Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Quick Answer

A rate buydown on a debt service coverage ratio, or DSCR, loan makes sense when the upfront cost of discount points is outweighed by the monthly payment savings, the lower payment strengthens the property’s rental coverage, and the investor expects to keep the loan beyond the break-even period.

The basic formula is simple:Break-even period = cost of discount points ÷ monthly payment savings

For rental investors, the decision goes deeper than that. A lower rate can reduce monthly principal and interest, but it can also change the property’s monthly payment obligation, cash flow, and DSCR. On a DSCR loan guide, where the property’s rental income carries the qualification logic, the rate buydown question becomes: does paying points make the deal stronger, or does it only make the rate look better?

At Ziffy, we usually see points work best for investors who plan to hold the rental long enough to recover the upfront cost, already have enough liquidity after closing, and are using the lower payment to improve a real investment metric. Points are much harder to justify when the investor expects to refinance soon, sell quickly, needs more cash for reserves, or is trying to fix a property that does not work at the purchase price.

Quick note on terminology: This article focuses on permanent rate buydowns through discount points. A permanent buydown lowers the note rate for the life of the loan, unless the investor refinances or pays off the loan. Temporary buydowns, such as 2-1 buydowns, reduce payments for a limited early period and may not use the same payment assumption for long-term DSCR qualification.

Table of Contents

What Is a Rate Buydown on a DSCR Loan?

A rate buydown on a DSCR loan usually means the borrower pays discount points at closing in exchange for a lower interest rate. The Consumer Financial Protection Bureau explains discount points as an upfront fee tied to a lower interest rate, with one point equal to 1% of the loan amount.

On a $400,000 DSCR loan, one point would cost $4,000 and half a point would cost $2,000. The investor pays that money upfront, usually as part of closing costs, in return for a lower note rate.

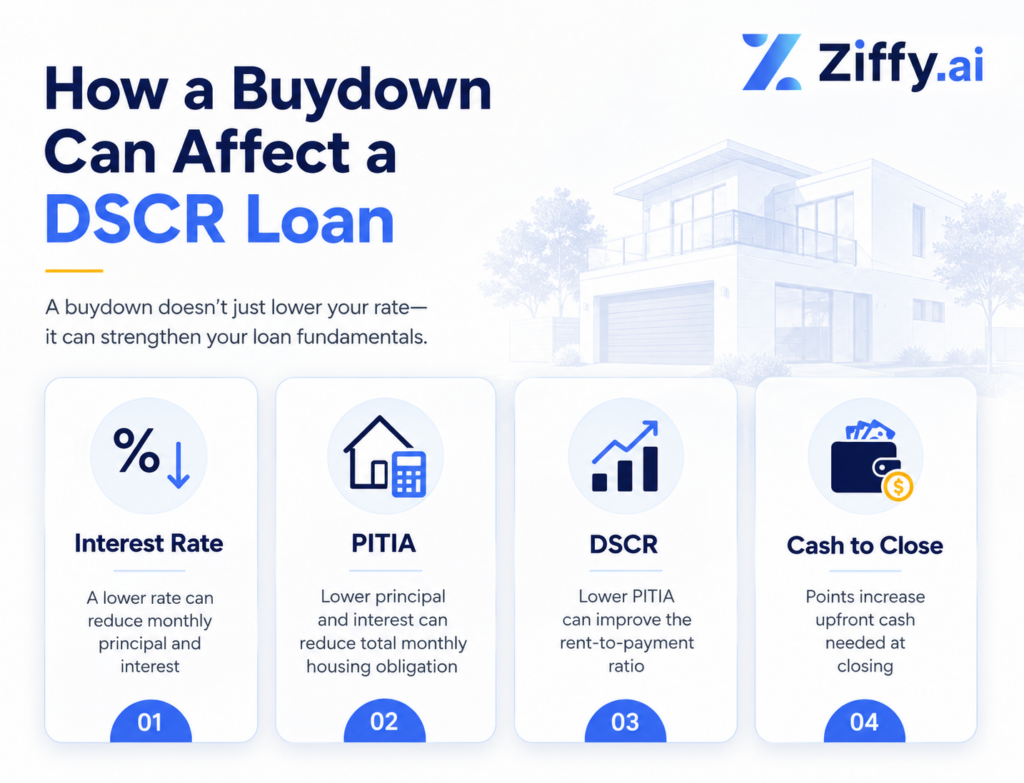

For an owner-occupied borrower, points are usually a payment and interest-savings question. For a rental investor, the math affects the deal in four places:

PITIA includes principal, interest, taxes, insurance, and association dues when applicable. Since DSCR is commonly calculated as gross monthly rent divided by PITIA, even a modest payment reduction can matter if the deal is close to a key rental-coverage threshold.

