Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Florida investment property insurance looks more workable in 2026 than it did during the worst stretch of the state’s insurance crisis, but investors still need to underwrite it property by property.

Citizens Property Insurance Corporation announced that its approved 2026 homeowners multiperil rates will drop by an average of 8.8%, with the new rates taking effect July 1 for new policies and at renewal for existing policyholders. Wind-only policyholders are expected to see an average 5.5% reduction. Citizens also reported that its policy count stood at 336,000 policies in March 2026, down 76% from a peak of 1.41 million policies in October 2023.

Insurance goes directly into PITIA, which includes principal, interest, taxes, insurance, and association dues. PITIA is the expense side of the debt-service coverage ratio, or DSCR. Whether a Florida rental qualifies often comes down to a single number: the actual insurance quote.

In the Florida DSCR files we review, insurance is often the variable that forces a fresh look at the deal. A listing can look strong on price and rent, then weaken once the real insurance quote, flood requirement, named-storm deductible, and association dues are added to the monthly cost. Florida insurance should be reviewed before the offer, not during the final week of underwriting.

Table of Contents

What Changed in Florida’s Insurance Market in 2026?

Florida’s insurance market did not improve because storm risk disappeared. The shift came from legislative reform, litigation changes, Citizens depopulation, and renewed private carrier activity.

Before the reforms, assignment of benefits allowed contractors and other third parties to take over certain insurance claim rights from policyholders. One-way attorney fee provisions also made property insurance litigation more expensive for carriers. Florida’s 2022 special session reforms prohibited the assignment of post-loss insurance benefits under residential and commercial property insurance policies issued on or after January 1, 2023, and removed one-way attorney fee provisions for suits arising under residential or commercial property insurance policies.

Milliman reported that since 2021, nine Florida insurers had gone insolvent, including three of the 10 largest property insurers in the state at the time: FedNat, United Property and Casualty, and St. Johns Insurance Company.

By 2026, the direction had changed. Citizens’ approved 8.8% multiperil rate reduction is one of the clearest signs that the market is not in the same position it was in 2022 or 2023.

That improvement helps investors, especially in newer construction, and properties with stronger wind-mitigation features. The cost gap between an inland rental and a coastal rental is still wide enough to affect financing.

Citizens’ 2026 Rate Reduction: What It Means for Investors

Many Florida owners moved to Citizens when private carriers pulled back, so the approved rate reduction reaches a large policyholder base. The approved statewide average decrease for homeowners multiperil policies is 8.8%, with rates effective July 1, 2026 for new business and at renewal for existing policyholders.

