Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

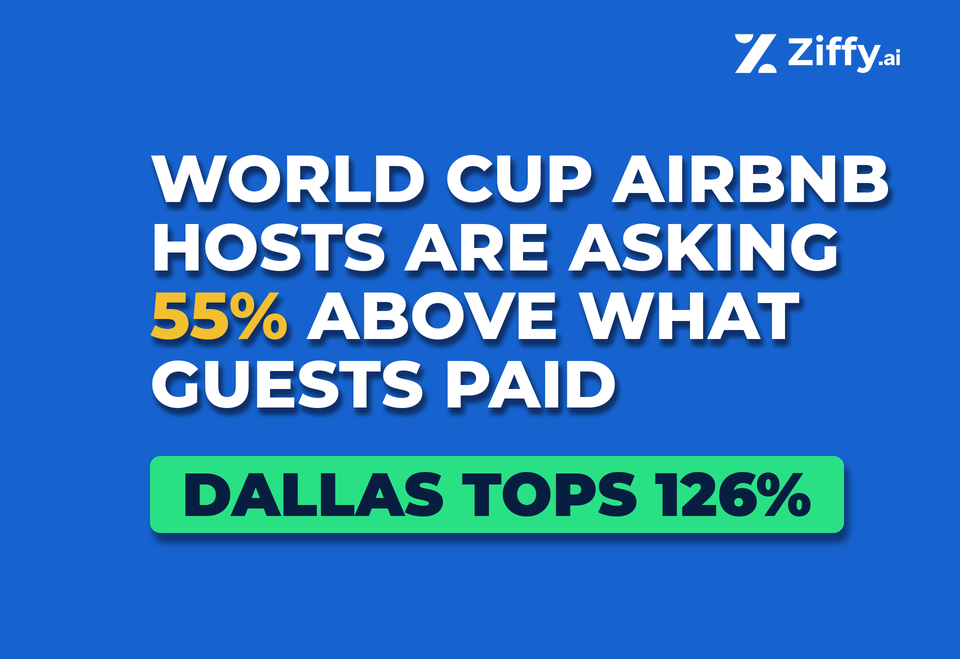

The World Cup’s Airbnb market is showing a pricing gap before the first whistle.

Across the 16 host cities, AirROI’s asking-to-booked gap averages 55% at the city level – hosts are listing available inventory well above the rates guests have actually booked. At the same time, hotel demand is not matching initial forecasts in most U.S. host markets.

AHLA survey data shows that 80% of surveyed hotel respondents report World Cup bookings below expectations, with only Miami and Atlanta showing demand signals that are not predominantly negative.

This analysis examines where Airbnb pricing expectations are most disconnected from booked demand, and where those disconnects overlap with the smallest renter-occupied housing bases.

Table of Contents

Key Highlights

-

Kansas City is the only U.S. host city where AHLA describes World Cup hotel bookings as trailing a typical summer without any major event.

Kansas City is the only U.S. host city where AHLA describes World Cup hotel bookings as trailing a typical summer without any major event.

An estimated 87.5% of surveyed hoteliers report bookings below expectations. It also has the highest Rental Market Exposure Index score at 28.6 and the smallest U.S. host-metro renter base at 305,888 units. - Dallas has the widest Airbnb asking-to-booked gap of any host city: $944 listed vs. $418 booked.

That 126% gap is more than double the 16-city average. The median listing near AT&T Stadium ($616) is itself 47% above the booked rate, and one in four listings is priced at or above $1,403/night. - Guadalajara is the only host city where asking and booked rates have nearly converged.

The gap is just 0.5% – hosts are asking about $197/night, while guests have booked at about $196/night. - Miami is the only U.S. host city where both hotel sentiment and Airbnb pricing signal genuine demand absorption.

Approximately 55% of surveyed hoteliers report booking pace ahead of expectations – no other U.S. host city tops 50%. - Boston Airbnb hosts priced to market, but the market is soft.

