Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

House hacking gives first-time investors a way to buy a home, reduce their monthly housing cost, and start building a rental portfolio without immediately buying a separate investment property.

Most beginners assume real estate investing starts with a 20% to 25% down payment, a second property, and enough cash reserves to carry two housing payments at once. House hacking changes that starting point. You buy a residential property, live in one unit or portion of it, and rent out the remaining space. The rental income helps cover your mortgage, taxes, insurance, and other housing costs.

Housing is already the largest monthly expense for most households. The US Bureau of Labor Statistics reported that housing averaged $26,266 per year in 2024, or 33.4% of total household spending. Census Bureau data also showed that over 21 million renter households spent more than 30% of income on housing costs in 2023. That is why house hacking stands out: it turns a cost most people simply pay every month into a starting point for ownership, rental income, and long-term portfolio building.

This guide is for renters tired of paying someone else’s mortgage, first-time buyers who want their home to help carry itself, and early-stage investors who want a lower-capital entry into real estate. If you want the broader foundation first, start with our guide on how to invest in real estate. If you are ready to focus on house hacking, this article walks through the property types, financing options, real math, tenant management, tax treatment, and exit strategy.

Ziffy Mortgage works with real estate investors across 48 states, including borrowers evaluating owner-occupied multi-unit purchases and future investment-property financing paths. For many investors, house hacking is not just a cheaper way to live. It is the first property in a larger buy-and-hold plan.

Table of Contents

What Is House Hacking?

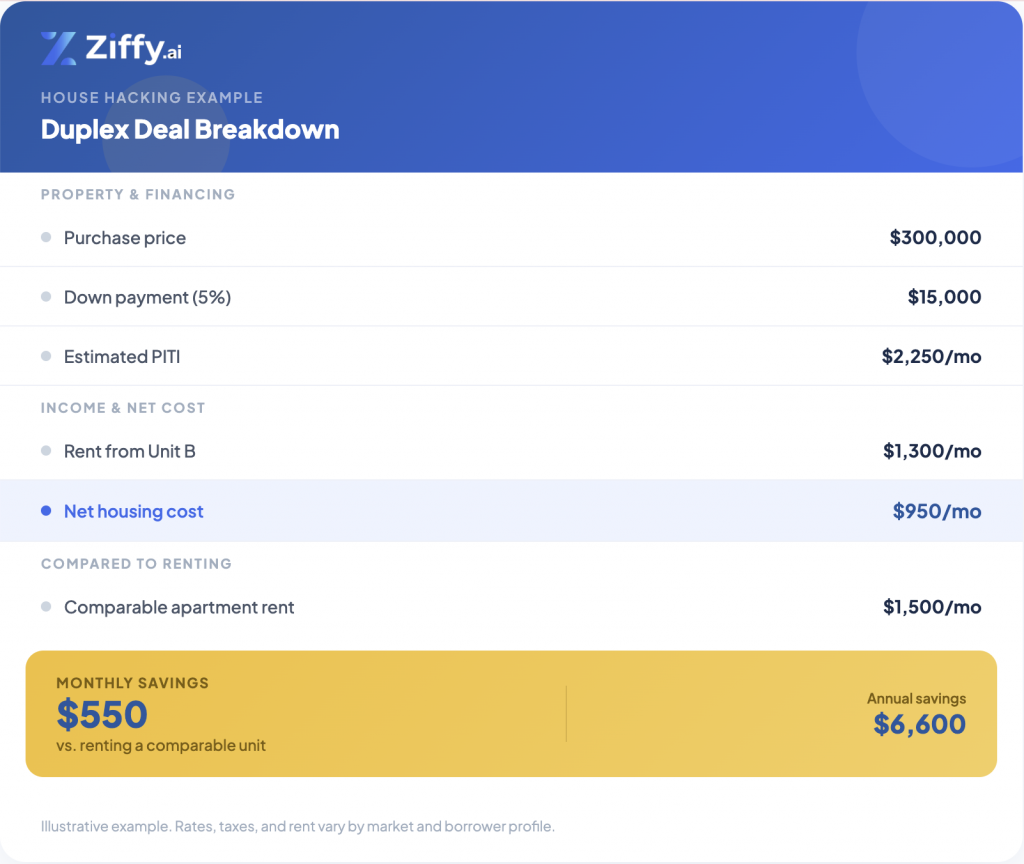

The classic setup is a duplex: you live in Unit A, your tenant lives in Unit B, and their rent covers part of your mortgage. That is house hacking, using your primary residence as an income-producing property from day one.

More broadly, house hacking is the strategy of buying a residential property, occupying one unit or portion of it as your primary residence, and renting out the remaining space to generate income that offsets your housing cost.

You qualify for owner-occupied financing because you will live in the property. You move in and collect rent from the other unit, room, or ADU. That rent reduces your monthly housing cost and, in the strongest deals, brings it close to zero.

Here is a simple example.

That does not mean you are “living for free” in every deal. In many real markets, the cleaner goal is living for far less than local rent while building equity in an asset you own.

