![Real Estate Investing 101: A Beginner’s Guide [Bonus: Smart Tools From Ziffy.ai]](https://ziffy.ai/learn/wp-content/uploads/2025/10/Ziffy-April-Banners-07-960x659.jpg)

Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Key Takeaways:

1. Real estate is one of the most reliable ways to build long-term wealth. It gives you control over your strategy, helps protect against inflation, and allows you to use financing to grow faster.

2. Ziffy.ai makes real estate investing easier by helping you find, compare, and analyze properties using real data and clear insights so you can invest with confidence.

3. Your strategy should fit your goals and lifestyle. Whether you want steady rental income, quick profits from flips, or to live in one unit and rent the rest, success starts with a clear plan.

4. Smart investing begins with understanding your market and your numbers. Ziffy.ai helps you see how each property performs so you can choose investments that truly build long-term value.

Table of Contents

Real estate investing sounds simple when you say it fast. Buy a property, rent it out, let the rent cover the payment, and build wealth over time. The reality is more technical. Your first deal forces you to understand rent support, debt service, reserves, taxes, insurance, market selection, and loan fit all at once.

That learning curve matters more now because beginners are entering a market where affordability is still uneven. The national rental vacancy rate was 7.2% in the fourth quarter of 2025, which means rental supply exists, but buying conditions are still shaped by price pressure and inventory constraints. In February 2026, the median existing-home sales price was $398,000.

Ziffy’s January 2026 housing research also found that 42 major US markets had zero active house or townhome listings under $300,000, and 55 markets had under-$300K inventory below 1%.

That is why beginners need more than motivation. You need a framework. At Ziffy, the strongest starting point is not “find a house and hope the math works.” It is to move in order: choose the right strategy, shortlist the right markets, analyze the property with conservative assumptions, and then line up the financing that fits the asset. In our experience, first-time investors make better decisions when they treat financing and analysis as part of the search itself, not as something to figure out after making an offer.

This guide walks through that full process. You will see how real estate makes money, which investment types are easiest to start with, how to analyze a rental using Ziffy’s real market data, how DSCR and other investor financing paths fit into the picture, which mistakes waste the most time, and what a beginner-friendly deal can actually look like when you strip away the fantasy math.

What Is Real Estate Investing?

Real estate investing is the process of buying property to generate income, build equity, benefit from appreciation, or improve after-tax returns over time. The distinction here is that investing is driven by repeatable numbers and a clear business plan, while speculating depends too heavily on price growth bailing you out later.

The underlying mechanics are straightforward. A rental property can make money in the following four ways:

- First, it can produce monthly cash flow if income exceeds expenses and debt service.

- Second, the property may appreciate over time.

- Third, your tenants can help pay down principal through the monthly mortgage payment.

- Fourth, rental real estate can create tax advantages through deductible expenses and depreciation. The IRS states that rental income is taxable, that eligible rental expenses can generally be deducted against that income, and that residential rental property is generally depreciated over 27.5 years.

Technically speaking, a few terms matter early:

- NOI is net operating income. That is your gross rental income minus operating expenses before debt service.

- PITIA is principal, interest, taxes, insurance, and association dues where applicable.

- Cap rate measures NOI relative to the property price or current value.

- Cash-on-cash return measures annual pre-tax cash flow relative to the cash you actually invested.

Our dedicated real estate and mortgage glossary explains all these important terms you should know about.

A property can have decent appreciation potential and weak current cash flow. It can also have a reasonable cap rate but still be a poor DSCR fit once taxes, insurance, and HOA dues are factored in. What we see often is that real estate investing is about using these advantages to align property decisions with your financial goals, whether that means stable cash flow, portfolio diversification, or long-term appreciation.

Types of Real Estate Investments

Most first deals do not go wrong because the investor chose a terrible asset class. They go wrong because the investor chose a property type that did not match their budget, time commitment, or financing path.

Investment type | Capital needed | Hands-on level | DSCR fit | Best fit for |

|---|---|---|---|---|

Single-family rental | Moderate | Low to moderate | Strong | Beginners who want a cleaner entry point |

Small multifamily, 2 to 4 units | Moderate to high | Moderate | Strong | Investors who want multiple rent streams |

Short-term rental | Moderate to high | High | Market and property dependent | Investors comfortable with operations |

Commercial real estate | Higher | Moderate to high | Separate loan logic | More experienced investors |

Single-family rentals

Single-family rentals are where many investors start because the financing is usually easier to understand, tenant demand is broad, and the exit options are flexible. You are not limited to selling only to investors later. A future owner-occupant may also be a buyer, which can matter.

