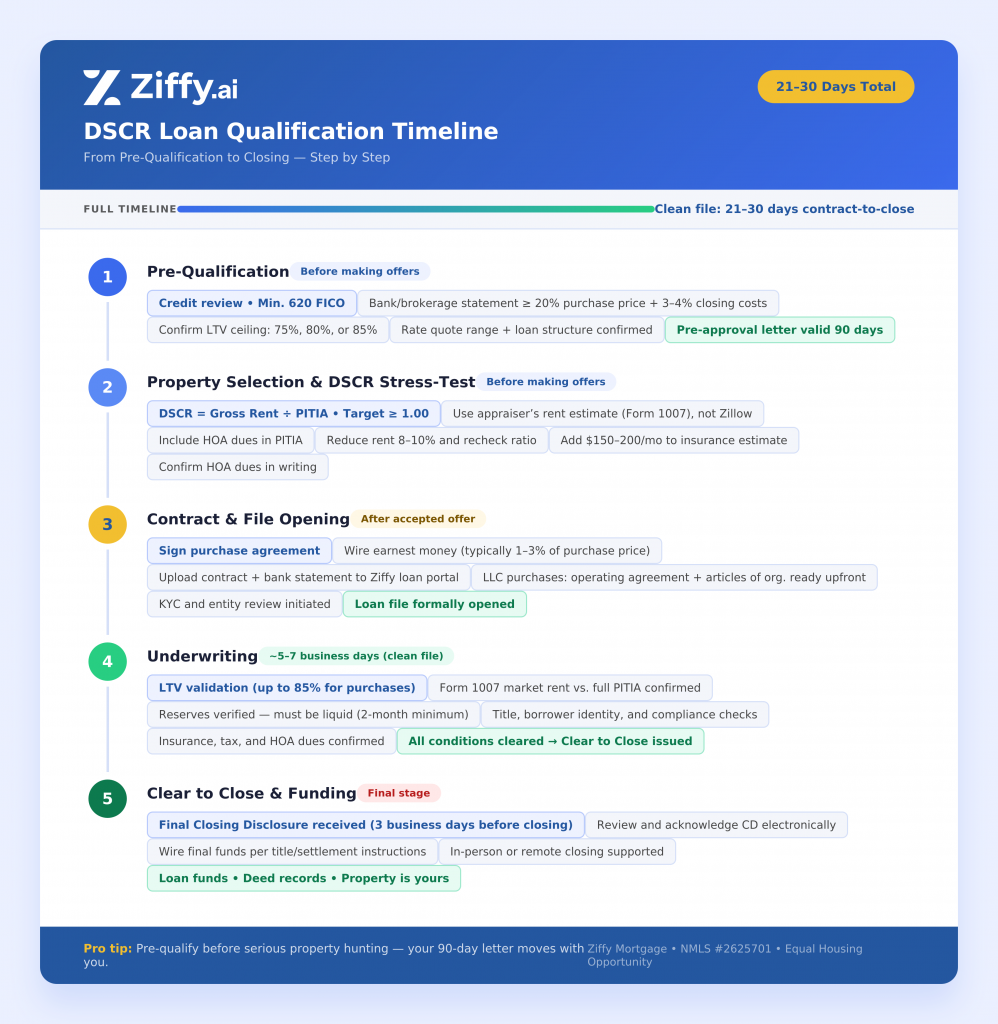

To qualify for a DSCR loan, you move through five main steps: pre-qualification, property selection, contract and file opening, underwriting, and closing. The process is built around the investment property’s rental income, not your W-2 income, and a clean file can often move from contract to close in 21 to 30 days.

Here is the basic order:

- Get pre-qualified before you make serious offers.

- Select a property and stress-test the DSCR.

- Sign the purchase contract and open the loan file.

- Complete underwriting and clear loan conditions.

- Review the final Closing Disclosure, sign closing documents, and fund the loan.

Ziffy pre-approval letters are valid for 90 days, which makes pre-qualification the right first step before serious property hunting begins. This article walks through what happens at each stage. For the eligibility table itself, review our guide to DSCR loan requirements in 2026.

Ziffy is licensed in 48 states and finances DSCR investment properties across a wide range of US markets, so the process below reflects what happens in active investor files, not a hypothetical loan sequence.

Step 1: Get Pre-Qualified Before You Find the Property

Many investors start by looking at listings, estimating rent, and trying to back into the loan after they already like a property. That order creates avoidable problems. Pre-qualifying first, then using the confirmed loan structure to screen deals, avoids the most common timing problem in DSCR purchases.