House hacking is also not the same as casually renting a spare bedroom to a friend. That can be a version of the strategy, but the defining feature is that rental income meaningfully offsets the total housing payment. The property has to be evaluated as both a home and an income-producing asset.

If this is your first investing concept, read our real estate investing 101 guide after this article. It will help you see how house hacking fits beside buy-and-hold rentals, BRRRR, short-term rentals, and other strategies.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

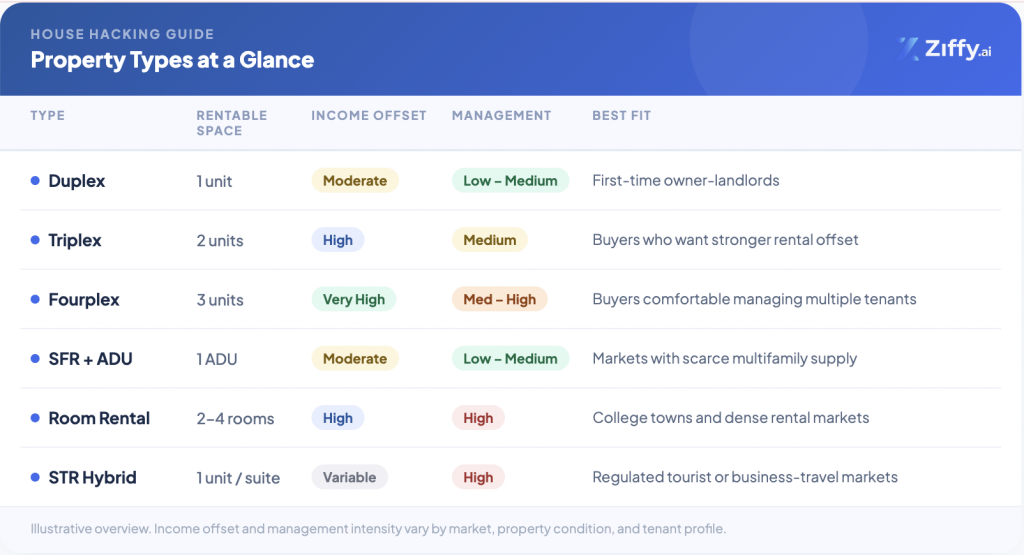

The 4 Main Types of House Hacking

House hacking is not one single property type. The right setup depends on your market, budget, tolerance for tenant interaction, and financing path.

1. Multi-Unit House Hacking: Duplex, Triplex, or Fourplex

This is the classic house hack. You buy a 2-4 unit residential property, live in one unit, and rent the others.

A duplex gives you one tenant household. A triplex gives you two. A fourplex gives you three. The more rentable units you have, the stronger the potential income offset, but the management workload also rises.

The 1-4 unit boundary matters. Properties with up to four residential units can generally fall under residential mortgage underwriting. Once you move to five or more units, the deal shifts into commercial property territory, with different underwriting, different documentation, and often a larger down payment requirement.

This setup is best for investors who want the clearest path from primary residence to rental property. Once you move out, the entire building can operate as a traditional long-term rental. It can also become a clean candidate for a future refinance, including a DSCR loan, if the rental income supports the debt.

The tradeoff is proximity. You are not just buying a rental. You are living next to your tenants. That can work well when leases, boundaries, and maintenance systems are clear. It gets messy when the owner treats the arrangement informally.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

2. Single-Family Home With an ADU

The ADU strategy works best in markets where duplexes are rare or overpriced. In suburban markets where every good multifamily listing gets bid up fast, a garage apartment, basement unit, or backyard cottage on a single-family lot can give you a similar rent offset with more privacy.

An accessory dwelling unit, or ADU, is a separate rentable living space on the same property as a main home. It may be attached or detached, but it needs to be legal, permitted, and usable as a rental under local rules.

Do not assume an ADU is legal just because it exists. You need to verify whether the unit was permitted, whether it can be rented, whether it meets habitability standards, and whether local zoning allows the use you are planning.

A beautiful backyard cottage does not help your loan file or rental strategy if the city does not allow it to operate as a legal rental.

ADU strategies work best in high-demand residential markets where tenants want privacy but cannot afford a full single-family rental.

3. Room-by-Room House Hacking

Room rentals can produce strong income, but they are not a passive version of house hacking. You are not just buying a house with extra bedrooms. You are creating a shared living arrangement with separate tenants, separate schedules, and a higher need for written rules.

In this model, you buy a larger single-family home and rent individual bedrooms. It is common near universities, hospitals, downtown employment centers, and areas with a strong young-professional tenant base.

The upside is income per square foot. A four-bedroom home rented by the room can sometimes produce more gross rent than the same home leased to one household.

The downside is management. Shared kitchens, bathrooms, guests, cleaning standards, parking, noise, and lease enforcement become part of your day-to-day life. This is not the lowest-friction version of house hacking.

Room rentals need precise leases. Each tenant should know what space they control, what space is shared, how utilities work, how guests are handled, and what happens if one tenant leaves before the others.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

4. Short-Term Rental Hybrid

A short-term rental hybrid means you live in one part of the property and rent another part on Airbnb, Vrbo, or a similar platform.