Lucas Hernandez,

Loan Officer, Ziffy, NMLS #2171747

A pattern we have noticed is that beginners often undervalue simplicity. The first property is not only about maximizing returns. It is also about learning how repairs, reserves, rent collection, financing, and holding costs actually feel in real life.

Small multifamily

A duplex, triplex, or fourplex can be a strong next step, or even a good first step if the numbers are strong enough. Multiple rent streams can reduce the impact of one vacancy and create better income coverage under the right conditions. At the same time, more units usually mean more management, more turnover risk, and more operational responsibility.

That is why the best multifamily deal is not automatically the one with the most doors. It is the one where the income is strong enough, the expenses are realistic, and the financing still leaves you room to operate.

Short-term rentals

Short-term rentals can outperform long-term rentals on gross income in the right market, but they are not a beginner shortcut. Revenue can swing seasonally, management is heavier, local rules can change, and underwriting standards can be more conservative. A short-term rental is closer to a hospitality business than a plain vanilla rental.

Commercial real estate

Commercial assets can be attractive because they offer scale and different lease structures, but they are usually not the cleanest first deal. The underwriting is more specialized, the financing is different, and mistakes get more expensive faster.

How to Analyze a Rental Property Using Ziffy’s Real Market Data

Analyzing is where beginners either gain clarity or fool themselves. A deal usually does not fail because the spreadsheet was impossible, but because the spreadsheet was too generous.

Start with the five numbers that matter

Before you get excited about a property, identify these five inputs:

- Purchase price: What you are paying for the asset.

- Gross rent: The market rent the property can realistically support.

- Operating expenses: Taxes, insurance, maintenance, vacancy, management, utilities you will cover, and any HOA dues.

- NOI: Income minus operating expenses, before debt service.

- Cash-on-cash return: Annual pre-tax cash flow divided by total cash invested.

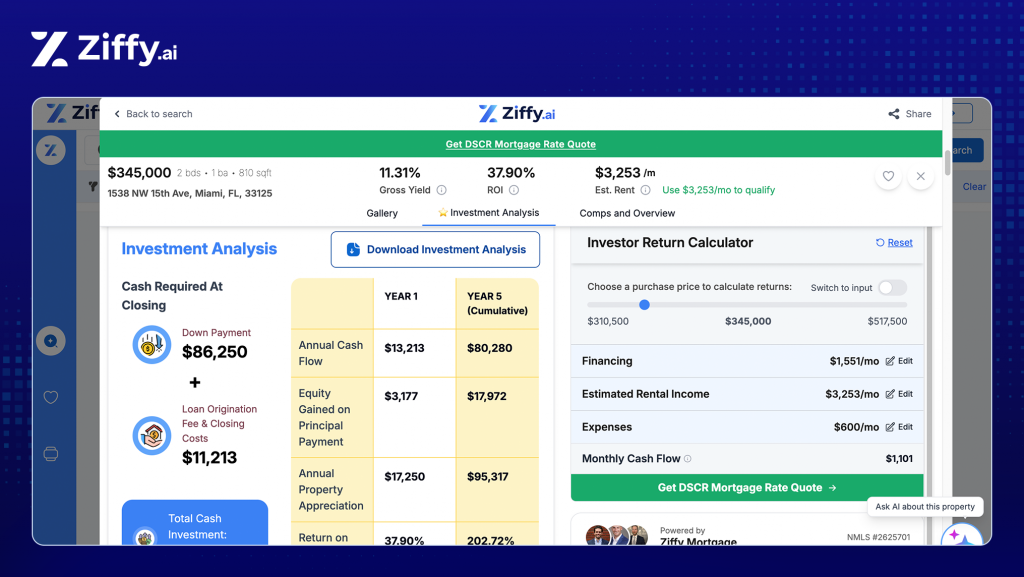

Ziffy’s AI-native real estate investing platform makes that process easier by pulling together the key investment metrics for properties on the platform, so you can screen deals faster without having to build the analysis manually.