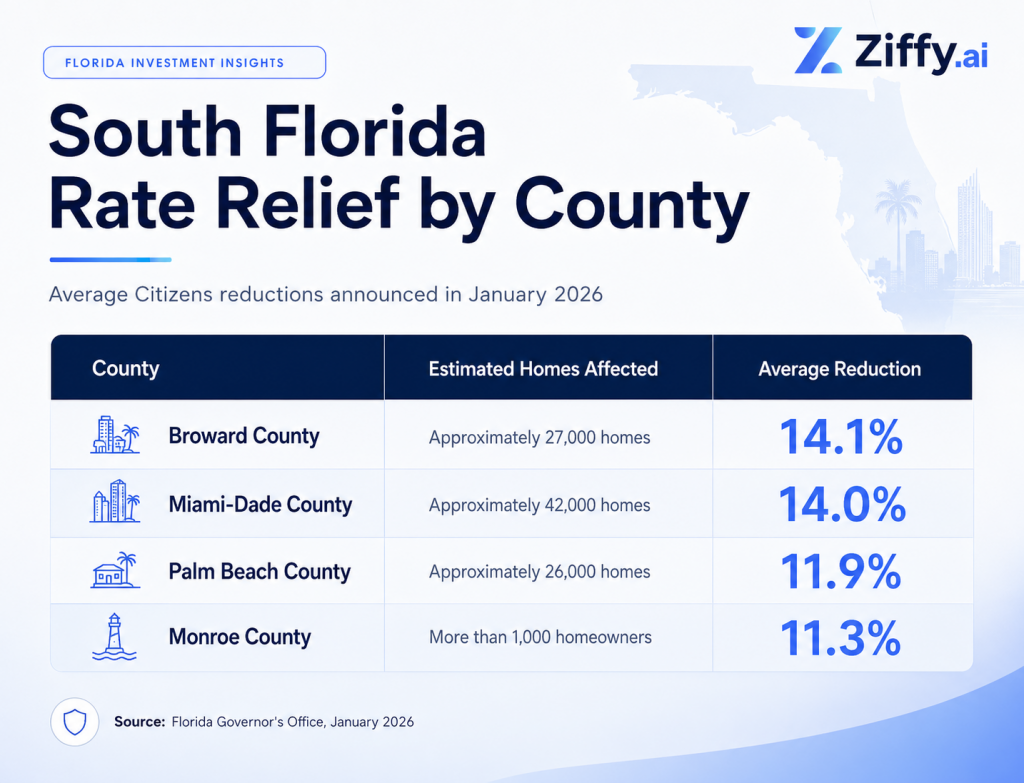

South Florida saw some of the largest reductions in the January 2026 state announcement, including:

The January state release identified the county-level reductions above. Citizens’ March 2026 announcement later confirmed the final regulator-approved statewide average reduction of 8.8% for homeowners multiperil policyholders.

- A $6,000 annual premium reduced by 8.8% saves about $528 per year, or $44 per month. That will not rescue every borderline deal, but it can matter when the DSCR is close and the rest of the file is strong.

- A $44 monthly reduction can move a property from 0.98 DSCR to roughly 1.00 DSCR, depending on rent and total PITIA.

Note: The $6,000 premium and monthly savings example are illustrative. Actual savings depend on the property, carrier, county, roof age, construction type, flood zone, and coverage structure.

The savings are meaningful, but they are not evenly distributed across property types or locations. The investor buying a newer inland rental and the investor buying an older coastal rental are still underwriting two very different insurance profiles.

What Has Not Changed for Florida Investors

Coastal investors should not expect 2017-style premiums to return. The insurance market is improving, but waterfront exposure, older construction, flood risk, roof age, and named-storm deductibles still matter.

Waterfront properties in Miami Beach, Fort Lauderdale, Naples, the Florida Keys, and parts of the Gulf Coast can still carry high annual premiums. Older homes with aging roofs, outdated electrical systems, or limited wind protection can also be difficult to insure through standard carriers.

Named-storm deductibles remain a major cost consideration. In Florida, these deductibles are commonly structured as a percentage of the insured dwelling value. On a $500,000 insured dwelling, a 3% named-storm deductible means the owner may be responsible for the first $15,000 of covered storm damage before the policy responds.

Flood insurance is separate from standard homeowners or landlord coverage. The Federal Emergency Management Agency (FEMA) states that homes and businesses in FEMA-designated Special Flood Hazard Areas with government-backed mortgages are required to carry flood insurance. FloodSmart guidance also notes that some lenders may require flood coverage outside a Special Flood Hazard Area.

Coastal Florida often needs more careful structuring for DSCR borrowers. A higher down payment can reduce monthly debt service and help the property clear DSCR, but it only works if the rent, insurance, taxes, and association dues still leave enough room in the ratio.

When a coastal Florida file comes in close on DSCR, the first thing I want to review is how the insurance was estimated. A generic quote can make the deal look stronger than it really is. Once the actual premium, flood requirement, and named-storm deductible are reviewed, the borrower may need a different down payment, a different property, or a no-ratio path if the file supports it.

How Florida Insurance Directly Affects DSCR Qualification

DSCR is the ratio us lenders use to determine whether a rental property qualifies for financing without making the borrower’s personal income the main approval path. The calculation is:

Gross monthly rent ÷ monthly PITIA = DSCR

At Ziffy, a 1.0 DSCR is generally the preferred minimum for standard DSCR financing. That means the property’s rent should at least cover its monthly housing expense. Ziffy also offers a no-ratio DSCR option (where DSCR is between 0 -1) for eligible files where the property, borrower profile, and overall structure support that path.