This can work in tourist corridors, downtown areas, beach markets, mountain towns, and event-driven cities. Nightly rates can beat long-term rent, but the income is less predictable and regulations vary sharply by city.

This strategy does not work if your municipality bans short-term rentals, your HOA restricts nightly stays, or your loan and insurance structure do not support the intended use. Verify local law, HOA rules, insurance coverage, and lender guidance before building your numbers around nightly-rate income.

Use our short-term rental guide before committing to this model. The nightly-rate upside is not worth much if the property cannot legally operate the way you planned.

The House Hacking Math: Does It Actually Work?

The core formula is straightforward:

Net Housing Cost = PITI - Rental Income Collected

PITI means principal, interest, taxes, and insurance. In some deals, you also need to include HOA dues, mortgage insurance, utilities paid by the owner, and maintenance reserves.

A house hack works best when your net housing cost is lower than what you would otherwise pay to rent a comparable home in the same market. The strategy works even better when the property also has a clear path to positive cash flow after you move out.

As of May 14, 2026, Freddie Mac’s Primary Mortgage Market Survey showed the average 30-year fixed-rate mortgage at 6.36%, slightly down from 6.37% the previous week. PMMS results are released weekly on Thursdays, so this was the latest available survey figure at the May 17, 2026 article update. Borrower rates vary by credit profile, loan size, property type, occupancy, points, and loan program.

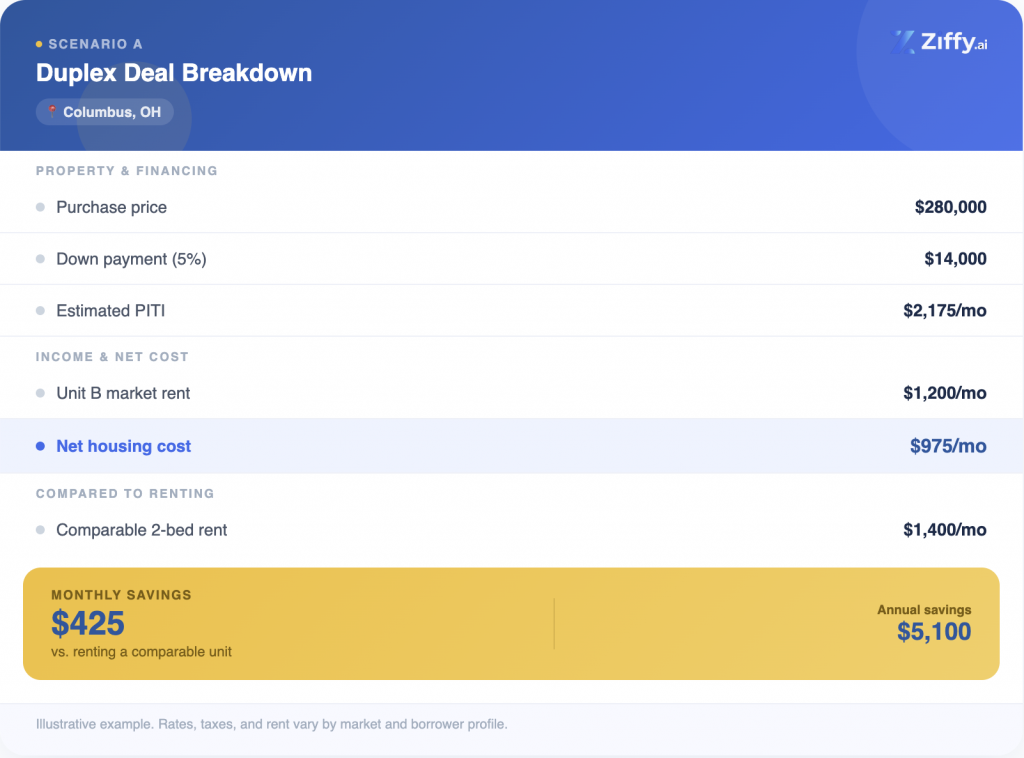

Scenario A: Duplex in Columbus, OH

This is the kind of deal that makes house hacking attractive. The buyer is not living for free, but they are living below comparable rent while owning the building. If they move out later and rent both units, the property has a path to becoming a full rental asset.

Investors looking in central Ohio can start with Columbus OH properties, then use Ziffy’s cash flow calculator to test rent, PITIA, vacancy, and operating expenses.