Boston’s 19% asking-to-booked gap is the tightest of any U.S. host city, yet 80% of surveyed hoteliers report bookings below expectations.

The World Cup Overpricing Gap Across 16 Host Cities

The World Cup is lifting short-term rental prices, but booked-rate signals are not keeping pace with available-rate expectations in every host city. The 55% average gap masks a wide spread: some markets show strong price absorption, others show hosts pricing ahead of proven demand.

1. Available World Cup inventory carries a $190/night premium over booked stays.

Average daily rates across the host cities rose from $215 in 2025 to $464 in 2026, a 116% year-over-year increase for the tournament window of June 11 through July 19. The increase was sharpest in Mexico, where ADRs rose 182%, followed by Canada at 119% and the United States at 111%.

But the booked-versus-available spread shows a more uneven market. Guests have booked tournament-window stays at an average of $326/night, while remaining available inventory is listed at $517/night – a $190/night spread.

Cluster | 2025 ADR | 2026 ADR | ADR Change | Avg Booked Rate | Avg Available Rate |

|---|---|---|---|---|---|

USA (11 cities) | $246 | $520 | +111% | $358 | $581 |

Mexico (3 cities) | $69 | $195 | +182% | $160 | $202 |

Canada (2 cities) | $258 | $565 | +119% | $402 | $635 |

All 16 cities | $215 | $464 | +116% | $326 | $517 |

Source: AirROI World Cup 2026 STR Data, May 2026 snapshot. Figures are simple (unweighted) averages of city-level values. The 55% asking-to-booked gap cited throughout is the average of 16 individual city-level gaps, not the ratio of aggregate available-to-booked rates. AirROI’s own published aggregate rates may differ due to their equal-weighting methodology.

2. Dallas, Kansas City, and Houston are the clearest overpricing outliers.

Dallas has the widest Airbnb asking-to-booked gap of any World Cup host city – $944/night listed vs. $418/night booked, a 126% gap. Kansas City follows at 93%, with hosts asking $874/night against a booked rate of $454/night. Houston ranks third at 88%, with hosts asking $499/night while guests have booked at $266/night.

These gaps do not mean the listings will remain unbooked. They mean hosts are pricing ahead of the currently proven demand curve. If demand does not catch up, these markets face a higher risk of late-cycle discounting or weaker occupancy.

Rank | City | Country | Booked Rate | Available Rate | Asking-to-Booked Gap |

|---|---|---|---|---|---|

1 | Dallas | USA | $418 | $944 | 126% |

2 | Kansas City | USA | $454 | $874 | 93% |

3 | Houston | USA | $266 | $499 | 88% |

4 | Atlanta | USA | $366 | $646 | 76% |

5 | NYC / NJ | USA | $283 | $473 | 67% |

6 | Toronto | Canada | $251 | $402 | 60% |

7 | Vancouver | Canada | $554 | $868 | 57% |

8 | Mexico City | Mexico | $107 | $163 | 53% |

9 | Philadelphia | USA | $353 | $534 | 51% |

10 | Miami | USA | $438 | $651 | 49% |

11 | Los Angeles | USA | $304 | $441 | 45% |

12 | Monterrey | Mexico | $177 | $247 | 40% |

13 | Seattle | USA | $473 | $616 | 30% |

14 | SF Bay Area | USA | $227 | $292 | 29% |

15 | Boston | USA | $354 | $421 | 19% |

16 | Guadalajara | Mexico | $196 | $197 | 0.5% |

Source: AirROI, May 2026. Gap = (available rate − booked rate) ÷ booked rate.

The pricing disconnect in Dallas extends well beyond the average. The median listed rate near AT&T Stadium is $616/night – 47% above what guests have actually booked at. Even the 25th-percentile listing, at $207, undercuts the $418 booked rate but everything from the median up is priced well beyond it. The top quartile starts at $1,403/night – 3.4 times the booked rate. By contrast, Boston’s median listing ($309) is 13% below its booked rate, and the SF Bay Area’s top-quartile listing ($349) is lower than Dallas’s median.