Insurance is one of the most variable components in PITIA, and Florida makes that difference easy to see.

Dorian Adams-Walker

Mortgage Loan Originator

Ziffy Mortgage

NMLS #2442830Right now in Florida, we’re seeing better conditions for investor purchases than we saw during the worst of the insurance cycle. The premium decreases are real, and wind mitigation credits can help. But I still would not let a borrower rely on a rough estimate for Florida insurance. In markets like Jacksonville and inland Tampa, the numbers can work cleanly. South Florida waterfront is still a different underwriting conversation.

Investors comparing Florida properties should review Ziffy’s DSCR loan requirements and DSCR loan guide before moving forward with a purchase.

Five Ways Florida Investors Can Reduce Insurance Costs in 2026

1. Order a Wind Mitigation Inspection Before Closing

A wind mitigation inspection can be one of the most useful insurance tools for Florida investors. The Uniform Mitigation Verification Inspection Form, also known as OIR-B1-1802, reviews features such as roof shape, roof deck attachment, roof-to-wall connections, secondary water resistance, and opening protection.

Wind is a major part of the Florida premium, and roof and opening features are among the main variables carriers use to price it. A property with better roof attachments, a hip roof, impact windows, shutters, or other qualifying features may receive a lower wind premium.

Investors often wait until after closing to order this inspection. That shifts the quote at the worst possible moment, after the offer is already in. If the inspection changes the quote, it is better to know that during due diligence while the offer terms or reserve plan can still be adjusted.

Dorian Adams-Walker

Mortgage Loan Originator

Ziffy Mortgage

NMLS #2442830For Florida investors, I usually want the wind mitigation conversation to happen before the appraisal stage. If the inspection shows credits, great. If it shows the roof or openings are weaker than expected, the borrower still has time to adjust the offer, down payment, or reserve plan instead of discovering the issue at the end of the file.

2. Request the Citizens Renewal Effective Date Before Making an Offer

If the property is insured through Citizens, ask the insurance agent when the 2026 approved rate change applies. Citizens said the 2026 rates take effect July 1 for new policies and at renewal for existing policyholders.

A policy that renewed before the effective date may not reflect the reduction until the next renewal. A new policy written after the effective date may be priced differently from an older quote. For a DSCR borrower, even a small monthly change should be reviewed because insurance moves PITIA directly.

3. Re-Quote the Private Market Before Renewal

Citizens’ policy count has dropped sharply, which suggests private carriers are taking on more Florida business again. Citizens reported a policy count of 336,000 in March 2026, down 76% from its October 2023 peak.

That creates a renewal opportunity. If a Florida rental property is currently on Citizens and is not in the hardest coastal category, it is worth requesting private market quotes before renewal.

Private coverage may also reduce one risk Citizens policyholders carry: assessment exposure. Citizens explains that assessments are charges both Citizens and non-Citizens policyholders may have to pay in addition to regular premiums when additional funds are needed to pay claims after a major storm, a series of storms, or another catastrophic event. Citizens policyholders can also face a policyholder surcharge if funds to pay claims are exhausted.

Citizens can still be the right coverage path for some properties, but investors should understand the true cost before assuming it is the cheapest option.

4. Review Flood, Wind, Liability, and Landlord Coverage Together

Florida investors should not review insurance one policy at a time without looking at the full risk profile.

A rental property may need landlord coverage, wind coverage, flood insurance, liability protection, loss-of-rent coverage, and association-related coverage depending on the property type. Condos and townhomes also require a careful review of the master policy because the investor’s individual policy may need to fill gaps.

Bundling can sometimes reduce the total cost, but the larger benefit is seeing what the property actually carries against what the lender requires.

For a broader investor insurance review, use Ziffy’s investment property insurance guide alongside the cash flow calculator.

5. Get a 4-Point Inspection on Older Florida Properties

Older Florida properties can create insurance problems quickly. A 4-point inspection reviews the roof, plumbing, electrical, and HVAC systems. These are the systems carriers care about most when deciding whether to insure an older home.

A property with an aging roof, aluminum wiring, outdated panels, polybutylene plumbing, or major HVAC issues may receive higher pricing or a decline from standard carriers.