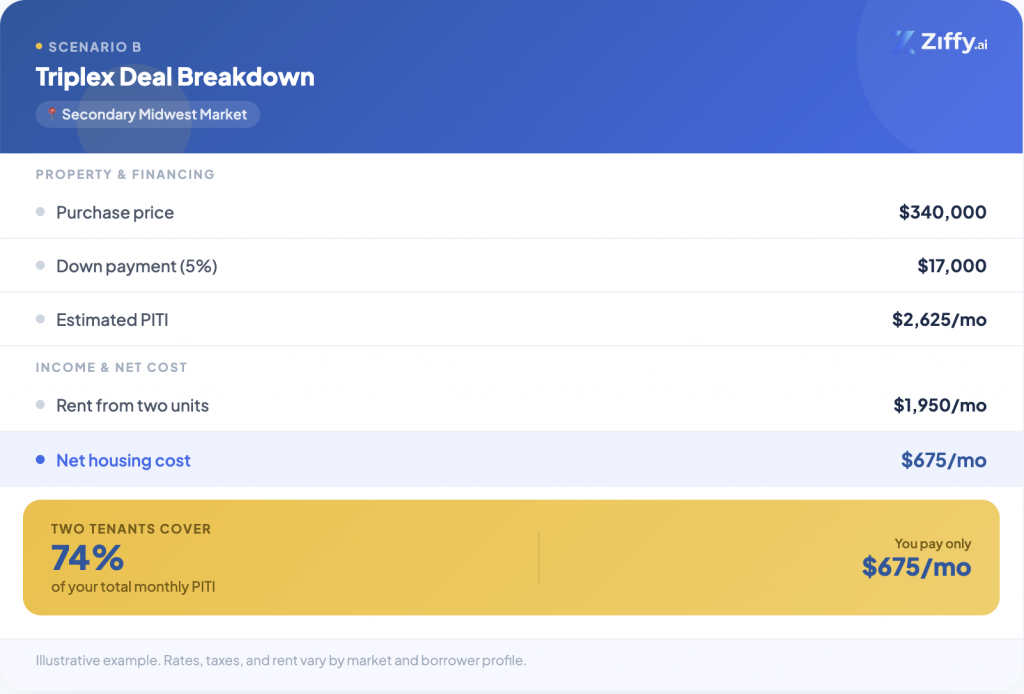

Scenario B: Triplex in a Secondary Midwest Market

This setup gives the buyer a much stronger income offset because two units are producing rent. The risk is that a triplex has more moving parts. You need to evaluate lease quality, tenant payment history, unit condition, deferred maintenance, separate utilities, and whether the rents are already at market.

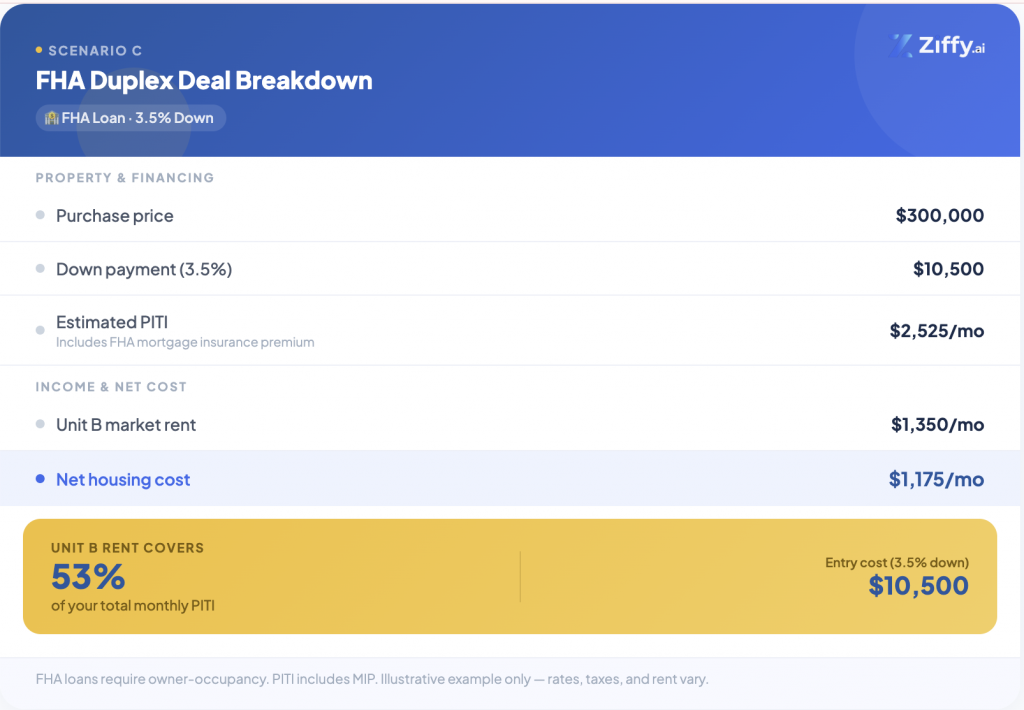

Scenario C: FHA Duplex With 3.5% Down

The FHA version lowers upfront cash, which can help buyers who have solid income but limited savings. The tradeoff is mortgage insurance. FHA loans generally include upfront and annual mortgage insurance premiums, and borrowers should review current HUD rules before choosing FHA over conventional financing. HUD’s Handbook 4000.1 is the central policy source for FHA single-family lending.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

What we see often is investors running the numbers at full estimated rent and full occupancy. The deal looks great until the appraiser’s rent schedule comes in lower or the first vacancy lasts longer than expected. Run the numbers with a cushion before you make the offer, not after the file is already moving.