Put differently: a typical Dallas World Cup listing is priced as though demand will rise to meet the asking price. In markets where demand has met price – Guadalajara, Miami – the gap is under 50%. In Dallas, it is 126%.

3. Guadalajara is the counterexample: prices rose sharply, but booked demand kept pace

Guadalajara is the only host city where asking and booked rates have nearly converged. Hosts are asking about $197/night, while guests have booked at about $196/night, leaving a gap of just 0.5%.

That matters because Guadalajara did not avoid price increases. Its ADR rose 159.7% year over year, and booked rates rose 145.3%. Hosts raised prices sharply, and guests absorbed them.

When ADR growth far outpaces booked-rate growth, the gap widens. Guadalajara’s booked-rate growth nearly matched its ADR growth – the hallmark of real demand absorption.

City | ADR YoY Increase | Booked Rate YoY Increase | Asking-to-Booked Gap |

|---|---|---|---|

Guadalajara | +159.7% | +145.3% | 0.5% |

Dallas | +238.2% | +69.5% | 126% |

Kansas City | +239.9% | +107.6% | 93% |

Houston | +121.0% | +35.3% | 88% |

The Hotel Demand Divide Across 11 U.S. Host Cities

AHLA’s hotel outlook shows that 80% of surveyed respondents across U.S. host markets say World Cup bookings are tracking below initial forecasts (AHLA FIFA World Cup 2026 Hotel Outlook, May 4, 2026). But the underperformance is not uniform: two cities show positive or non-negative signals, four are flat, and five show no incremental lift over a typical summer.

4. Kansas City is the only U.S. host city where AHLA describes World Cup hotel bookings as trailing a typical summer without any comparable event baseline.

Among the 11 U.S. host markets surveyed by AHLA, Kansas City stands alone. An estimated 87.5% of surveyed hoteliers (the midpoint of the reported 85-90% range) report booking pace below expectations.

More critically, Kansas City is the only host market where AHLA describes current bookings as worse with the tournament than without it – not merely below World Cup expectations, but behind what a normal June or July would look like. Every other underperforming host city is at least matching a typical summer.

Dallas and Houston are below World Cup expectations but broadly in line with a normal June or July.

New York is softer than expected but tracking normal summer demand. Boston, Philadelphia, SF Bay Area, and Seattle are also behind expectations and showing no incremental lift over a normal summer respondents described the tournament as a ‘non-event’- but none is singled out by AHLA as performing worse because of the tournament’s net effect the way Kansas City is.

5. Miami is the only U.S. host city where both hotel demand and Airbnb pricing signal genuine demand absorption.

Miami is the strongest positive signal in the AHLA data: approximately 55% of surveyed respondents reported booking pace ahead of expectations and typical summer benchmarks. No other U.S. host city tops 50%.

On the Airbnb side, Miami’s 49% asking-to-booked gap is below the 16-city average, and its +102% match-day premium is moderate – less than a third of the spikes seen in Kansas City (+313%) or Dallas (+310%), and well below the 16-city average.

The contrast with other large markets is instructive. Dallas, Houston, and Kansas City all post Airbnb gaps of 88% or more alongside negative hotel sentiment (AHLA survey). Miami posts the opposite: a moderate pricing gap alongside confirmed hotel demand.

Whether this reflects Miami’s existing international tourism infrastructure, a stronger fixture draw, or the market’s baseline seasonal demand, the result is consistent – Miami is absorbing tournament demand rather than pricing ahead of it.

Atlanta is the second-best signal, but the safer reading is that Atlanta is roughly split, roughly 50% of surveyed respondents in line with or ahead, rather than overwhelmingly positive. Every other U.S. host market shows a negative or flat signal.