Understand how DSCR fits into the math

If you plan to use DSCR financing, you also need to understand how the income side is judged. At a simple level, DSCR compares qualifying rent to PITIA. If the rent comfortably covers the payment, the structure is stronger. If it barely covers the payment, the file is tighter.

At Ziffy Mortgage, our DSCR loan is based on property-based qualification rather than personal-income-heavy underwriting, including the no W-2, no pay stubs, no tax returns, and no DTI-check message investors care about.

Lucas Hernandez,

Loan Officer, Ziffy, NMLS #2171747

In DSCR underwriting, the property’s qualifying rent is often tied to the appraiser’s rent schedule and comparable leases, not the most optimistic listing projection in your worksheet. What most guides don’t mention is that the rent you believe a property can earn is not always the rent your financing will recognize; in DSCR underwriting, the qualifying income is tied to the appraiser’s rent schedule, not your worksheet. HUD’s FY 2026 Fair Market Rent system can be a useful starting reference for local rent conditions, but it is still a reference point, not a substitute for property-level underwriting.

Do not separate cash flow from financing

A property that looks cheap can still be weak if taxes, insurance, or HOA dues are heavy. One thing that surprises investors is how quickly those non-rent-line items can compress a deal that looked healthy at first glance.

To be clear, a good beginner deal does not need to be perfect. It needs to be resilient. It should still make sense if rent comes in a little lighter than expected, if reserves matter more than you hoped, or if the property has one or two normal ownership surprises in year one.

What Ziffy’s own market data shows

In Ziffy’s top multifamily market research, Columbus ranked first overall, Raleigh second, and Nashville third after our company evaluated the 50 largest metros using ten factors including affordability, liquidity, population growth, and market fundamentals.

Within those same market examples, the projected monthly cash flow on featured listings ranged from $16 in Raleigh to $646 in Nashville, with multiple Columbus examples still showing positive monthly cash flow at lower price points. That spread is exactly why beginners should not assume a strong city automatically means every property in it is a good first deal.

The Columbus examples are especially useful to understand how range matters. In our research, one Columbus single-family property was listed at $220,000 with $1,950 per month in rental income and $503 per month in projected cash flow. Another was listed at $135,000 with $1,049 per month in rent and $161 per month in projected cash flow. A third came in at $109,900 with $871 per month in rent and $148 per month in projected cash flow. Those are very different deal profiles, even though they sit in the same metro.

That is the reason analysis comes before emotion. Your first job is not to find the prettiest property. It is to find a property that can still hold together when you run it through a realistic model. You can check all the cash-flowing investment properties listed on Ziffy.ai and see how they fare.

Investment Properties on Sale Today

How to Finance Your First Investment Property

Many beginners think the financing conversation starts after the property search. In practice, it starts before you search seriously, because financing determines what kind of deal will actually work for you.

For some investors, conventional financing can work well. If income is easy to document, debt levels are manageable, and the file is straightforward, it may be a good path. But many investors hit friction early. The paperwork is heavier, DTI can become a constraint, and a property that looks viable on paper may still be harder to place than expected.

That is where DSCR financing becomes relevant. The distinction here is that DSCR is built around the property’s ability to support itself. Ziffy’s mortgage terms are made for investors, without the need for W-2s, pay stubs, tax returns, or DTI checks.

Lucas Hernandez,

Loan Officer, Ziffy, NMLS #2171747

The other thing beginners need to understand is that the down payment is only one part of the capital stack. Closing costs, prepaid items, reserves, and post-closing liquidity all matter. What we see often is that investors ask, “Can I buy this property?” when the better question is, “Can I buy this property and still own it comfortably six months later?”

Lucas Hernandez,

Loan Officer, Ziffy, NMLS #2171747

Bridge loans and fix and flip financing have their place, but they are situational tools. A beginner buying a straightforward rental usually does better by solving for durable acquisition financing first, then learning the faster-moving or more specialized products later. Rates and terms change based on the property, leverage, reserves, borrower profile, and market conditions, so the right structure is always deal-specific.

How to Choose the Right Market

A lot of beginners start by searching where they live, where they grew up, or where they have family. That instinct is understandable. It is also expensive when the market does not support your goals.