Lenders do not underwrite your deal based only on a listing description or a rent estimate you found online. For 2-4 unit primary residences, rental income rules depend on loan program, documentation, property management experience, and whether the rent can be used to qualify. Fannie Mae’s rental income worksheet applies a 75% factor to gross monthly rent or market rent, with the remaining 25% accounting for vacancy loss, maintenance, and management expenses.

That is why conservative underwriting matters. Use 85% to 90% of projected market rent in your first pass. If the deal only works at perfect rent and perfect occupancy, it is not a strong deal.

Use our cash-on-cash return guide once you are comparing this property against other investment options. House hacking is partly about reducing your living cost, but the deal still needs to make sense as an asset.

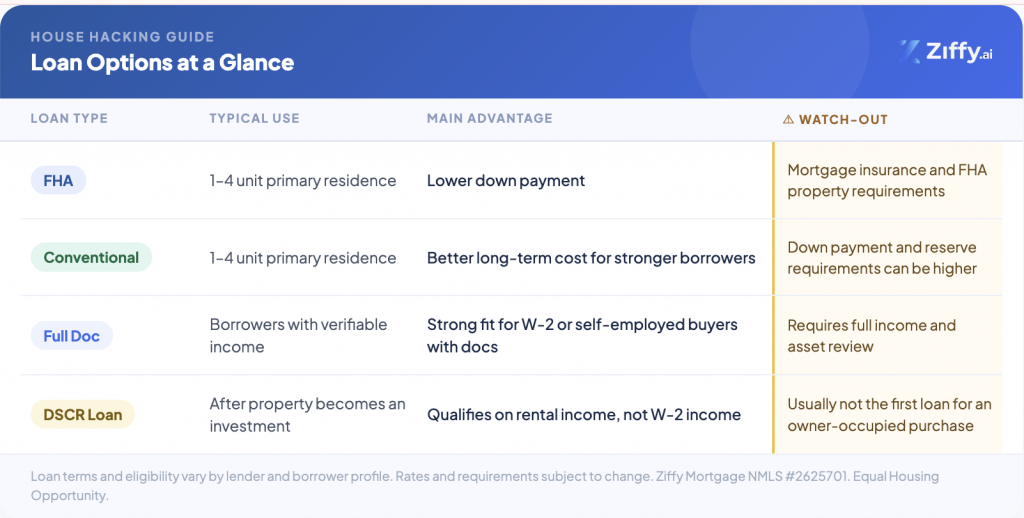

How to Finance a House Hack

Financing is where house hacking gets its biggest advantage. You are buying an income-producing property, but because you will live there, you may qualify under owner-occupied mortgage rules instead of investment property rules.

An investor buying a separate rental property often needs a larger down payment, higher reserves, and stronger investment-property pricing. A house hacker may be able to use FHA, conventional, or a full documentation owner-occupied loan because the property is also their primary residence.

The DSCR Loan Exit Ramp

House hacking becomes more powerful when you treat it as the first step in a portfolio plan.

After you satisfy the owner-occupancy requirement and are ready to move out, the property can become a full investment property. At that point, a DSCR loan may become the stronger financing tool.

A DSCR loan qualifies the property based on rental income relative to PITIA, not your W-2 income or personal debt-to-income ratio. That matters because many investors outgrow traditional DTI-based financing as they add properties.

The sequence looks like this:

- Buy a 2-4 unit property using owner-occupied financing.

- Live in one unit while renting the others.

- Build equity and landlord experience.

- Move out after satisfying occupancy rules.

- Rent your former unit.

- Refinance into a DSCR loan if the property’s rent supports the debt.

- Use the next property to repeat the process.

Read our DSCR loan requirements guide before assuming the refinance will work. DSCR qualification depends on rent, PITIA, credit, reserves, property type, leverage, and loan purpose.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Full Documentation Loan Through Ziffy

A full documentation loan works for borrowers who can verify income through W-2s, tax returns, pay stubs, self-employment documentation, or other accepted income documents.

For house hackers with stable income and a clear owner-occupancy plan, this can be a clean way to finance a 1-4 unit property. Ziffy looks at the borrower’s income, assets, credit, reserves, property details, occupancy plan, and rent support to help determine which loan path fits the file.

Read our full documentation loan guide if your income is documentable and you want to compare it against FHA or other financing paths.

What most house hacking guides do not mention is that rental income can help with qualification on certain 2-4 unit owner-occupied purchases. Under Fannie Mae rental income calculations, 75% of projected rental income may be used in the analysis when the file meets program requirements. For a buyer with tight DTI, that rent support can change the approval path.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

FHA Loan

FHA loans are popular with first-time house hackers because they allow low down payments on eligible 1-4 unit primary residences. FHA can be especially useful for buyers with limited upfront capital or credit profiles that do not receive the strongest conventional pricing.

The tradeoff, however, is mortgage insurance. FHA mortgage insurance can increase the monthly payment and may remain in place for a long period depending on the loan term, down payment, and case details. Borrowers should compare total cost, not just down payment.

