Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Quick Answer

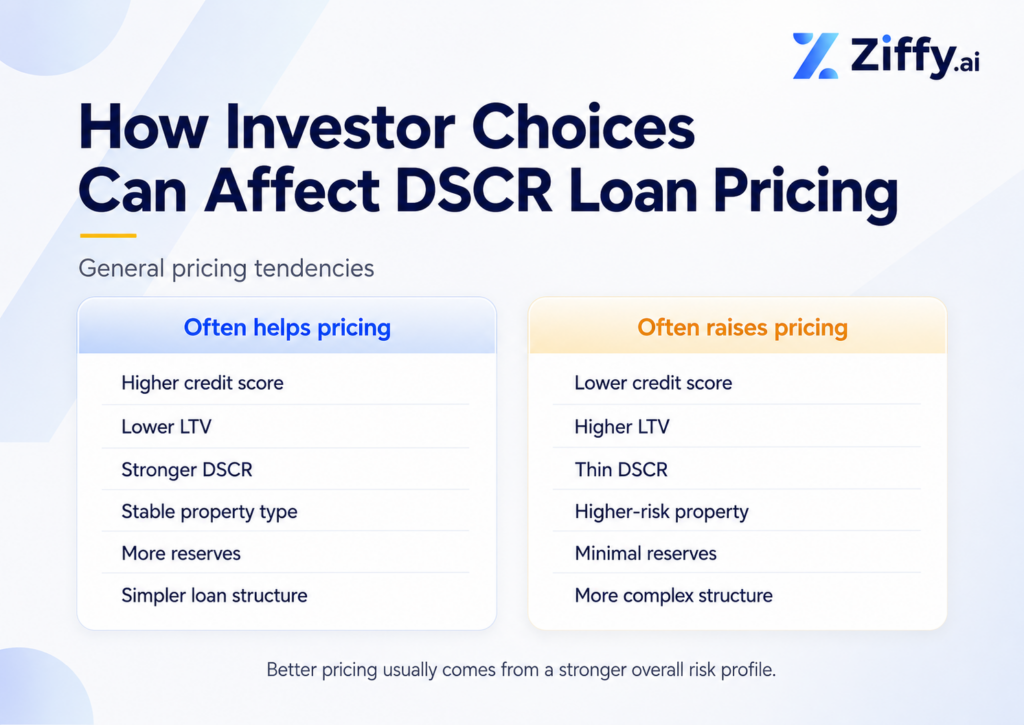

A DSCR loan rate begins with current market pricing, then changes according to the risk and structure of the transaction. The seven factors investors can influence most are credit score, loan-to-value ratio, debt service coverage ratio, property profile, loan amount, cash reserves, and loan terms.

Improving one factor can help, but lenders price the complete file. Strong credit may not secure the best terms when the property has thin cash flow, high leverage, limited reserves, or a complex loan structure.

A larger down payment can reduce LTV and strengthen the property’s DSCR.

Underwriting uses supportable rent and full PITIA, not an optimistic cash-flow estimate.

A lower interest rate may require discount points, stricter prepayment terms, or a different loan structure.

Compare quotes using the same loan amount, LTV, term, lock period, points, and prepayment option.

A debt service coverage ratio loan, commonly called a DSCR loan, qualifies an investment property mainly through its rental income rather than the borrower’s personal debt-to-income ratio.

We calculate DSCR using this formula:

DSCR = Gross monthly rental income ÷ PITIA

PITIA includes principal, interest, property taxes, insurance, and association dues when applicable. A ratio of 1.00 means the qualifying rent equals the monthly housing obligation. We generally prefer a DSCR of 1.00 or higher for a standard file, although eligible properties below 1.00 may qualify through our no-ratio option.

Business-purpose investment loans can also follow a different regulatory framework from owner-occupied consumer mortgages. Under 12 CFR 1026.3(a), credit extended primarily for a business or commercial purpose is exempt from Regulation Z. State law and lender underwriting requirements still apply.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

When I review a DSCR deal, I am not looking for a perfect number on paper. I want to know whether the property still works when the assumptions become less comfortable. If the loan only qualifies using the highest possible rent and the lowest possible expenses, the margin may be too thin. A stronger file gives the investor room for vacancies, repairs, insurance increases, and the other costs that rarely stay exactly where you expect them.

Table of Contents

7 DSCR Pricing Factors That Investors Can Control

1. Credit Score

DSCR underwriting reduces the emphasis on personal income, not on credit. Credit history can affect the interest rate, discount points, maximum leverage, and available loan structures.