As mentioned earlier, Ziffy’s market research gives a better framework. In its multifamily ranking, Ziffy analyzed 50 major metros using factors such as affordability, lending activity, population growth, and broader market fundamentals. Columbus came out first overall because of its balance of affordability, steady growth, and the highest multifamily lending volume per capita among the metros studied. Raleigh and Nashville followed because of their labor-market strength, renter demand, and migration tailwinds.

The affordability section of that same research is useful for beginners because it shows how far apart markets really are. Ziffy listed Cleveland at $54,734 and St. Louis at $55,133 among the most affordable metros by minimum annual income needed, while San Jose came in at $129,433 and New York at $127,726 on the least-affordable side. That is not a small gap. It changes renter demand, acquisition strategy, and the kind of property you can reasonably target as a first deal.

Ziffy’s January 2026 starter-home inventory research tells a similar story from another angle. After analyzing 855 housing markets, we found that 42 markets had zero active house or townhome listings under $300,000 and that 55 markets had under-$300K availability below 1%. That matters to investors because it shows how quickly lower-price inventory can disappear once you move into the wrong metro or the wrong price band.

In practical terms, market selection should come down to four questions:

1. What do prices look like relative to rents?

You want a market where rent is doing enough work to support the purchase.

2. What does renter demand look like?

Population growth, labor-market depth, and affordability all affect this.

3. How liquid is the market?

A market with healthy lending and transaction activity gives you more flexibility later.

4. Can the market support your strategy?

A buy-and-hold investor and a short-term-rental operator are not looking for the same market traits.

The goal is to move from market-level conviction to property-level discipline, which is where Ziffy can help you screen actual listings against the strategy you have in mind.

Investment Strategies That Make Sense for Beginners

The best beginner strategy is not the one that sounds impressive. It is the one that survives normal mistakes.

Buy and hold

Buy and hold is the default for a reason. It gives you time to let financing stabilize, let rents season, let equity build, and learn ownership without relying on a fast exit. For most beginners, this is the cleanest starting strategy.

House hacking

If you are open to living in part of the property while renting another part, house hacking can reduce your housing cost while teaching you how rent, maintenance, and tenant management work in the real world. It is not the same as building an investor-only portfolio, but it is a legitimate entry path.

Fix and flip

This works best when the business plan is clear, the renovation scope is controlled, and the investor is prepared for time pressure and execution risk. A first-time investor can do a flip, but it is usually less forgiving than a stable rental.

Short-term rental

This strategy can work well in the right market, but it brings more operational work and more rule-related uncertainty. It is usually better for investors who already understand how to manage income volatility.

Common Beginner Mistakes That Can Ruin an Otherwise Good First Deal

Based on hundreds of first-time investor files we have worked through at Ziffy, the mistakes below cost more time and money than most beginners expect.

1. Using listing rent instead of supportable rent

Many beginners build their analysis around the rent they hope to achieve, or the number shown on a listing site, instead of the rent the file can actually support. That creates a false sense of safety. A property can look attractive on paper and then weaken quickly once the appraisal or rent schedule comes in lower.

Lucas Hernandez,

Loan Officer, Ziffy, NMLS #2171747

2. Ignoring closing costs and post-closing reserves

A lot of first-time investors focus so hard on the down payment that they forget everything around it. Closing costs, prepaid items, vacancy, insurance adjustments, and early repairs all matter. Bringing enough money to close is not the same thing as being ready to own.

Lucas Hernandez,

Loan Officer, Ziffy, NMLS #2171747

3. Choosing the property before solving the financing

This is one of the most common sequencing mistakes. Investors get attached to a property first and only then find out that the DSCR is weak, the payment is too tight, or the structure needs to change.

Lucas Hernandez,

Loan Officer, Ziffy, NMLS #2171747

4. Underestimating vacancy, maintenance, and frictional costs

A beginner spreadsheet often assumes that nothing goes wrong. Real ownership rarely behaves that way. There is almost always some turnover cost, some maintenance, some delay, or some income softness during the hold.

Lucas Hernandez,

Loan Officer, Ziffy, NMLS #2171747

5. Buying in a market they know instead of a market that performs

Familiarity feels safe, but it does not automatically create a better investment. The better first move is usually to compare markets on price, rent, cash flow, and financing fit, then decide whether the location actually supports your goals.

Lucas Hernandez,

Loan Officer, Ziffy, NMLS #2171747

Case Study: How a Beginner Could Screen a First Rental in Columbus

This case uses a live market snapshot from Ziffy.ai.