A 4-point inspection should happen before the deal is too far along. A property can look attractive from a rent-to-price standpoint and still become difficult to finance if the insurance file does not clear.

Before making an offer on a Florida rental, model the current insurance quote, a possible post-wind-mitigation premium, and a higher renewal scenario. Ziffy’s property analysis helps investors look at those expense changes against rent, PITIA, DSCR, and cash flow before the purchase decision gets too far along.

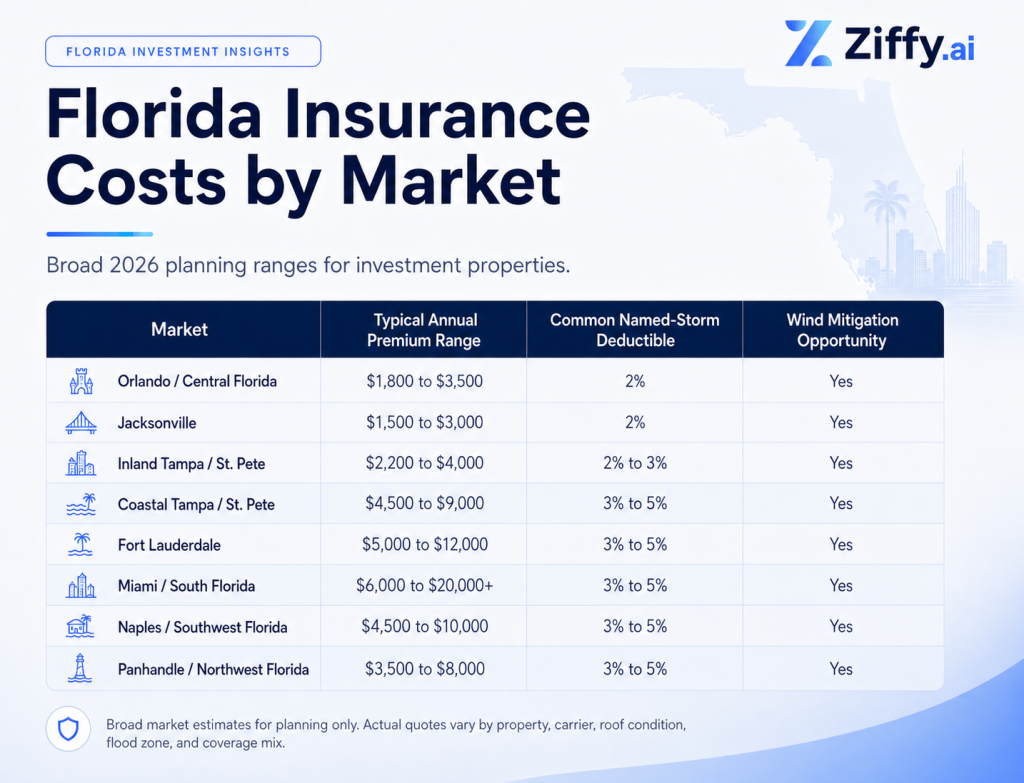

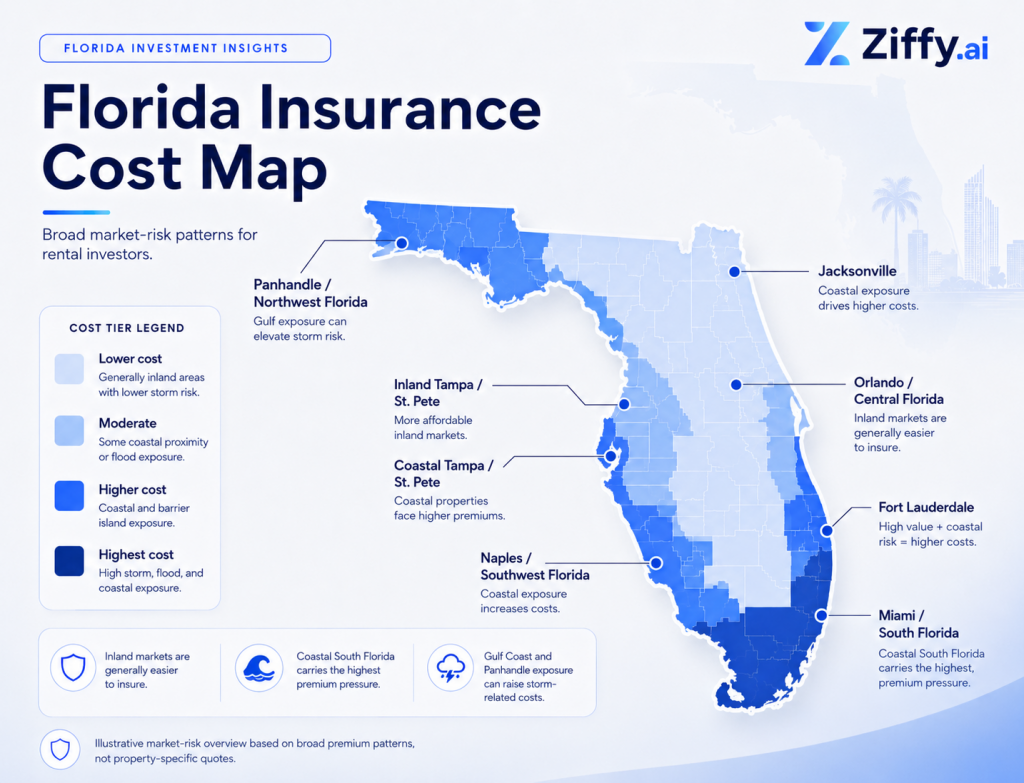

Florida Investment Property Insurance Cost Ranges by Market

Florida insurance pricing is property-specific, but investors still need a starting point when comparing markets. These broad 2026 ranges are for investment-property planning only and should be verified with a Florida-licensed insurance agent before publication use, underwriting use, or borrower-facing quotes.

Insurance note: Premium ranges are market estimates for investment properties and vary by dwelling value, age, construction type, flood zone, carrier, roof condition, coverage selection, and wind mitigation results. Consult a licensed Florida insurance agent for property-specific quotes.

In the ranges above, the difference between lower-cost inland examples and higher-cost coastal examples can exceed $5,000 a year, and that gap moves the DSCR comparison directly.

That difference can decide whether a property qualifies on the first pass or needs more down payment or a different insurance structure.

What to Watch Through the Rest of 2026

