Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Townhouses can be good investment properties, but only when the rent, HOA, and legal structure all work together. At Ziffy, townhouses are an eligible DSCR property type, and DSCR is calculated using gross rental income divided by PITIA, with HOA dues included when they apply. That one detail explains why some townhouse deals underwrite cleanly while others get squeezed even when the rent looks decent at first glance.

The real question is not whether townhouses are “good” in the abstract. It is whether a specific townhouse fits the kind of investing you are trying to do. A low-HOA townhouse in a clean PUD structure can be a practical buy-and-hold rental. A condo-classified townhouse with heavy dues and restrictive HOA rules can become a thin-margin asset fast. This guide walks through both sides so you can screen the deal correctly before you offer.

Table of Contents

What Makes a Townhouse Different as an Investment

A townhouse sits between a detached rental and a condo, and that is exactly why investors misread them. Physically, it may feel closer to a small single-family home. Legally, though, the lender is looking at project structure, not just curb appeal. Fannie Mae’s project standards distinguish between condo projects and PUD projects, and its PUD eligibility rules state that the unit cannot be legally created as part of a condo or co-op project. That distinction changes how the property is reviewed and whether project-level issues become part of the file.

The distinction here is between a PUD-style townhouse and a condo-style townhouse. They can look almost identical from the street, but the legal structure changes the financing path. If the unit is part of a condo project, lenders may need project review, and Fannie Mae’s ineligible-project standards can narrow the clean exit path for both today’s loan and tomorrow’s resale buyer.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

That is why townhouses belong in the broader conversation around types of investment properties, but they should never be screened as a generic attached-housing category. You are not only underwriting the unit. You are also underwriting the obligations that come with the project around it.

Why Investors Buy Townhouses in the First Place

One reason is pricing. As of January 20, 2026, Ziffy’s starter-home inventory research across 855 housing markets found that 63.45% of active house and townhome listings were priced at $300,000 or higher, based on a Dec. 23, 2025 active-listings snapshot. That does not mean every townhouse is cheaper than a detached house in its market, but it does explain why attached housing stays in the investable conversation when entry pricing gets harder.

Another reason is operational simplicity. In our experience, investors often accept less exterior control when the tradeoff is less day-to-day maintenance coordination. A well-run townhouse HOA can take recurring exterior tasks off your plate in a way an older detached rental cannot. Roof coordination, exterior upkeep, and common-area disputes often stop being one-property problems. That does not make the HOA free. It makes the cost more predictable when the project is healthy.

A pattern we have noticed is that townhouse renters often want a layout that feels closer to a home than an apartment. More space, a garage, a small outdoor area, and separation across multiple floors can make the property more durable as a long-term rental. That does not guarantee longer tenancy, but it can support a steadier hold in suburban submarkets where renters want more room without paying full detached-home pricing.

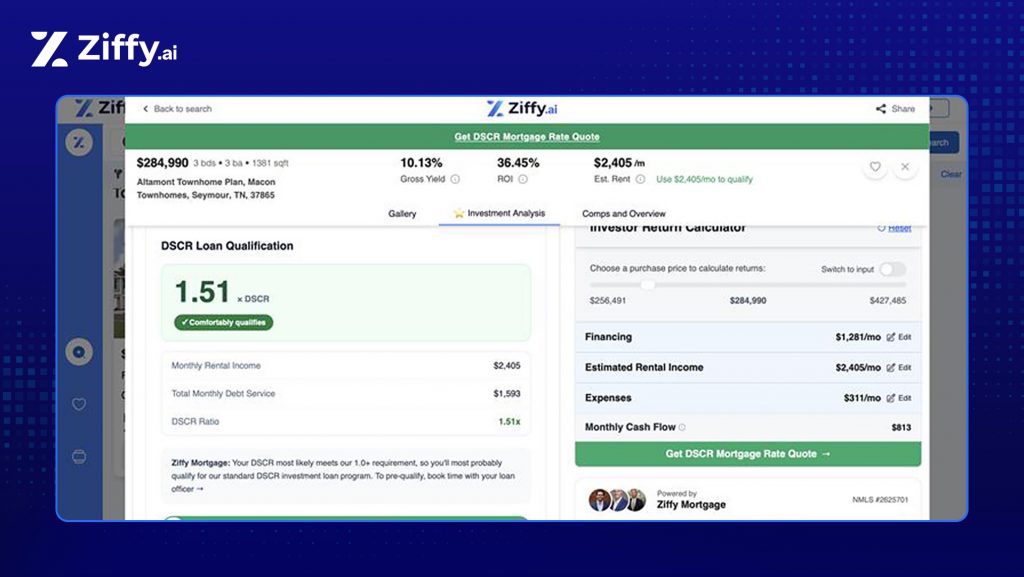

The best reason to like townhouses is still simple math. In Seymour, Tennessee, one townhouse currently listed on Ziffy shows $2,405 in estimated monthly rent, $1,593 in total monthly debt service, and 1.51x DSCR under the current assumptions. That sits comfortably above the standard 1.0+ DSCR benchmark. That is the kind of attached-housing profile investors actually want: reasonable price, clean rent support, and real DSCR margin.

