Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

A subject-to real estate deal lets an investor take title to a property while the seller’s existing mortgage stays in the seller’s name.

The investor owns the property and agrees to make the mortgage payments, which includes collecting rent, handling repairs, and managing the asset as they would any rental. The lender did not originate a new loan to the investor. The seller remains legally responsible for the mortgage until that loan is paid off, refinanced, formally assumed with lender approval, or the property is sold.

Subject-to, often shortened to sub-2, sits in the creative financing category. It is not a formal loan assumption, a lease option, or a DSCR loan; in each of those structures, either the lender is involved or the financing belongs to the investor.

That split is exactly where the risk lives; the investor controls the asset, but the liability stays with someone whose life keeps moving after closing.

Table of Contents

What Transfers in a Subject-to Deal?

What transfers to the buyer | What stays with the seller |

|---|---|

Deed ownership | Existing mortgage liability |

Title interest | Credit exposure tied to the loan |

Possession and control | Original lender relationship |

Rental income rights | Payment history reporting |

Property management responsibility | Due-on-sale clause exposure |

Tax and insurance coordination | Risk if the buyer misses payments |

The seller transfers ownership, but the mortgage note does not automatically move with the property. In a standard sale, the seller’s mortgage is usually paid off at closing. In a subject-to structure, the buyer takes title subject to the existing debt.

The key legal issue is the due-on-sale clause. 12 CFR Part 191 defines a due-on-sale clause as a contract provision that lets the lender, at its option, declare the secured debt immediately due and payable when the property, or an interest in the property, is transferred without the lender’s prior written consent.

For investors comparing creative structures with more conventional financing, Ziffy’s investment property loans guide gives the broader view of how investor financing is normally structured.

Why Investors Use Subject-to Deals

Sub-2 deals usually begin with a seller who needs a faster exit than a traditional listing provides, while the investor is trying to control the property with the existing debt still in place.

Most sub-2 sellers are solving one of three problems: a foreclosure they cannot outrun, a life event that needs a fast exit, or a payment they can no longer afford. The investor is trying to control the property through the seller’s existing debt rather than originating new financing at current rates.

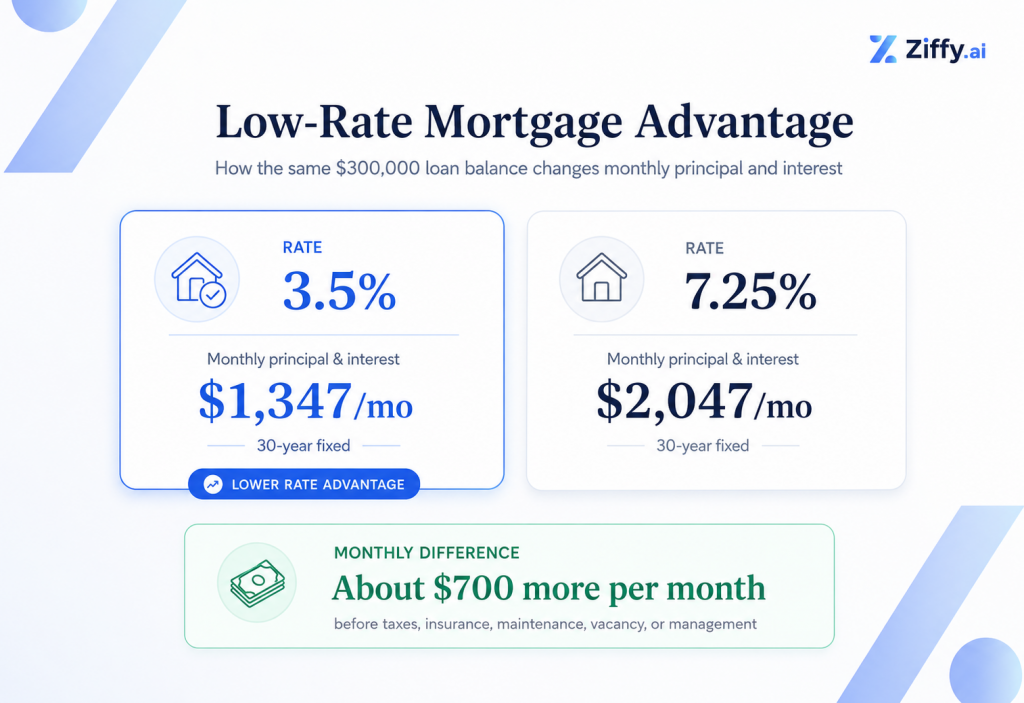

Take a $300,000 loan balance on a 30-year fixed mortgage. At 3.5%, principal and interest is about $1,347 per month. At 7.25%, principal and interest is about $2,047 per month. That is roughly $700 per month before taxes, insurance, maintenance, vacancy, or management.