A rate buydown should not be treated like a coupon on the interest rate. On a DSCR file, we are looking at whether the lower payment actually improves the rental coverage, protects cash flow, or helps the investor hold the property more comfortably. If it only lowers the rate but drains reserves, it may not be the better structure.

How Discount Points Affect DSCR

At Ziffy, DSCR is calculated as:

DSCR = gross monthly rent ÷ PITIA

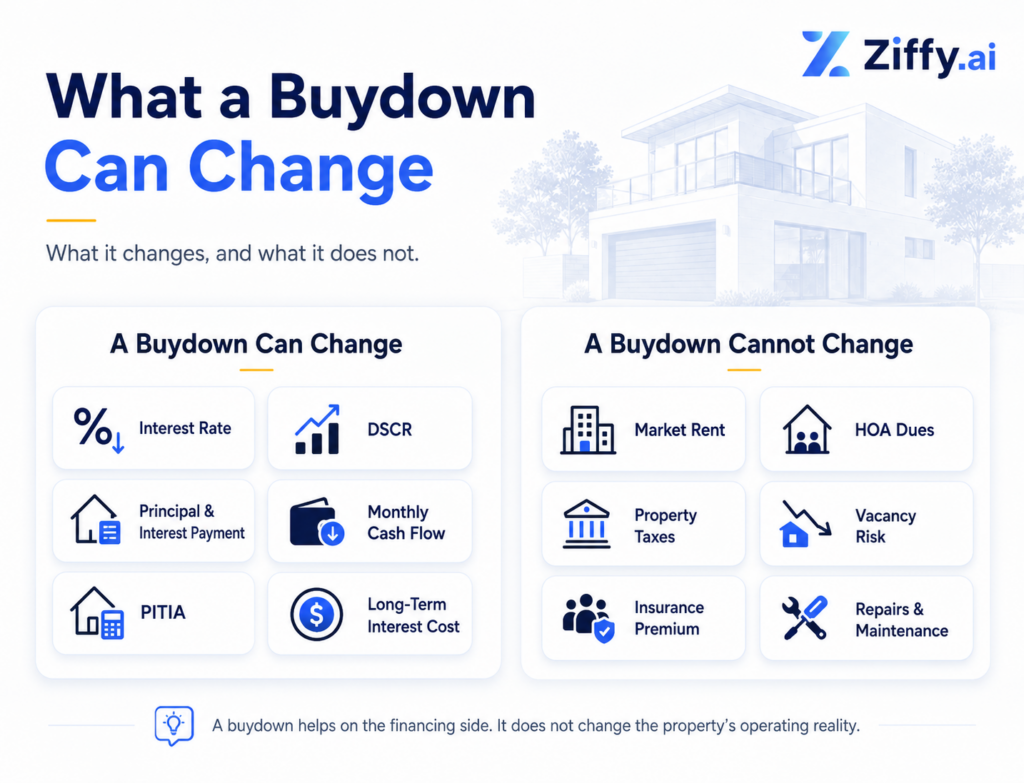

A rate buydown affects the denominator. It can lower the principal and interest portion of the monthly payment, which can reduce PITIA. It does not change the rent, property taxes, insurance premium, homeowners association dues, repairs, vacancy, or property management cost.

Technically speaking, the rate buydown matters because it works on the payment side of the DSCR formula. The rent numerator stays the same, but the PITIA denominator can move lower if the interest rate reduction is strong enough. That is why a rate buydown can improve DSCR even when the property’s rent estimate has not changed.

Here is the practical split:

What most guides do not mention is that points can sometimes affect the financing path, not only the payment. A property that sits close to a DSCR threshold may look different after the monthly principal and interest payment is reduced. A property far below workable coverage usually needs a different fix: lower purchase price, more down payment, stronger rent support, or a different loan structure.