Townhouses can also fit portfolio growth well when they qualify through the DSCR path. At Ziffy, the DSCR loan program can finance single-family homes, townhouses, condominiums, and multifamily properties from 2 to 10 units, with qualification based primarily on rental income rather than personal income or debt-to-income ratio. For investors trying to keep acquisitions moving without leaning on W-2 underwriting every time, that matters.

Where Townhouse Investments Break Down

The biggest risk is usually not the rent. It is the HOA. What most guides do not mention is that HOA dues are not merely an operating expense you can mentally tuck away after the deal penciles. In DSCR underwriting, HOA dues are part of PITIA. Since DSCR equals gross rental income divided by PITIA, the dues directly reduce the ratio the lender sees.

A townhouse that looks fine at first glance can move from comfortably financeable to borderline just because the monthly HOA is higher than expected. Same rent. Same purchase price. Very different underwriting outcome.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

The next problem is rule risk. With a townhouse, you are often buying into leasing rules, occupancy caps, architectural controls, and sometimes short-term rental restrictions. This will not work if the HOA has already hit its rental cap or blocks the exact leasing strategy you plan to use. That is why townhouse due diligence needs the governing documents early, not after you fall in love with the unit.

Project classification is the other major break point. To be clear, townhouses are not disqualified from DSCR financing. At Ziffy, townhouse properties can fit the DSCR path. But condo-classified townhouse projects can introduce review friction that detached homes skip, and Fannie Mae’s ineligible-project standards are another reminder that project structure can narrow the financing pool.

Cash Flow Analysis: How to Run the Numbers Correctly

Start with two separate tests. First, run lender math. Does the rent cover PITIA, including HOA dues when they apply. Second, run investor math. After the payment, management, vacancy, and reserves, is there still enough spread left to justify the hold. Those are connected questions, but they are not the same question.

Technically speaking, the PITIA calculation treats HOA dues as a fixed payment obligation, not a variable ownership cost you can explain away later. That is why townhouse underwriting feels less forgiving than a quick back-of-the-envelope rental estimate. Once the HOA gets large enough, the deal does not need to be terrible to start looking thin.

For a simple benchmark, HUD’s FY 2026 Fair Market Rent schedule lists the Nashville-Davidson, Murfreesboro, Franklin metro at $2,211 for a three-bedroom unit. If you model a townhouse with a $221,250 loan at about $1,585 in monthly principal and interest, then add $350 for taxes and insurance and a $175 HOA, the DSCR comes out to roughly 1.05x using that HUD rent figure. Push the HOA to $425 and the ratio drops to about 0.94x. That is not theoretical hand-waving. It is the same deal changing shape because the fixed obligations got heavier.

If you use a more conservative illustrative rent of $2,100 on the same payment assumptions, the ratio is effectively break-even at just under 1.0. That is the clearer takeaway. A townhouse does not need catastrophic numbers to become a borderline loan. It only needs a thin rent-to-payment spread and an HOA that looked harmless when you first saw the listing.

That is why the clearest example here is still Seymour. It shows what a townhouse looks like when the rent covers clearly and the project does not appear to be dragging the file down.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Pro Tips Before You Make an Offer

Ask for the HOA budget and reserve information early. One downside to consider is that a low monthly fee is not automatically good news. Sometimes it means the project is efficient. Other times it means the HOA is under-reserved and future assessments are being deferred into your ownership period. If the dues are low but the project looks tired, dig harder.

Confirm PUD versus condo classification before you spend money on the full file. Do not rely on the listing description. Ask the title company, review the recorded declaration, or have the loan team confirm the project structure early. Fannie Mae’s PUD rules are explicit that the subject unit cannot be legally part of a condo or co-op project.

Stress test the DSCR before you offer, not after. Run the rent against PITIA first, then run the property again with management and vacancy. If the deal only works in the prettiest version of the math, it does not really work. This is the tip most investors skip because the initial numbers can feel close enough. Close enough is not the same thing as durable.