Florida’s insurance recovery still needs to hold through hurricane season and reinsurance renewal decisions over multiple cycles.

Reinsurance remains one of the pressure points. Carriers rely on reinsurance to manage catastrophe exposure, and reinsurance pricing affects what insurers charge policyholders. If reinsurance costs rise again after a major storm season, investors could see pressure return in future renewals.

Citizens depopulation is another signal to watch. A lower Citizens policy count generally suggests private carriers are willing to write more Florida business. If that trend reverses, it may point to tighter underwriting or higher renewal pressure.

Anyone actively managing Florida rentals should put annual re-quotes on the calendar. Insurance improvements are not evenly distributed by ZIP code, roof age, property type, or carrier appetite. A rental that was difficult to quote in 2024 may have better options in 2026. The reverse can also happen after a storm, roof issue, or carrier guideline change.

The properties that stall in underwriting are usually the ones where insurance was treated as a last-week item. Florida’s reforms have helped the market, but they do not protect an investor who has not modeled the actual premium yet.

FAQs

Is Florida property insurance getting cheaper in 2026?

For many Citizens policyholders, yes. Citizens announced that approved 2026 homeowners multiperil rates will decrease by an average of 8.8%, with rates effective July 1 for new policies and at renewal for existing policyholders. Wind-only policyholders are expected to see an average 5.5% reduction.

Coastal properties, older homes, flood-zone properties, and buildings with older roofs can still carry high premiums.