We accept credit scores starting at 620, subject to the property, loan structure, leverage, and complete borrower profile. Reaching the minimum does not guarantee the strongest pricing because the full transaction still matters.

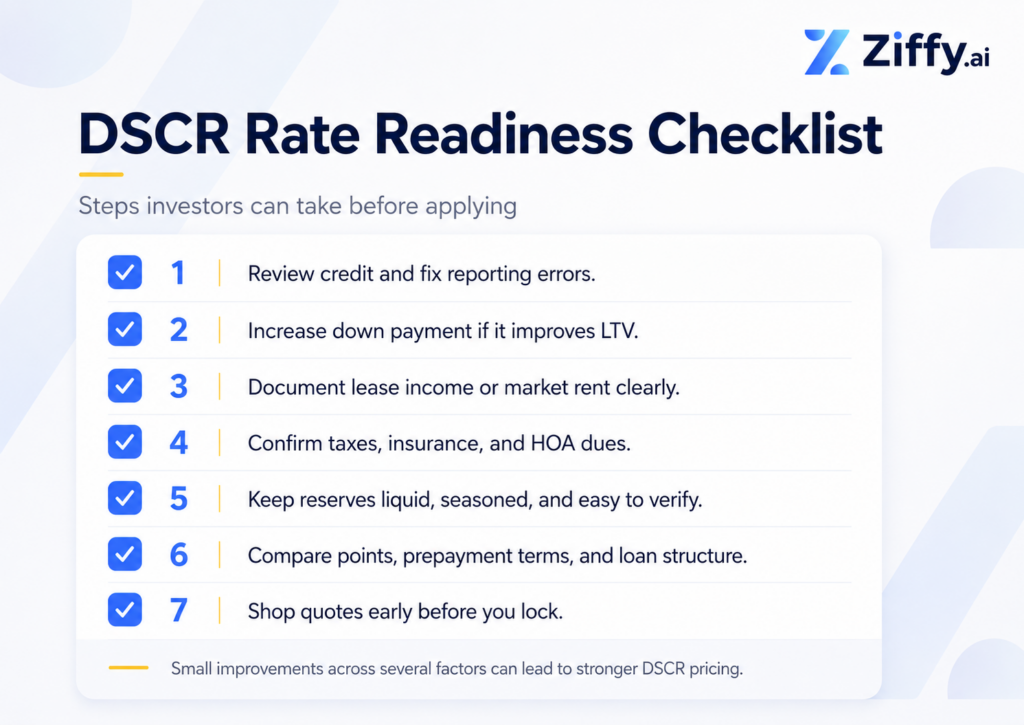

Review your credit reports before applying. Correct legitimate reporting errors early and avoid opening new accounts or increasing balances while the loan is being priced or underwritten.

2. Down Payment and Loan-to-Value Ratio

Loan-to-value ratio, or LTV, compares the loan amount with the property’s value. A lower LTV gives the lender more equity protection and may reduce risk-based pricing adjustments.

A larger down payment can also strengthen DSCR. Borrowing less reduces principal and interest, which lowers PITIA when rent and the other property expenses remain unchanged.

The largest down payment is not automatically the best choice. Investors also need liquidity for closing costs, reserves, repairs, vacancies, and future acquisitions. We can price several LTV options so the investor can see whether contributing more capital creates a meaningful improvement.

Jeff Larrabee

Sr. Customer Loan Specialist

Ziffy Mortgage

NMLS #482306I usually ask investors what they want their cash to accomplish before we decide how much to put down. More equity may improve the rate and the DSCR, but it can also leave the borrower with less money for repairs, reserves, or the next property. The goal is not to make the down payment as large as possible. It is to find the point where the loan gets meaningfully better without weakening the investor’s overall plan.

3. Debt Service Coverage Ratio

A stronger DSCR gives the property more room to cover its mortgage obligation. The ratio can weaken when taxes, insurance, HOA dues, or the final interest rate are higher than the preliminary estimates.

Consider a Miami property with:

- Estimated monthly rent: $3,376

- PITIA: $2,451

The DSCR is:

$3,376 ÷ $2,451 = 1.38

The estimated rent is 38% higher than the monthly housing obligation. The calculation also shows why the interest rate affects qualification. Interest is part of PITIA, so a higher rate raises the denominator and reduces DSCR unless another input changes.