At Ziffy, DSCR pre-qualification starts with the basics. We review credit, confirm the minimum FICO requirement, and look at whether the borrower has enough liquid funds for the expected down payment, closing costs, and reserves. As a general starting point, investors should be ready to show bank or brokerage statements that cover at least 20% of the estimated purchase price plus roughly 3% to 4% for closing costs.

Ziffy underwrites DSCR files without W-2s, pay stubs, tax returns, or a personal DTI calculation. The approval is driven by whether the property’s rental income covers the payment.

One tradeoff to factor in: DSCR loans usually carry higher rates than conventional loans investment property – typically 0.5% to 1% higher depending on leverage, credit, and DSCR ratio. For investors who want to scale without DTI limits or who cannot document income through W-2s, that tradeoff can still make sense, but it should be built into the return analysis before applying.

Pre-qualification produces a rate quote range and a confirmed LTV lane before the property search gets serious. If the file is likely to work at 75%, 80%, or 85% LTV, that number should guide the first round of deal screening.

Sellers and agents also tend to take a pre-qualified buyer more seriously, especially in competitive markets where financing certainty matters.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

Step 2: Select the Property and Stress-Test the DSCR

Property selection is where the math either works or it does not. The DSCR tells you before you make the offer.

The basic formula is:

DSCR = Gross Monthly Rent ÷ PITIA

PITIA means principal, interest, taxes, insurance, and association dues. The last part is where many investors make mistakes. HOA dues are part of the payment calculation, so they can lower the DSCR on condos, townhouses, and properties in planned communities.

The rent input also needs to be handled carefully. The number that matters in underwriting is not the rent estimate pulled from a rental website. For purchase files, underwriters use the appraiser’s market rent estimate, typically supported by the Single-Family Comparable Rent Schedule, also known as Form 1007.

A 1.00 DSCR means the property’s gross rent matches the PITIA payment. A 1.25 DSCR gives the file more cushion. A DSCR below 1.00 can still be possible through Ziffy’s No-Ratio DSCR option, but it is not priced or structured the same way as a stronger DSCR file.

With the No-Ratio DSCR option, the file may require a higher down payment, more liquid reserves, or a different rate structure than a standard DSCR loan. If your target property shows a DSCR below 1.00, discuss the deal with a loan officer before submitting an offer because the structure may still work, but the economics will look different from a standard DSCR file.

Here is what a stronger file can look like. A Ziffy listing for 100 Hemingway Ct, Georgetown, KY 40324 shows $2,356 in estimated monthly rent and a DSCR profile that clears the breakeven threshold. That cushion gives the file more room to absorb small changes in insurance, taxes, or final rent support.

Now compare that with a property showing $2,050 in rent against $1,980 in PITIA. That works out to a 1.04 DSCR. A 1.04 DSCR clears the threshold, but the cushion is thin. A small insurance increase, higher tax estimate, or lower appraiser-supported rent number could shift the structure.

In our experience reviewing DSCR files, reducing the rent by 8% to 10% before submitting an offer is one of the simplest ways to filter out deals that only work at the most optimistic number. A pattern we’ve noticed is that early insurance estimates can come in $150 to $200 per month lower than the actual policy quote, especially in markets where premiums have moved over the last 12 months. Running both adjustments before the file opens usually leads to fewer surprises in underwriting.

HOA dues should be confirmed before the file moves forward. On a condo or townhouse deal, the official HOA amount can move the DSCR more than investors expect. It is much better to catch that change during deal analysis than after underwriting has already recalculated the payment.

You can run these scenarios through the DSCR loan calculator before the paperwork starts moving. For the property review itself, use our investment property due diligence checklist to make sure the financing math is being checked alongside taxes, insurance, rent, HOA, condition, and local market risk.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

Steps 3 and 4: Contract, File Opening, and Underwriting

A signed purchase agreement opens the loan file. You will also wire earnest money, which is often 1% to 3% of the purchase price, depending on the market and contract terms. Once the contract is signed, you upload the purchase agreement and updated bank statement to Ziffy’s loan portal.

If you are buying through an LLC, do not wait until underwriting asks for entity documents. Have the operating agreement, articles of organization, and related entity paperwork ready when the file opens. Entity purchases require additional review, including ownership, authorization, and standard KYC checks. FinCEN’s Customer Due Diligence Rule is one reason lenders review beneficial ownership and entity structure in legal entity transactions.