Rate buydown analysis belongs in the same deal worksheet where the investor is reviewing rent, PITIA, DSCR, reserves, and exit plan. It should not sit as a separate rate-shopping exercise.

The Break-Even Test for DSCR Discount Points

The first test is the classic break-even calculation:

Cost of discount points ÷ monthly payment savings = break-even period

Suppose an investor pays $4,000 in points and saves $125 per month.

$4,000 ÷ $125 = 32 months

The investor needs to keep the loan for roughly 32 months before the monthly savings recover the upfront cost. After that point, the savings begin to work in the investor’s favor.

The CFPB’s discount points and lender credits guide explains the same borrower tradeoff: paying points means paying more upfront to lower the rate, while lender credits generally mean paying less upfront in exchange for a higher rate.

For DSCR investors, the break-even test should answer three questions at once:

- How long will I keep this loan? (Points need time to pay off)

- Does the lower payment improve DSCR enough to matter? (The loan file may be stronger if PITIA drops)

- Does paying points leave enough reserves after closing? (A lower payment is not helpful if the investor is undercapitalized)

A rate buydown starts to look stronger when all three answers point in the same direction.

The Bigger Question: Points or a Better Deal?

Before paying points, investors should ask whether the property itself needs work.

A better purchase price can improve the investment more than a slightly lower rate. So can a lower loan amount, stronger rent support, a more accurate insurance quote, or choosing a property with fewer association costs. Points should not become a way to force a thin deal through the numbers.

Ziffy’s AI-native investment workflow lets investors review rent, cash flow, and DSCR before the loan conversation starts, so the rate decision is tied to the deal from the beginning. Investors can review investment properties, compare rent and cash flow assumptions, test DSCR, and then decide which financing structure fits the deal. Rate is one input. It should not carry the entire investment decision.

A property that only works after an expensive buydown may still be too tight. A property that works before points may become stronger with a buydown if the investor plans to hold it long enough.

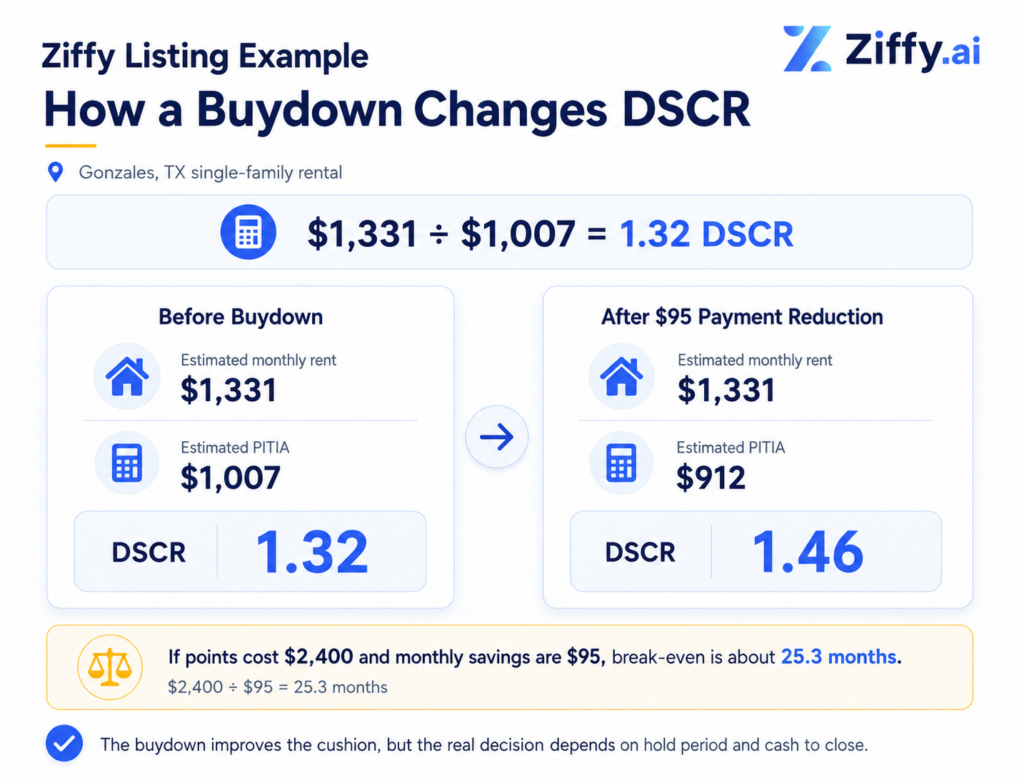

Ziffy Listing Example: How a Buydown Can Change DSCR

A single-family rental in Gonzales, TX listed on Ziffy had an estimated monthly rent of $1,331 and estimated monthly PITIA of $1,007, producing a 1.32 DSCR.