In Ziffy’s top multifamily market research, Columbus ranked first overall, and one featured single-family example was listed at $220,000 with $1,950 per month in rental income, $503 per month in projected cash flow, and a DSCR-loan-available flag.

Here is how a beginner could think through that deal:

The first question is not whether the property is exciting. It is whether the spread is wide enough to be useful. A projected $503 per month in cash flow is not huge, but it is materially stronger than the thin $16 per month example Ziffy surfaced in Raleigh. That tells you the Columbus example gives the investor more room for error if rent comes in lighter than expected or expenses run a bit higher.

The second question is whether the market itself supports the strategy. Columbus ranked first in Ziffy’s metro study because of its affordability, steady growth, and high lending activity per capita. That matters because a first property works better when the market gives you some combination of renter demand, financing liquidity, and reasonable entry pricing.

The third question is whether the investor’s financing path matches the property. If the investor is self-employed, has complex personal income, or simply wants a property-income-based loan structure, a DSCR path may make more sense than trying to force a conventional file. Ziffy’s investor-facing mortgage language consistently frames DSCR around that use case.

Lucas Hernandez,

Loan Officer, Ziffy, NMLS #2171747

That is the bigger lesson. A beginner-friendly case study is not about finding a magical deal. It is about finding a deal where the market, the property, and the financing are all pulling in the same direction.

What to Do Next

If you are serious about buying your first investment property, the next step is not to rush into offers. It is to tighten your process. Start with the strategy you can actually execute. Pick markets where price, rent, and demand give you a realistic path. Analyze each deal with conservative assumptions. Then choose financing that matches the property instead of forcing the property into the wrong loan box.

That is where Ziffy fits best. You can move from finding rental opportunities to evaluating rents, returns, and investor financing in one workflow rather than treating each step as a separate project. The most common question we get is whether beginners need to know everything before they start. No, you do not need to. You do need to know enough to avoid the mistakes that make a first deal harder than it needs to be.

Real estate investing gets easier to understand when you stop treating it like a vague wealth-building idea and start treating it like a decision process. The right first deal is not just about finding a property with positive cash flow. It is about choosing the right market, analyzing the numbers honestly, understanding how the financing works, and making sure the property can support the strategy you have in mind. That is what helps beginners avoid expensive mistakes and move into their first investment with more clarity and confidence.

FAQs

How much money do I need to start investing in real estate?

There is no universal number. It depends on the property type, financing structure, down payment, closing costs, and reserves. The reason this matters is that “enough to close” is not the same thing as “enough to own safely for the first year.”

Can I invest in real estate without W-2 income?

Yes, depending on the property and the loan structure. Ziffy Mortgage DSCR is relevant here because it is designed around property’s rental performance rather than a traditional personal-income-heavy file, meaning no W-2, no pay stubs, no tax returns, and no DTI-check positioning.

What is a good cap rate for a rental property?

A good cap rate depends on the market, property condition, risk level, and your strategy. A lower cap rate in a strong market may still make sense if the property is stable and the financing holds comfortably. The honest answer is that cap rate alone does not tell you whether a deal is good for you.

How do I know if a property will cash flow?

To know if a property will bring you positive cash flow, use realistic rent, realistic expenses, realistic vacancy, and a realistic payment. If the deal only works under best-case assumptions, it is not a dependable cash-flow deal.

What is the difference between cap rate and cash-on-cash return?

Cap rate looks at the property before financing. Cash-on-cash return looks at the return on your actual invested cash after financing. Both matter, but cash-on-cash often tells a beginner more about what ownership will actually feel like.

Do I need an LLC to buy an investment property?

Not always. This depends on your legal, tax, insurance, and portfolio goals. The best structure should support the strategy, not complicate it unnecessarily. This is one of those decisions where a CPA and attorney should be part of the conversation.

What tax benefits come with rental real estate?

The IRS generally allows eligible rental expenses to be deducted against rental income, and residential rental property is generally depreciated over 27.5 years. Your specific tax outcome depends on the ownership structure, your income, and how the property is used.

How long does it take to close on an investment property?

That depends on the loan type, appraisal timing, title work, entity setup where relevant, and how quickly the file moves. What we see often is that beginners assume the loan is the whole timeline, when in reality the transaction only moves as fast as the slowest major step.