Under FHA security instruments, borrowers are required to establish bona fide occupancy as a principal residence within 60 days and continue occupancy for at least one year. Confirm current requirements with your loan officer before relying on FHA for a house hack.

Conventional Loan

Conventional financing can be a better long-term fit for borrowers with stronger credit, income documentation, and reserves. It may require more money down on 2-4 unit properties depending on the program and borrower profile, but the mortgage insurance structure can be more favorable than FHA over time.

A conventional loan can also make sense if your exit plan is to hold the property and refinance later. The lower lifetime mortgage insurance drag can matter once the property becomes a full rental.

Cash Reserves

Cash reserves are separate from your down payment and closing costs. They are liquid funds left over after closing.

For a house hack, reserves matter because one vacancy or repair can change the math quickly. If your PITI is $2,300 per month and a lender requires two to six months of reserves, you may need $4,600 to $13,800 in available assets after closing.

Ziffy’s reserve review depends on the file. Property type, loan program, credit profile, number of units, occupancy, and borrower strength all matter.

A pattern we have noticed: buyers who account for reserves before shopping rarely get surprised at the closing table. Buyers who do not often find themselves scrambling to explain the gap between their savings and what is actually available after the down payment and closing costs.

Use our guide to cash reserves for investment property loans to understand how reserves affect rental financing.

How to Find a House Hack Property

A good house hack starts with the right market. You need a price-to-rent relationship that gives the rental unit enough income to offset your housing payment.

Start with three property searches.

- First, look for 2-4 unit residential properties. On listings, these may appear as multifamily, duplex, triplex, fourplex, or income property.

- Second, look for single-family homes with an existing ADU or a lot that may support one. Do not assume an ADU is legal just because it exists.

- Third, look for large single-family homes in markets where room rentals are common. College towns, hospital corridors, and downtown employment centers tend to perform better for this model than quiet suburban neighborhoods.

The fastest 15-minute screen looks like this:

Screening Question | What You Need |

|---|---|

What is the estimated PITI? | Use current rate, taxes, insurance, and HOA if applicable |

What rent is already being collected? | Ask for leases and rent roll |

What is conservative market rent? | Use lease data, local property managers, and rent comps |

What is your net housing cost? | PITI minus conservative rent |

Is that lower than local rent? | Compare against similar units |

What repairs are obvious? | Roof, HVAC, plumbing, electrical, foundation, unit interiors |

What is the exit? | Hold, DSCR refinance, sell, or move into the next house hack |

Before making an offer, run the property through our investment property due diligence checklist. House hacking gives you a lower-capital entry point, but it does not protect you from buying a property with bad leases, weak rent support, or expensive deferred maintenance.

Markets Where House Hacking Tends to Work Better

House hacking usually works best where purchase prices are still reasonable compared with achievable rent.

Midwest markets such as Columbus OH, Indianapolis, Cleveland, Kansas City, and Toledo often give buyers more realistic duplex and triplex opportunities than high-cost coastal markets. Parts of the Southeast and Texas secondary markets can also work, especially where workforce rental demand is strong and multifamily supply still exists at entry-level prices.

High-cost markets such as Los Angeles, New York City, San Francisco, and Seattle are harder. The purchase price is often too high relative to the rent from the second unit. That does not make house hacking impossible, but it raises the income threshold and lowers the margin for error.

Our guide to the best places to invest in real estate can help you compare market-level fundamentals before narrowing your search.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

For a deeper sourcing framework, read our guide on how to find cash flow properties.

Step-by-Step: How to House Hack From Offer to Move-In

Step 1: Get Pre-Approved Before You Shop

Do not analyze properties without knowing your real budget. Pre-approval tells you your purchase ceiling, expected cash to close, documentation gaps, and likely loan path.

For house hacking, pre-approval is especially important because the property type can change the file. A duplex, triplex, fourplex, ADU, and single-family room rental may not be treated exactly the same way. Ziffy reviews income, assets, credit, intended occupancy, reserves, and property goals before helping you structure the right path.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

Step 2: Define Your Property Criteria

Choose your property type before you shop seriously.

Set your maximum purchase price, target net housing cost, preferred unit count, repair tolerance, reserve comfort level, and target ZIP codes. Also decide which unit you plan to occupy. Lenders need a clear owner-occupancy designation, and your occupancy plan needs to make sense.

Narrowing your search to two or three ZIP codes helps you learn rent comps faster. You will start recognizing which duplexes are overpriced, which neighborhoods rent quickly, and which listings have rent estimates that are too optimistic.

Step 3: Run the 15-Minute Screen

Use this formula:

Estimated PITI - Conservative Rent = Net Housing Cost

Then compare your net housing cost with what you would pay to rent a similar unit.

If the house hack costs $950 per month and a comparable apartment costs $1,450, the strategy is giving you a $500 monthly housing advantage before equity growth. If the house hack costs the same as renting, you need to look more carefully at appreciation potential, principal paydown, tax treatment, and future rental conversion.