Many sellers still hold mortgages originated during lower-rate years, which is what creates the payment gap; Freddie Mac reported the average 30-year fixed rate at 6.51% as of May 21, 2026.

The capital demand is also lower than a traditional purchase. The buyer may cover closing costs, arrears, repairs, seller relocation money, or a negotiated equity gap, but no new purchase mortgage closes at the table. That removes the underwriting delay: no lender income review, no new appraisal dependency, no debt-to-income calculation. In a pre-foreclosure or time-sensitive seller situation, that speed can be the difference between closing the deal and losing it.

The deal sidesteps institutional financing, which means it also sidesteps the protections, disclosures, underwriting discipline, and clean liability transfer that come with it.

Rates shown are for illustrative purposes. Actual rates depend on borrower profile, property type, loan-to-value ratio, and market conditions.

How a Subject-to Deal Actually Works

The defining mechanical step is the title transfer. The deed is recorded in the buyer’s name, but the loan remains with the seller. The lender’s contract is still with the original borrower.

Payment handling is where disciplined operators separate themselves from reckless ones. In our experience reviewing investor financing files, the best sub-2 operators use a documented third-party payment or servicing setup so the seller can see that the mortgage is being paid. Without that visibility, the seller is trusting the buyer with their credit every month.

Insurance is where the deal gets quietly complicated. The buyer needs proper hazard insurance because they now own the property, but insurance changes can create lender visibility. A change in policy, mailing address, insured party, or servicer notice can raise questions about ownership. That does not mean the loan will automatically be called, but it does mean the insurance plan should be reviewed before closing.

The buyer manages the property as they would any rental. The operational side can feel entirely normal – rent comes in, expenses go out – but the financing side remains fragile as long as the debt belongs to someone else.

Lucas Hernandez,

Mortgage Loan Originator, Ziffy, NMLS #2171747

Subject-to Deal Lifecycle

For BRRRR investors, the subject-to structure can overlap with acquisition strategy. The difference is that a BRRRR method deal relies on a refinance plan, while a sub-2 deal depends on one because the seller remains exposed until the old loan is replaced or paid off.

The Due-on-Sale Clause is the Central Legal Risk

The due-on-sale clause is the legal pressure point in every subject-to deal, not a buried footnote, but an active contract right the lender can enforce.

A due-on-sale clause gives the lender the option to declare the secured debt immediately due and payable after an unauthorized sale or transfer, as defined by the federal regulations under 12 CFR Part 191.

Most performing loans don’t draw attention for years. A lender collecting payments on time has no immediate reason to investigate the file.

If the lender calls the loan due, the investor does not get to keep the low-rate mortgage because the file has been performing. Fannie Mae’s Servicing Guide says that unless the transfer is exempt or falls into a limited exception, the servicer must accelerate the debt when enforcing the due-on-sale provision.

Steven Glick,

Director of Mortgage Sales, Ziffy, NMLS #1231769

Events That Can Trigger Due-on-Sale Risk

Trigger | Why it creates risk |

|---|---|

Missed payment | The lender reviews the file because the loan is no longer performing |

Seller bankruptcy | The bankruptcy process can expose the property transfer and mortgage liability |

Insurance change | Policy updates may alert the lender that ownership or occupancy changed |

Seller death | Estate, probate, or heirs may reopen questions around ownership and liability |

Lender audit | Servicing or portfolio review may surface an unapproved transfer |

A subject-to deal should be priced around the possibility that the payoff timeline changes. If the lender demands repayment earlier than expected, the investor needs cash, a sale strategy, a private capital source, a bridge loan, or a refinance option that can move quickly.

When Subject-to Goes Wrong

Seller bankruptcy is the scenario that creates the most legal exposure in a sub-2 deal and the one most investors underweight. If the seller files bankruptcy after transferring title, the mortgage is still in their name. The bankruptcy process can expose the transfer, bring the lender into the conversation, and put pressure on the property even if the buyer has made every payment.

Seller death introduces title and probate complications that a performing deal cannot prevent. Heirs may not understand the subject-to agreement. Probate may raise title questions. A properly documented file can still become slow and expensive if the seller’s family disputes the transaction or refuses to cooperate with future paperwork.

A seller who decides they want their name off the loan is harder to manage than a cooperative one. The investor may own the property, but the seller still sees the mortgage on their credit profile. If the seller wants to buy another home, refinance other debt, or clean up their borrowing capacity, they may contact the servicer, pressure the investor to refinance, or refuse to cooperate with future title and payoff paperwork unless the agreement clearly covers those obligations.