The loan file is formally opened once the contract and required intake documents are in. If you found the property through Ziffy’s AI-native real estate investing platform, the investment metrics can help organize the financing conversation early because rent, yield, DSCR, and estimated payment figures have already been reviewed as part of the deal screen.

Underwriting reviews LTV, rent support, reserves, identity, compliance, and title. Ziffy DSCR purchases can go up to 85% LTV, but files structured at 75% usually have more room when rent support, insurance, taxes, or HOA dues shift during review.

The appraiser’s Form 1007 rent is compared against the full PITIA, including confirmed HOA dues. Reserves are reviewed as part of the same file check. Ziffy’s baseline starts at two months, but those funds have to be liquid and verifiable, so retirement accounts and restricted accounts should be confirmed before being counted toward the requirement. For a deeper breakdown, read our guide to cash reserves for an investment property loan.

Borrower identity, title, and compliance checks run in parallel with the rest. LLC purchases add entity ownership review at this stage.

What we see often is that underwriting delays come from simple items, not major deal problems. A bank statement may be stale. The LLC documents may be incomplete. The insurance quote may not match the payment used in the first DSCR screen. None of those issues automatically break the deal, but each one can add another round of review.

Underwriting turnaround runs 5 to 7 business days on a complete file. A clean DSCR purchase can move from contract to closing in about 21 to 30 days. If the bank statement is more than 30 days old, if LLC documents are missing, or if title issues remain unresolved, the timeline can stretch.

A recent Ziffy borrower purchased a single-family rental in Princeton, TX for $240,000 with 25% down, a $180,000 loan amount, and a 30-year fixed DSCR structure at 7.25%. The file opened on January 15, 2026, received final approval, and closed on February 12, 2026, which put the full timeline at 28 days.

The file moved cleanly because the leverage was structured at 75% LTV instead of the maximum, the rent story was clear from the beginning, and the borrower submitted documentation without gaps in the first round.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Investor warning: HOA dues must be confirmed in writing before the final PITIA is built. A verbal estimate from the seller or listing agent is not enough. Underwriting uses the official amount, and a meaningful difference can change the DSCR, the required down payment, or both.

Step 5: Closing and Funding

When underwriting clears all conditions, the file moves to Clear to Close and the Closing Disclosure is issued. The final Closing Disclosure shows the exact funds needed to close, final loan terms, prepaid items, and closing costs.

You review and acknowledge the Closing Disclosure electronically, then prepare the final funds to wire according to title or settlement instructions. Depending on the transaction, closing can happen in person or through a remote closing process supported by Ziffy.

After the final documents are signed and the required funds are received, the lender funds the loan and the deed records. At that point, the investment property is yours.

The 21 to 30 day timeline assumes clean documentation from the first round. Files that need repeated document corrections, updated statements, revised insurance figures, HOA clarification, or title work can take longer.

Get DSCR Pre-Qualified

Qualifying for a DSCR loan follows a clear sequence: confirm the loan structure, test the property’s DSCR, open the file with complete documentation, clear underwriting, and close.

Start with pre-qualification before you make serious offers. You can get DSCR pre-qualified, then use the DSCR loan calculator to test properties before you apply. For a broader explanation of how the product works, read the complete DSCR loan guide.

FAQs

How long does DSCR underwriting take?

DSCR underwriting runs 5 to 7 business days on a complete file. The full contract-to-close timeline can be about 21 to 30 days when the borrower submits clean documentation, the appraisal supports the rent, title is clear, and conditions are resolved quickly.

What documents do I need for a DSCR loan?

For a DSCR purchase, you typically need a signed purchase contract, recent bank or brokerage statements, entity documents if buying through an LLC, identification documents, insurance information, and any additional items requested during underwriting. The appraisal and rent schedule are ordered as part of the loan process.

Can I use an LLC for a DSCR loan?

Yes, Ziffy supports DSCR loans for eligible LLC purchases. If you are buying through an LLC, have your operating agreement, articles of organization, and ownership documents ready before the file opens. Entity files require additional review, so waiting to gather those documents can slow the timeline.

What happens if my DSCR comes in below 1.0?

A DSCR below 1.0 means the property’s gross rent does not fully cover PITIA. Ziffy’s No-Ratio DSCR option may still create a path, but the file will likely require a larger down payment, more reserves, or a different rate structure. Investors should review that scenario with a Ziffy loan officer before making an offer because the deal economics can look different from a standard DSCR file.

Should I get pre-qualified before I find a property?

Yes. Pre-qualification gives you a clearer view of your likely LTV, rate range, reserve needs, and loan structure before you start making offers. That is the information you need to screen properties with real numbers.