Ask the HOA whether rentals are capped and how many rental slots are already in use. “Rental cap utilization” sounds like dry admin language, but it can decide the whole strategy. If the cap is full, you may be buying a unit you cannot lease the way you planned.

Based on the townhouse DSCR loans we’ve closed, properties with modest HOA dues tend to qualify at standard thresholds far more consistently than properties where the dues consume too much of the rent before the investor has even budgeted management or vacancy. That is not a surprise. It is just the underwriting reality showing up exactly where it should.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Townhouse vs. Single-Family vs. Condo

Factor | Townhouse | Single-family rental | Condo |

|---|---|---|---|

Entry point | Often mid-range | Often higher in the same submarket | Often lowest |

Maintenance burden | Usually lighter if HOA is healthy | Usually highest | Usually lightest |

HOA drag on DSCR | Moderate to high | Usually low or none | Often highest |

Financing path | Cleanest when structured as PUD | Usually most straightforward | Most project-sensitive |

STR flexibility | Project-dependent | Usually strongest | Often most restricted |

Best fit | Investors balancing maintenance and affordability | Investors prioritizing control and resale flexibility | Investors who can handle tighter project review |

The table is not saying townhouses beat single-family rentals or condos across the board. It is saying the tradeoff is predictable. If you want the easiest underwriting and broadest resale pool, detached single-family usually wins. If you want lighter maintenance and a manageable acquisition price, townhouse can win. If you want the lowest-maintenance ownership box and can live with more project review friction, condo still has a place.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Who Should Buy a Townhouse, and Who Should Not

A townhouse can be a strong fit for a newer investor who wants a long-term rental without taking on every exterior repair issue that can come with a detached home. In that case, a healthy HOA is doing useful work for you, not just collecting a fee.

It can also work well for an investor trying to qualify through the DSCR path, but only when the HOA-adjusted ratio is tested before the offer goes in. If the dues push the file toward the edge, a comparable single-family rental may produce a cleaner result at a similar price.

A townhouse is a weaker fit for an STR investor who needs flexible rules. It is also a weaker fit for someone buying through an LLC without first confirming whether the project documents place any restrictions on ownership or leasing structure. The legal work is not the hard part. The hard part is catching the restrictions before closing.

How to finance a townhouse investment property

At Ziffy, a townhouse investment property usually fits the DSCR path when the rent supports PITIA and the legal structure is acceptable for underwriting. DSCR qualification is based primarily on rental income rather than personal-income qualification, and townhouses are one of the eligible property types. A 1.0+ DSCR is the cleaner standard threshold, though some below-1.0 scenarios may still be explored case by case.

That does not mean every townhouse is financed the same way. PUD-style townhouses are usually simpler. Condo-classified townhouses can trigger project-sensitive review, and Fannie Mae’s project standards are a reminder that not every project is equally easy to deliver. The practical move is to run the rent, taxes, insurance, and HOA through the DSCR math exactly the way underwriting will see it before you treat the property as a real target.

Rates and terms are subject to change based on credit, reserves, property type, project structure, and the full loan scenario. Illustrative examples are for education only, and actual results will vary.

Next Steps

If a townhouse deal is on your shortlist, do three things before you move forward. Confirm whether the project is a PUD or condo, plug the HOA into the DSCR math instead of treating it as a side expense, and stress test the deal with real ownership costs before you offer. That will tell you more than the listing description ever will.

Your next move should be practical, not theoretical. Run the deal through Ziffy’s DSCR loan calculator, compare the real monthly spread with a cash flow calculator, and check the bigger return picture with a rental property ROI calculator. Then get pre-qualified if the property still looks clean after that. If the townhouse only works in the optimistic version of the math, keep looking. If it still works after the stricter test, that is when it becomes a real candidate.

FAQs

Are townhouses harder to finance as investment properties?

Not automatically. The main question is whether the project is legally a PUD or a condo, because that changes the review path and the project standards the lender applies.

Do HOA fees affect DSCR loan approval?

Yes. HOA dues are included inside PITIA when they apply, so higher dues directly lower the coverage ratio.

Can I use a DSCR loan to buy a townhouse?

Yes. Townhouses are one of the property types that can fit the DSCR path.

What is a good DSCR for a townhouse?

A ratio above 1.0 is the cleaner place to be for best terms.

Can I Airbnb a townhouse investment property?

Only if the HOA and project rules allow it. That answer has to come from the governing documents, not the floor plan or listing copy. For that strategy, review the short-term rental guide.

Are townhouses good long-term buy-and-hold rentals?

They can be, especially when the HOA is reasonable, the structure is straightforward, and the rent still leaves enough room after debt service to make the hold worthwhile. For that approach, see the buy-and-hold strategy guide.