Insurance and title gaps can unravel the deal at the worst possible moment. A claim event exposes whether the policy, insured parties, deed, title work, and lender interest were handled correctly. Cheap paperwork becomes expensive when a claim, refinance, or dispute forces every document into review.

Before closing a sub-2 deal, the legal documents, title structure, insurance setup, and seller disclosure language should be reviewed by a licensed real estate attorney familiar with creative financing in that state.

Dorian Adams-Walker,

Mortgage Loan Originator, Ziffy, NMLS #2442830

Subject-to Red Flags to Review Before Closing

What we see often is investors who model the sub-2 acquisition carefully but do not price the seller’s post-closing life into the deal. The property can be performing fine, and the investor may still want the seller’s name off the liability before the next acquisition.

Sub-2 vs Loan Assumption vs DSCR Financing

A loan assumption is the cleaner legal version because it involves the lender directly. The buyer formally assumes the seller’s loan with lender approval instead of taking title while leaving the loan in the seller’s name.

What most guides on subject-to skip: formal loan assumption is only available on Federal Housing Administration (FHA) and Veterans Affairs (VA) loans in any straightforward way. HUD states that FHA-insured Single Family Forward Mortgages are assumable, and VA borrower-rights guidance says VA loans committed on or after March 1, 1988 may be assumed if the loan holder or VA approves the purchaser’s creditworthiness. Conventional Fannie Mae and Freddie Mac loans are typically not assumable in the same direct way, which limits formal assumption to a narrower set of transactions than many investors expect.

A lease option gives the investor control without immediate ownership. The investor leases the property and holds an option to buy later. That can reduce due-on-sale exposure because title does not transfer immediately, but the investor also does not own the asset yet.

A DSCR loan creates new financing in the investor’s name, qualified through rental income and property cash flow rather than W-2 income or personal tax returns. The rate is current market, not the seller’s legacy rate; but the debt belongs to the investor, not the seller. It creates a new investor loan based primarily on rental income and property cash flow, not W-2 income, pay stubs, or personal tax returns. For a sub-2 investor who wants to remove the seller from the debt, DSCR is the institutional exit path.

Strategy | Title transfer | Lender approval | Qualification basis | Due-on-sale risk | Scalability |

|---|---|---|---|---|---|

Subject-to | Yes | Usually no upfront approval | Seller’s existing loan stays in place | High if transfer is discovered or loan is reviewed | Limited without a refinance plan |

Loan assumption | Yes | Yes | Lender-approved assumption process | Low when approved properly | Moderate, depends on loan type and approval |

Lease option | Not at first | Usually not tied to loan assumption |

| Lower because title does not transfer immediately | Limited because buyer does not own the asset yet |

DSCR loan | Yes | Yes, through new loan origination | Rental income and property cash flow | No due-on-sale issue from the seller’s old loan after payoff | Stronger for repeat acquisitions |

Steven Glick,

Director of Mortgage Sales, Ziffy, NMLS #1231769

How DSCR Works as the Institutional Exit

The strongest sub-2 plans treat the seller’s mortgage as a short-term acquisition tool with a defined institutional exit.

The investor needs to know whether rent can support the projected refinance payment after the seller’s old loan is replaced. The new rate may be higher, but the financing is no longer tied to the seller’s credit profile, cooperation, bankruptcy risk, estate issues, or future borrowing needs.

Model the refinance before closing. The key items are projected rent, debt service, loan-to-value ratio, reserves, title seasoning, insurance, and whether the property can qualify after the existing seller loan is paid off. For example, a property with $1,800 in projected monthly rent and a projected $1,450 monthly DSCR payment gives the investor a clearer margin before they close the sub-2 deal, not after. If the refinance payment rises above the rent support, the investor needs to know that before taking title.

The DSCR refinance conversation is built around rental income and property cash flow.

Before counting on that exit, review DSCR loan requirements and run the numbers through Ziffy’s DSCR calculator.

When Subject-to Makes Sense

Subject-to makes the most sense when the rate spread is large, the seller is cooperative, and the investor has a defined exit before closing.

A seller with a 3.25% mortgage in a 6.5% market creates real monthly payment value. The rate spread has to be large enough to justify the legal, title, insurance, and refinance complexity.

Seller motivation and seller instability are different things. Speed and desperation often look the same in the first conversation. A seller who needs speed, understands the structure, and cooperates on documentation creates a very different file from a seller facing bankruptcy risk, judgments, liens, or family conflict.