Demand Tier | Cities | Interpretation |

|---|---|---|

Positive / non-negative | Miami, Atlanta | Miami is clearly positive; Atlanta is roughly split or better |

Below WC expectations but normal summer | Dallas, Houston, NYC / NJ, | Tournament not adding meaningful incremental lift |

Below expectations, no incremental lift (‘non-event’) | Kansas City, Boston, Philadelphia, | Tournament adding nothing over a normal summer |

Note- Kansas City alone is tracking below a normal summer, not merely flat to it.

Source: AHLA FIFA World Cup 2026 Hotel Outlook, May 4, 2026. AHLA data reflects qualitative survey sentiment, not verified occupancy or revenue figures. For ranged estimates, this analysis uses midpoints: Kansas City 87.5% (from 85-90%), Los Angeles 67.5% (from 65-70%), NYC/NJ 67% (from “approximately two-thirds”).

6. 65-70% of surveyed hoteliers cite visa barriers as the top demand constraint.

Across markets, approximately 65-70% of AHLA respondents cite visa processing delays and geopolitical concerns as the primary constraint on World Cup demand (AHLA, May 2026).

Approximately 50% say early FIFA room block reservations created an artificial demand signal. When those blocks were subsequently released or cancelled, hoteliers were left recalibrating against a weaker-than-expected baseline.

This combination, restricted international arrivals and evaporated block bookings helps explain why even large international gateways like New York and Los Angeles are showing flat rather than elevated demand.

Match-Day Premiums vs. Actual Booking Absorption Across 16 Host Cities

Match-day premiums are the sharpest pricing signal in the dataset, but a high premium does not mean guests are paying it at that level. The gap between peak pricing and actual booking behavior separates markets with real demand from markets where hosts are pricing into a vacuum.

7. Monterrey has the steepest match-day premium at +387%, and booked rates are much closer to available rates. Dallas and Kansas City post comparable premiums, but their booked rates lag significantly.

On peak match days, Monterrey rates spike to +387% above 2025 day-of-week rates, the steepest single-day premium in the dataset. Kansas City follows at +313% and Dallas at +310%. But the critical difference is absorption.

Monterrey’s asking-to-booked gap is 40% and Guadalajara’s is 0.5%, confirming stronger alignment between asking prices and booked demand in Mexican markets.

Dallas at +310% premium carries a 126% gap; Kansas City at +313% carries a 93% gap. High premiums with wide gaps suggest hosts are pricing for peak-night demand that has not materialized broadly.

City | Top Match-Day Premium | Asking-to-Booked Gap | Absorption Signal |

|---|---|---|---|

Monterrey | +387% | 40% | High premium, strong absorption |

Kansas City | +313% | 93% | High premium, weak absorption |

Dallas | +310% | 126% | High premium, weakest absorption |

Guadalajara | +281% | 0.5% | High premium, near-full absorption |

Vancouver | +203% | 57% | Moderate premium, moderate absorption |

Philadelphia | +188% | 51% | Moderate premium, moderate absorption |

Mexico City | +186% | 53% | Moderate premium, moderate absorption |

Atlanta | +185% | 76% | Moderate premium, elevated gap |

Houston | +185% | 88% | Moderate premium, weak absorption |

NYC / NJ | +131% | 67% | Lower premium, elevated gap |

Seattle | +122% | 30% | Lower premium, tighter gap |

Miami | +102% | 49% | Lower premium, moderate absorption |

Toronto | +99% | 60% | Lower premium, elevated gap |

Boston | +67% | 19% | Lower premium, tight gap |

Los Angeles | +54% | 45% | Lower premium, moderate absorption |

SF Bay Area | +47% | 29% | Lowest premium, tighter gap |

Source: AirROI, May 2026. Match-day premium = peak match-day rate vs. 2025 same-day-of-week rate.

The concentration of the steepest premiums on specific match days, rather than sustained elevation across the full 39-day tournament window, suggests that demand in many host cities is event-specific rather than destination-wide.