For a borderline file, confirm which rent figure underwriting will accept, obtain a realistic insurance quote, and test whether a lower LTV or a different payment structure improves the ratio. Our DSCR calculator lets investors adjust the purchase price, down payment, rate, rent, and property expenses before applying.

4. Property Type, Use, and Condition

The lender prices the collateral as well as the borrower. A stabilized rental with supportable market rent usually presents a cleaner risk profile than a property with deferred maintenance, unusual features, mixed use, or difficult-to-document income.

We finance eligible:

- Single-family homes

- Townhouses

- Condominiums

- Multifamily properties with two to ten units

Larger multifamily and commercial transactions may be handled through our commercial financing channel.

Appraisal findings, condominium eligibility, short-term-rental use, property condition, association dues, and the number of units can affect the available program and final pricing. A property that requires substantial repairs or lease-up may be better suited to a bridge loan before moving into permanent DSCR financing.

5. Loan Amount

We offer DSCR loans from $100,000 to $10 million, subject to the borrower, property, loan purpose, leverage, and complete file.

Pricing and underwriting requirements may change at different balance thresholds. When the proposed loan amount is close to an LTV or program boundary, we can compare nearby loan amounts.

A modest reduction in proceeds may improve the terms. In other cases, contributing more cash may produce little measurable benefit. The numbers should be compared before the investor commits additional capital.

6. Cash Reserves

Cash reserves are liquid funds remaining after the down payment and closing costs. They provide a cushion for vacancies, repairs, insurance increases, or delayed rent payments.

We generally require at least two months of reserves for a DSCR loan. The final requirement can vary with leverage, loan size, property type, borrower profile, and the number of financed properties.

More reserves do not automatically produce a lower interest rate. They can, however, strengthen the complete file and help the borrower qualify for a more favorable structure.

7. Loan Structure, Points, and Prepayment Terms

The interest rate is only one part of the loan’s price. A fully amortizing mortgage, an interest-only DSCR loan, and an adjustable-rate structure can produce different payments, qualification results, and long-term costs.

The Consumer Financial Protection Bureau’s guidance on points and lender credits explains the trade-off:

- Discount points increase the upfront cost in exchange for a lower rate.

- Lender credits reduce upfront closing costs in exchange for a higher rate.

One point equals 1% of the loan amount, but it does not buy a fixed rate reduction. The improvement varies by lender, market conditions, and transaction.

Use this calculation before paying points:

Break-even months = Cost of points ÷ Monthly payment savings

Paying points makes more sense when the expected holding period comfortably exceeds the break-even period.

Review the prepayment terms just as closely. A prepayment penalty can create a significant cost when the property is sold or the loan is refinanced during the penalty period. Request comparable pricing with and without the penalty when both options are available.

How to Compare DSCR Loan Quotes

Ask each lender to price the same:

- Loan amount and LTV

- Fixed or adjustable term

- Amortization period

- Interest-only option

- Discount points or lender credits

- Prepayment structure

- Rate-lock period

A rate lock generally protects the quoted rate through closing when the loan closes within the stated period and the application does not materially change. Ask about extension fees before locking.

The best quote is the structure that fits the investor’s expected hold period, cash-flow target, and capital plan, not simply the lowest headline rate.

Jeff Larrabee

Sr. Customer Loan Specialist

Ziffy Mortgage

NMLS #482306When two quotes are close, I look beyond the rate. I want to know how many points the borrower is paying, what happens if the property is sold or refinanced early, and whether the payment still supports the investor’s cash-flow target. A slightly lower rate can become the more expensive choice if it comes with heavy upfront costs or terms that do not match the investor’s hold period.

FAQs

What Has the Biggest Effect on a DSCR Loan Rate?

There is no universal single factor. Credit, LTV, DSCR, property risk, reserves, and loan structure work together to determine pricing.

Can a High DSCR Offset a Lower Credit Score?

A strong DSCR can improve the overall file, but it does not erase the borrower’s credit profile. The transaction must still meet the applicable credit, leverage, and property requirements.

Can a Larger Down Payment Improve Both the Rate and DSCR?

Yes. A larger down payment can lower LTV and reduce principal and interest. The investor should also consider how much liquidity will remain after closing.

Is the Lowest Interest Rate Always the Best Quote?

No. The lowest rate may require more points, a longer prepayment penalty, or higher upfront costs. Compare the total cost over the period you expect to keep the loan.

Can a Property Below a 1.00 DSCR Qualify?

Possibly. We may consider eligible properties below 1.00 through our no-ratio DSCR option, usually with a stronger equity position or more conservative leverage elsewhere in the file.