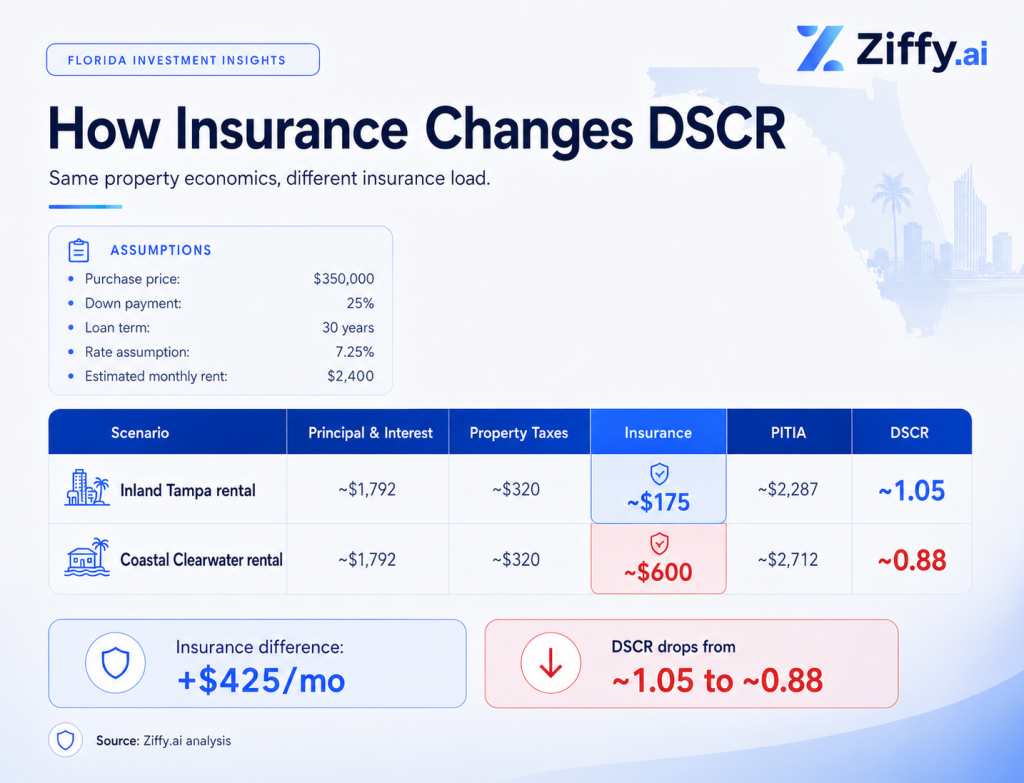

How does insurance affect DSCR on a Florida investment property?

Insurance is included in PITIA, which is the expense side of the DSCR calculation. Higher insurance raises PITIA directly, and PITIA is the denominator in the DSCR formula.

For example, a property with $2,400 in rent and $2,287 in PITIA has about a 1.05 DSCR. If the same property’s PITIA rises to $2,712 because of a higher insurance quote, the DSCR falls to about 0.88.

Can I still get a DSCR loan on a Florida coastal rental?

Yes, but the property has to qualify based on the full payment, including insurance, taxes, and association dues. Coastal properties can still work when the rent is strong enough, the down payment is sized correctly, and the insurance quote is realistic.

If the DSCR falls short, Ziffy’s no-ratio DSCR program may be available for eligible files.

Do Florida rental properties need flood insurance?

If the property is in a FEMA-designated Special Flood Hazard Area and the lender requires flood coverage, the borrower must carry flood insurance. FloodSmart also notes that some lenders may require flood insurance even outside a Special Flood Hazard Area.

Flood insurance is separate from standard homeowners or landlord coverage, so investors should review it early in the transaction.

What is a named-storm deductible?

A named-storm deductible is a separate deductible that applies when damage is caused by a named storm, such as a hurricane or tropical storm. In Florida, it is often calculated as a percentage of the insured dwelling value.

On a $500,000 insured dwelling, a 3% named-storm deductible equals $15,000. That $15,000 belongs in the reserve calculation before closing, not as a surprise after a storm.

What inspections help reduce Florida insurance costs?

The two most useful inspections for Florida investors are a wind mitigation inspection and a 4-point inspection. A wind mitigation inspection can identify features that may qualify for insurance credits. A 4-point inspection helps carriers review the roof, plumbing, electrical, and HVAC systems, especially on older homes.