Note: City-level gaps are rounded to the nearest whole number except where sub-1% precision is material (Guadalajara).

8. Boston’s Airbnb hosts priced to market and the market is soft.

Boston is the mirror image of Dallas. Where Dallas hosts are listing at 3.4 times the booked rate at the 75th percentile, Boston’s asking-to-booked gap is just 19% – the tightest of any U.S. host city.

Hosts near Gillette Stadium are asking an average of $421/night against a booked rate of $354, and even the 75th-percentile listing ($529) sits well below the median listing price in Dallas ($616).

But realistic pricing has not translated into strong bookings. Boston’s booked-rate growth of 34.8% year over year ranks near the bottom of U.S. cities, its match-day premium of +67% is the third-lowest of any U.S. host, and 80% of surveyed hoteliers (AHLA) report bookings below World Cup expectations.

The pattern suggests demand itself is limited, not misdirected by aggressive host pricing. For a market that will host seven World Cup matches including two knockout-round games, that is a weaker return than the fixture schedule would suggest.

9. SF Bay Area booked rates rose just 1.7% year over year, the weakest booked-rate increase of any host city.

While most host cities saw booked rates rise by double or triple digits, the SF Bay Area’s booked ADR increased from $223/night to $227/night, functionally flat.

Los Angeles followed at 8.3%, Toronto at 17.7%, and Miami at 24.0%. At the opposite end, Monterrey booked rates rose 149.8%, Guadalajara 145.3%, and Kansas City 107.6%. Smaller or lower-cost markets are absorbing the most dramatic pricing shifts.

City | 2025 Booked Rate | 2026 Booked Rate | YoY Change |

|---|---|---|---|

Monterrey | $71 | $177 | +149.8% |

Guadalajara | $80 | $196 | +145.3% |

Kansas City | $219 | $454 | +107.6% |

Vancouver | $306 | $554 | +80.8% |

Mexico City | $61 | $107 | +75.2% |

Dallas | $247 | $418 | +69.5% |

Philadelphia | $223 | $353 | +58.3% |

Atlanta | $231 | $366 | +58.2% |

Seattle | $312 | $473 | +51.4% |

NYC / NJ | $198 | $283 | +43.2% |

Houston | $197 | $266 | +35.3% |

Boston | $262 | $354 | +34.8% |

Miami | $353 | $438 | +24.0% |

Toronto | $213 | $251 | +17.7% |

Los Angeles | $280 | $304 | +8.3% |

SF Bay Area | $223 | $227 | +1.7% |

Source: AirROI, May 2026. Booked rates reflect average nightly rates on confirmed bookings for the tournament window.

10. Seattle complicates the demand-softness narrative: strong STR performance, weak hotel sentiment.

Among the five cities where hotel bookings trail both World Cup expectations and typical summer benchmarks (per AHLA), Seattle is an outlier on the Airbnb side. Its booked rate of $473/night is the highest of any U.S. host city, booked-rate growth of 51.4% is well above average, and the 30% asking-to-booked gap signals that hosts near Lumen Field have priced in line with actual demand.

In Boston, Philadelphia, and the SF Bay Area, the other three cities in this demand tier at least one of those Airbnb metrics is also weak. In Seattle, all three are healthy: high absolute booked rate, strong YoY growth, and a tight gap. Yet 80% of surveyed hoteliers (AHLA) report bookings below expectations.

The gap between strong short-term rental performance and soft hotel sentiment raises a question about channel distribution: in a high-cost market with extensive Airbnb supply, some tournament demand may be routing to short-term rentals rather than traditional hotels.

Debjit Saha

Co-Founder and CTOZiffy.ai

Rental Market Exposure Across 11 U.S. Host Metros

The overpricing gap measures where hosts are asking more than guests have paid. This section measures something different: where those pricing disconnects overlap with smaller renter-occupied housing bases, creating greater proportional exposure if short-term rental shifts materialize.