Use the rental property ROI calculator once you are past the first screen and want to evaluate the longer-term return.

Step 4: Make an Offer and Request the Rent Roll

For a multi-unit property, always request the rent roll, current leases, security deposit details, lease expiration dates, and known maintenance issues.

You are not only buying walls and a roof. You may be inheriting tenant relationships, under-market rents, late-payment history, old leases, undocumented agreements, or maintenance promises made by the seller.

Include appropriate inspection protections. A house hack can be a strong strategy, but not if your first year is consumed by a roof failure, sewer issue, or unsafe electrical system.

Step 5: Complete Third-Party Reports

The appraisal matters for both value and rent support. On a multi-unit property, the appraiser may provide a rent schedule that helps the lender evaluate projected rental income. That figure can differ from the listing rent estimate or your own projection.

The inspection matters because every extra unit adds extra systems. A duplex may have two kitchens, two water heaters, separate electrical panels, separate HVAC, or shared mechanicals that need closer review.

Title and insurance also need attention. Ziffy’s processing team helps coordinate required loan steps, but the borrower should read documents carefully and ask questions early.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

Step 6: Move Through Underwriting

Underwriting verifies your income, assets, credit, reserves, property eligibility, and occupancy plan. For 2-4 unit properties, the file may also involve rent documentation and additional property-level review.

Respond quickly to documentation requests. A delayed bank statement, unexplained deposit, missing lease, or unclear occupancy plan can slow the file.

Step 7: Move In and Set Up the Rental Side Properly

Closing is not the finish line. It is the day you become both owner and landlord.

Before or immediately after closing, organize leases, rent collection, tenant communication, maintenance requests, emergency procedures, utility tracking, and records. If a unit is vacant, begin tenant screening quickly. Vacancy weakens the house hack math.

The biggest mistake is treating the rental side casually because you live nearby. Proximity is helpful, but it does not replace systems.

Managing Tenants When You Live Next Door

Living near your tenants gives you an advantage. You can catch maintenance issues early, spot exterior problems quickly, and respond to emergencies faster than an absentee landlord.

It also creates a boundary problem. Without clear rules, tenants may knock on your door for minor issues, expect informal rent flexibility, or treat shared spaces casually.

Use five rules from day one.

- First, use a proper lease. A handshake agreement is not enough. Spell out rent, due dates, late fees, maintenance reporting, shared spaces, parking, pets, guests, noise, and access.

- Second, set communication hours. Define what counts as an emergency, such as active water leaks, no heat, no power, or safety concerns. Everything else should go through the agreed maintenance channel.

- Third, screen tenants the same way you would for a property across town. Credit, income, landlord references, and background checks matter more when the tenant lives next door.

- Fourth, charge market rent. Discounting rent because you like the tenant may feel generous at first, but it weakens your numbers and creates problems when renewal time comes.

- Fifth, document everything. If a conversation happens face-to-face, follow up by text or email. Written records protect both sides.

In our experience, house hackers who set up written systems before move-in have fewer tenant friction issues in the first six months. The lease, maintenance channel, communication hours, and rent collection process should be clear before anyone has a reason to test the boundaries.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

House Hacking and Taxes: What You Need to Know

Rental income from a house hack is taxable. In most individual rental scenarios, rental income and expenses are reported on Schedule E. IRS Publication 527 covers residential rental income, expenses, depreciation, and special rental situations, including renting only part of a property.

You may be able to deduct expenses tied to the rental portion of the property, including:

For a duplex where you live in one unit and rent the other, a common approach is to allocate shared expenses by square footage or unit percentage. If each unit is the same size, 50% of certain shared expenses may relate to the rental side. Direct expenses for the rental unit may be fully rental-related.

The primary residence exclusion can still apply to the owner-occupied portion if you qualify. IRS Publication 523 covers the tax rules for selling a home and includes guidance for properties with separate business or rental use. Mixed-use properties need careful handling because the rental portion and depreciation history can affect the tax result.

Depreciation recapture is one of the most overlooked tax issues. If you depreciate the rental portion, the IRS may require recapture when you sell. Speak with a tax professional before filing or selling because house hacking creates both personal-use and rental-use tax questions.

Read our real estate taxes guide for broader coverage.

5 Common House Hacking Mistakes to Avoid

1. Running the Numbers at Full Rent

What we see often: a buyer uses the highest rent estimate they can find, assumes full occupancy, and ignores turnover. Then the appraiser’s rent support comes in lower, the unit sits vacant for three weeks, or taxes reset after closing.

Use conservative rent. Budget at least some vacancy. Add maintenance reserves. If the deal still works, you have a stronger property.

2. Skipping Tenant Screening

A tenant who “seems nice” can still miss rent, damage the unit, ignore lease rules, or create daily stress. Screen every applicant. Verify income. Call landlord references. Use written criteria. Follow fair housing rules. Do not lower your standards because you are living nearby.