The exit should be specific: sell within a defined window, refinance once rent and equity are documented, or use the property as part of a broader rental acquisition strategy. A vague plan to ‘keep making payments’ leaves the seller attached to the debt indefinitely and the investor with no clear path when the seller’s life changes.

Lucas Hernandez,

Mortgage Loan Originator, Ziffy, NMLS #2171747

For investors planning to hold and scale, the DSCR exit should be part of the acquisition math from day one. Ziffy’s cash flow calculator can help stress-test rent, expenses, and debt service before the investor negotiates final terms.

When Subject-to Does Not Hold Up

Sub-2 breaks down under three conditions. A thin rate spread is the first: if the investor is accepting due-on-sale exposure, title complexity, and refinance uncertainty for a small payment difference, the deal is probably being forced.

Seller instability is harder to diagnose than a thin rate spread. A seller trying to avoid foreclosure can still be part of a legitimate transaction, but bankruptcy risk, lawsuits, tax liens, estate conflict, or unclear ownership history require deeper legal review. They are stepping into the consequences of the seller’s existing debt relationship.

Scale is the pressure point sub-2 investors often underestimate. Sub-2 can work as a one-off acquisition tool but becomes harder to manage as a portfolio strategy: every deal carries a separate seller liability, servicer relationship, insurance setup, and due-on-sale exposure.

A DSCR cash-out refinance solves the scale problem more directly. The investor may lose the below-market rate, but the new loan is in the investor’s name, qualified through property income, and structured for repeat acquisitions. For investors who want to keep buying, that clarity usually matters more than squeezing every month out of the seller’s old rate.

Investors who need a different short-term capital path before a refinance may also compare bridge loans or fix-and-flip loans, depending on the property plan.

Next Steps

Before closing, three things should be locked before the purchase agreement is signed: the legal structure, the insurance setup, and the refinance timeline.

The structure can protect cash flow when the seller’s rate is well below current market, but it can also leave the seller exposed, trigger due-on-sale risk, and force a refinance sooner than planned.

If the plan is to hold the property and build a portfolio, map the DSCR exit before closing. Ziffy can help investors review rental income, projected debt service, loan-to-value ratio, reserves, title seasoning, and refinance timing through a DSCR pre-qualification.

Start with the DSCR loan guide or review No-Ratio DSCR loans if the property needs a different documentation path.

FAQs

Is subject-to real estate legal?

Purchasing property subject to an existing mortgage is legal, but it does not erase the lender’s contract rights. If the mortgage includes a due-on-sale clause, the lender may have the right to call the loan due after an unauthorized transfer, subject to federal law, state law, and the loan documents. Every sub-2 deal should be reviewed by a licensed real estate attorney before closing.

Can a lender really call the loan due if I take over a property subject-to?

Yes. A due-on-sale clause can give the lender the right to demand full repayment after an unauthorized ownership transfer. Federal law recognizes the enforceability of due-on-sale clauses, with specific exemptions for certain transfers. The practical risk may be event-driven, but the consequence can be severe if the lender accelerates the debt. See 12 CFR Part 191 for the federal due-on-sale framework.

What happens to the seller’s credit in a subject-to deal?

The mortgage usually remains on the seller’s credit profile because the loan stays in the seller’s name. If the investor makes every payment on time, the seller’s payment history may remain protected. If the investor misses payments, the seller’s credit can be damaged even though the seller no longer owns the property. That is why sellers often want proof of payment handling and a defined refinance or payoff timeline.

Can I refinance a subject-to property into a DSCR loan?

Yes, if the investor owns the property and the file meets DSCR refinance guidelines. Ziffy evaluates DSCR files primarily through rental income and property cash flow, not the investor’s W-2 income, pay stubs, or personal tax returns. The lender will still review credit, reserves, appraisal, title, insurance, entity structure, and loan-to-value ratio. Title seasoning should be confirmed during Ziffy pre-qualification before the investor treats DSCR as the planned sub-2 exit.

Why would I refinance out of a low-rate subject-to loan?

The reason is control. A 3.5% mortgage in the seller’s name may produce stronger monthly cash flow, but it does not give the investor clean liability, lender-recognized debt ownership, or a repeatable financing structure. A DSCR refinance trades the old rate for legal clarity, seller release, institutional underwriting, and the ability to use equity for the next deal.

Do I need a real estate attorney for a subject-to deal?

Yes. Subject-to real estate involves title transfer, lender contract rights, due-on-sale exposure, seller liability, insurance structure, and state-specific legal issues. A general purchase contract is not enough for this kind of transaction. Work with a licensed real estate attorney who understands creative financing before entering a subject-to agreement.