11. Kansas City has 305,888 renter-occupied units – the smallest rental base of any U.S. host metro, roughly 8.5% the size of New York’s.

Kansas City’s renter-occupied housing stock is the smallest among the 11 U.S. host metros, less than half the next-smallest metro (Seattle at 643,789) and roughly 8.5% of the largest (NYC at 3,594,730).

In a metro with this thin a housing cushion, even temporary shifts in short-term rental supply are proportionally larger than the same absolute change in New York or Los Angeles.

Kansas City is the convergence point of this analysis: the smallest rental base, the weakest hotel booking sentiment (per AHLA survey), and the second-widest U.S. asking-to-booked gap.

12. Kansas City tops Ziffy’s Rental Market Exposure Index at 28.6, more than double every other U.S. host city.

The Rental Market Exposure Index combines hotel booking underperformance (AHLA survey) with rental housing stock size (Census). Cities where weak demand signals coincide with smaller rental bases receive higher scores.

The index is a proportional exposure signal, it identifies where a smaller local rental market has less cushion if event-driven shifts occur. It does not measure displacement, does not claim that long-term rental units were converted to short-term rentals, and does not establish a causal relationship between STR supply growth, hotel booking underperformance, or rental housing availability.

Kansas City’s score of 28.6 is 2.3x the second-ranked city (Seattle at 12.4) and 15x the lowest-ranked (NYC at 1.9).

The ranking divides into three tiers: Kansas City alone at the top, a middle cluster of four cities between 9.8 and 12.4, and a lower tier where either stronger demand signals or large rental bases dilute the proportional exposure.

Rank | City | Renter-Occupied Units | Renter Share | AHLA: % Not Ahead of Expectations | Exposure Score |

|---|---|---|---|---|---|

1 | Kansas City | 305,888 | 34.2% | 87.5% | 28.6 |

2 | Seattle | 643,789 | 40.0% | 80% | 12.4 |

3 | Boston | 746,120 | 38.4% | 80% | 10.7 |

4 | SF Bay Area | 776,462 | 44.5% | 80% | 10.3 |

5 | Philadelphia | 818,726 | 33.2% | 80% | 9.8 |

6 | Houston | 1,031,551 | 38.8% | 70% | 6.8 |

7 | Atlanta | 783,586 | 33.9% | 50% | 6.4 |

8 | Dallas | 1,153,805 | 39.9% | 70% | 6.1 |

9 | Miami | 921,750 | 39.5% | 45% | 4.9 |

10 | Los Angeles | 2,320,767 | 51.6% | 67.5% | 2.9 |

11 | NYC / NJ | 3,594,730 | 48.5% | 67% | 1.9 |

Exposure Score = (AHLA % below expectations) ÷ (renter-occupied units ÷ 100,000).

13. New York’s rental cushion: a 67% Airbnb gap that barely registers on the Exposure Index.

The contrast between Kansas City and New York illustrates why absolute pricing gaps do not translate directly into local market impact.

New York’s 67% Airbnb asking-to-booked gap is higher than six of the eleven U.S. host cities – higher than Philadelphia (51%), Miami (49%), Los Angeles (45%), Seattle (30%), the SF Bay Area (29%), and Boston (19%). Two-thirds of surveyed hoteliers report bookings below expectations (AHLA).

By those measures alone, New York would appear to be a strained market. But the metro area’s 3.59 million renter-occupied units, nearly 12 times the size of Kansas City’s renter base means the same proportional shift in short-term rental supply that would visibly compress availability in Kansas City dissipates across a housing stock that dwarfs the tournament’s footprint.

The Exposure Index reflects that: New York scores 1.9, the lowest of any U.S. host metro. Scale is insulation.

14. Los Angeles is the only U.S. host metro where renters outnumber homeowners, 51.6% renter-occupied.

Los Angeles has the highest renter share of any U.S. host metro at 51.6%, the only one above 50%. NYC follows at 48.5%.