3. Choosing the Wrong Strategy for the Market

A room-rental model that works near a university may fail in a quiet suburb. A short-term rental plan may collapse if the city restricts permits. An ADU may be unusable if it was never legally permitted. Match the strategy to documented local demand and local rules.

4. Ignoring the Exit Strategy

House hacking is not just a way to reduce your housing payment. It is often the first move in a larger portfolio plan.

Before you buy, decide what happens when you move out. Will you sell? Keep the property as a long-term rental? Refinance into DSCR? Move into another house hack? Use it as a BRRRR-style stepping stone?

Our guides to the BRRRR method and buy and hold strategy can help you compare the next step.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

5. Underestimating Repairs Across Multiple Units

A duplex has more systems than a single apartment. A triplex has even more. Multiple kitchens, bathrooms, furnaces, water heaters, doors, locks, and appliances create more maintenance exposure.

Budget for repairs even when the inspection looks clean. A practical starting point is setting aside a percentage of rental income for maintenance and capital reserves. The exact number depends on property age, condition, systems, and local labor costs.

Case Study: From House Hack to First Cash-Flowing Rental

Illustrative scenario based on current Columbus, OH market conditions

A buyer in Columbus OH purchases a two-unit duplex for $275,000 using 5% down conventional financing.

- Property type: 2-unit duplex

- Purchase price: $275,000

- Down payment: $13,750

- Estimated 30-year fixed rate: 6.75%

- Estimated PITI: $2,120/month

- Unit B rent at closing: $1,175/month

- Net housing cost: $945/month

- Comparable rent nearby: $1,450/month

- Monthly savings vs. renting: $505/month

The buyer lives in Unit A and rents Unit B. The deal does not produce free housing on day one, but it lowers the buyer’s monthly housing cost by about $505 compared with renting a similar unit nearby. At the same time, the buyer owns the asset, builds equity, and learns how to manage a rental with one tenant household.

At month 14, the buyer relocates for a job opportunity. Instead of selling, they rent Unit A. Combined market rent from both units is about $2,400 per month. If PITIA and loan structure support it, the borrower may explore a DSCR refinance and hold the duplex as a long-term rental.

Three decisions made the scenario stronger:

- The buyer chose a property where the numbers worked at conservative rent.

- The buyer avoided relying on appreciation to justify the purchase.

- The buyer knew the exit before closing: hold the property and convert it into a full rental after moving out.

Dorian Adams-Walker,

Mortgage Loan Originator, NMLS #2442830

Next Steps

House hacking is one of the most practical entry points into real estate investing because it starts with the housing expense you already have. Instead of paying rent with no ownership upside, you use an owner-occupied property to reduce your monthly cost, build equity, and create a path toward future rental income.

The strategy works best when three pieces line up: the right market, the right property type, and conservative underwriting. A duplex with real rent support in a strong Midwest rental market can be a better starting point than a more expensive property in a market where the second unit barely offsets the payment.

Before you make an offer, run the numbers through Ziffy’s cash flow calculator, review the investment property due diligence checklist, and get pre-approved so you know your real budget.

FAQs

Can you house hack with an FHA loan?

Yes. FHA loans can be used for eligible 1-4 unit residential properties when the borrower occupies the property as a primary residence and meets FHA and lender requirements. FHA can be useful for buyers with limited down payment funds, but mortgage insurance and property standards need to be included in the decision.

How long do you have to live in a house hack before moving out?

Many owner-occupied loan programs expect the borrower to occupy the home as a primary residence for at least one year, but rules vary by loan program and file details. Review your occupancy requirement before closing. After you move out, the property may become an investment property, and a DSCR refinance may become an option if the rent supports the debt.

Does house hacking work in expensive markets?

It can, but the math is harder. In high-cost markets such as Los Angeles, New York City, San Francisco, and Seattle, purchase prices often rise faster than achievable rent from the second unit. House hacking tends to work more cleanly in markets where duplexes, triplexes, ADUs, or room-rental homes can be purchased at prices that still allow meaningful rent offsets.

What is the difference between house hacking and the BRRRR method?

House hacking uses your primary residence to reduce housing costs and build equity while you live in the property. The BRRRR method focuses on buying, renovating, renting, refinancing, and repeating with investment properties. Some investors house hack first, then use BRRRR later after building capital and landlord experience.

Is rental income from a house hack taxable?

Yes. Rental income is taxable and is usually reported on Schedule E for individual rental property owners. You may also be able to deduct rental-related expenses and depreciate the rental portion of the property. Speak with a tax professional because mixed-use properties can create depreciation, allocation, and sale-treatment issues.

What happens when I am ready to move out?

You usually have three paths: sell the property, keep it as a long-term rental, or refinance it into a DSCR loan if rental income supports the loan. For investors who want to scale, the DSCR path can be the strongest because it qualifies primarily on the property’s income rather than W-2 income or personal DTI.

Do I need landlord experience before house hacking?

No, but you need to operate professionally from the beginning. Use a written lease, screen tenants, document communication, keep reserves, and treat the rental side as a business. House hacking can teach landlord skills quickly because you are close to the property, but that same proximity makes weak systems more painful.