A high renter share does not mean World Cup Airbnb demand harms renters. It means renters make up a larger share of the occupied housing base, relevant context when local officials or housing reporters evaluate event-driven accommodation pressure.

The 100,000-Listing Surge Meets Uneven Demand

Airbnb’s supply expansion is real. The demand picture is more complicated.

15. Airbnb says more than 100,000 new homes listed in host cities since October 2025, but hotel booking sentiment has not matched the supply growth in most U.S. markets.

According to Airbnb, over 100,000 homes have listed on the platform in host cities for the first time since October 2025, supported by a $750 new-host incentive for entire-home listings and an 80% year-over-year increase in host-city searches (Airbnb Newsroom, May 2026; Airbnb Newsroom, February 2026).

Around one in six guests booking tournament-time stays is a first-time Airbnb user, and 77% of entire-home listings still available are priced under $500/night (Airbnb, May 2026).

That is the supply-side picture. The demand side is uneven. In the three U.S. cities with the widest overpricing gaps, hotel sentiment (per AHLA survey) ranges from flat to the weakest in the country:

City | Asking-to-Booked Gap | AHLA Hotel Sentiment |

|---|---|---|

Dallas | 126% | 70% below expectations; in line with typical summer |

Kansas City | 93% | 87.5% below expectations; trailing typical summer |

Houston | 88% | 70% below expectations; in line with typical summer |

Miami | 49% | 55% ahead of expectations |

Guadalajara | 0.5% | N/A (not surveyed) |

The pattern is not uniform. Guadalajara reached near-full price convergence. Miami’s positive hotel sentiment and moderate Airbnb gap confirm real demand absorption.

These markets show that host-city STR expansion can align with actual demand but across the broader tournament footprint, that alignment is the exception rather than the norm.

Amresh Singh

Founder and CEOZiffy.ai

Methodology

This analysis combines three datasets. Short-term rental pricing comes from AirROI’s World Cup 2026 dataset – 16,000 active Airbnb listings (the 1,000 closest qualifying listings to each of the 16 host stadiums), captured in a May 2026 snapshot for the June 11-July 19 tournament window and compared against the same calendar dates in 2025.

Hotel demand sentiment comes from the AHLA FIFA World Cup 2026 Hotel Outlook (May 4, 2026), a qualitative survey of hoteliers across the 11 U.S. host markets. Rental housing stock comes from the U.S. Census Bureau’s 2020-2024 ACS 5-Year Estimates (Table B25003), at the metropolitan-statistical-area level.

All city-level averages are simple (unweighted) means. Each city’s asking-to-booked gap is (available rate − booked rate) ÷ booked rate; the 55% figure cited throughout is the average of the 16 individual city gaps, not the ratio of aggregate rates.

Percentages are calculated on unrounded underlying values, so the rounded dollar figures shown in tables may not reproduce them exactly. The Rental Market Exposure Index and its inputs are defined in Ranking Calculations below

Sources

1. AirROI World Cup 2026 STR Data

16,000 active Airbnb listings sampled across 16 host cities (1,000 closest qualifying listings to each stadium, ranked by proximity). May 2026 snapshot. Tournament window: June 11-July 19, 2026, compared against same calendar dates in 2025.

AirROI’s press kit states that its World Cup STR data is free to use in editorial coverage with attribution. Metrics used: average daily rate (ADR), booked rate, available rate, year-over-year changes, match-day premiums, and price distribution (P25/P50/P75).

2. Airbnb Press Releases

Airbnb’s May 2026 release was used for the 100,000 new-listing figure, first-time guest share, and under-$500 availability claim. Airbnb’s February 2026 release was used for the $750 new-host incentive, 80% year-over-year search growth, and the Deloitte earnings estimate.

Airbnb’s 100,000 new-listing figure is an aggregate across all 16 host cities – city-level allocation is not available from the source. AirROI’s 16,000-listing sample is a separate dataset.

3. American Hotel & Lodging Association (AHLA) FIFA World Cup 2026 Hotel Outlook

Published May 4, 2026. Survey of hoteliers across 11 US host markets. Reflects April 2026 booking sentiment. Qualitative survey (percentage of respondents reporting above/below expectations), not hard occupancy or revenue figures. Does not cover Canadian or Mexican host cities.

For ranged figures, this analysis uses midpoint estimates: Kansas City 87.5% (from 85-90%), Los Angeles 67.5% (from 65-70%), NYC/NJ 67% (from “approximately two-thirds”). For Atlanta and Miami, where AHLA reports positive or neutral sentiment, this analysis inverts to derive the below-expectations measure for index consistency: Atlanta 50%, Miami 45%.

4. U.S. Census Bureau – American Community Survey 2020-2024 5-Year Estimates

Metropolitan Statistical Area level for 11 US host metros. Provides total occupied housing units, owner-occupied units, and renter-occupied units. Downloaded May 25, 2026.

Ranking Calculations

1. Asking-to-Booked Pricing Risk (Ranking 1)

Cities ranked by: (available rate − booked rate) ÷ booked rate × 100. Covers all 16 host cities.

The 55% figure used throughout this report is our own recomputation: the simple average of the 16 individual city-level gaps shown in the ranking table. AirROI publishes a 56% topline gap computed across its full 16,000-listing dataset; the one-point difference is methodological – averaging 16 city-level ratios is not the same as a listing-level average across all markets.

For the same reason, dividing AirROI’s aggregate rates of $497 (available) and $332 (booked) directly yields about 50%, because larger markets weigh differently in an aggregate than in an equal-weighted average of cities. We use our recomputed 55% throughout so the headline number is reproducible directly from the table.

2. Rental Market Exposure Index (Ranking 2)

Score calculated as: (AHLA % below expectations) ÷ (renter-occupied housing units ÷ 100,000).

Higher scores indicate greater proportional exposure, markets where weak hotel demand signals coincide with smaller renter-occupied housing bases. Covers 11 US host cities only.

The index does not include the Airbnb asking-to-booked gap directly in its formula; Airbnb gap is analyzed separately and discussed alongside the exposure score where relevant.

Limitations

- This analysis measures the gap between Airbnb host pricing and guest booking behavior, contextualized against hotel sentiment and housing stock. It does not measure the number of long-term rental units converted to short-term rentals, does not claim World Cup STR listings were previously occupied by long-term tenants, and does not establish a causal relationship between STR supply growth, hotel booking underperformance, or rental housing availability. The Rental Market Exposure Index is a proportional exposure signal, not a displacement measure.

- AirROI samples 1,000 stadium-adjacent qualifying listings per host city, not the total metro short-term rental market. Results reflect the stadium-proximate accommodation market and may not represent metro-wide conditions.

- AHLA data reflects hotelier survey sentiment (subjective responses), not verified occupancy, revenue, or booking transaction data.

- Census ACS 5-year estimates are a rolling average across 2020–2024 and may not reflect 2025–2026 housing stock changes.

- Airbnb’s 100,000 new-listing figure is an aggregate across all 16 host cities. City-level allocation is not published.

- The co-occurrence of Airbnb pricing gaps, weak hotel booking sentiment, and small rental market size does not establish that STR supply growth caused hotel underperformance or affected long-term rental availability.

- Canadian and Mexican host cities are included in the STR pricing analysis (Ranking 1) but excluded from the Rental Market Exposure Index (Ranking 2) due to different national census methodologies.

About Ziffy

Ziffy.ai is an all-in-one, AI-native real estate investment platform designed to help investors discover, analyze, and finance U.S. real estate opportunities.

The platform combines AI-native property search with detailed investment analysis on every listing, including rental income potential, cash flow, and return metrics. Ziffy also provides access to specialized financing solutions such as DSCR loans, fix-and-flip loans, and bridge loans, enabling investors to evaluate and execute opportunities in one place.