$1,331 ÷ $1,007 = 1.32 DSCR

Now look at what happens if a rate buydown lowers the monthly payment by $95.

The buydown makes a bigger difference here because the property’s monthly PITIA is relatively low. A $95 reduction may not look huge on its own, but against a $1,007 monthly payment, it meaningfully improves the rent-coverage ratio.

This does not mean the buydown turns a weak property into a strong one. The property already had positive rent coverage before the buydown. The lower payment simply gives the investor more breathing room and a stronger DSCR cushion.

The second part of the decision is the break-even period. If the investor paid $2,400 in points to save $95 per month, the break-even period would be about 25 months.

$2,400 ÷ $95 = 25.3 months

For an investor planning to hold the loan for several years, that math can be worth reviewing. For an investor expecting to refinance or sell in 18 months, the savings may not last long enough to justify the upfront cost..

When Discount Points Actually Pay Off on a DSCR Loan

Discount points tend to work best when the investor’s hold period, cash position, and property numbers all support the decision.

1. The Investor Plans to Hold the Rental Long Term

A long-term rental with stable rent support gives the buydown more time to recover the upfront cost.

For investors buying stabilized single-family rentals, townhomes, condos, or small multifamily properties, a lower payment can help protect monthly cash flow over a longer hold. The key is not the lower rate by itself. The key is the length of time the investor expects to keep the loan.

In our experience, investors get the most value from a buydown when they confirm their hold plan before closing. Investors who pay points first and work out the hold plan later sometimes find the loan refinanced or paid off before they hit break-even — erasing the savings entirely.

If the break-even period is 32 months and the investor expects to hold the loan for seven years, points deserve a serious look. If the investor expects to refinance after lease-up or sell within two years, the upfront cost becomes harder to defend.

2. The Lower Payment Moves the Property Into a Better DSCR Position

A buydown is more valuable when it improves the property’s DSCR enough to affect the file.

For example, a property with a 0.98 DSCR may move above 1.00 if the payment drops enough. A property at 1.21 may move closer to 1.25. A property already at 1.55 may not need the buydown for qualification, though the lower payment may still help cash flow.

The investor should compare DSCR before and after points, not just rate before and after points.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

The mistake is looking at points as a rate decision only. On an investor file, I want to know what the points do to PITIA, what they do to DSCR, and what cash the borrower has left after closing. If the buydown improves the number but leaves the investor too tight, we need to look at a different structure.

3. The Investor Has Enough Cash After Closing

Points increase cash to close, which makes post-closing liquidity the first constraint to evaluate.

A borrower may have enough money to pay points, but still be better off keeping that cash for reserves. Rental properties need room for vacancy, repairs, tenant turnover, insurance deductibles, and tax changes. A lower monthly payment does not replace liquidity.

This is especially relevant because post-closing reserve requirements can affect how strong the file looks. Investors should not spend reserve money on points just to improve the monthly payment.

4. The Rent Support Is Stable

A lower rate can improve the loan side of the equation, but it cannot repair weak rent assumptions.

If the rent estimate is too aggressive, the DSCR may still be misleading after points. The better move is to confirm rent support first, then decide whether a buydown helps. This matters for long-term rentals and becomes even more important with short-term rentals, where seasonal income can create a tempting but risky model.

The strongest buydown candidates are usually properties where rent is supportable, taxes and insurance are reasonably firm, and the investor already understands the likely monthly operating picture.

5. The Investor Is Not Expecting a Quick Refinance

A refinance can end the original loan before the investor reaches break-even.

This does not make points automatically wrong, but it raises the bar. If the investor is buying a property, making improvements, stabilizing the rent, and planning to refinance soon, paying points on the first loan may not deliver enough savings.

For transitional deals, a bridge loan may fit the early stage better, with DSCR financing used later once the property is stabilized.

When Discount Points Usually Do Not Pay Off

Points can be useful, but they are not always the smartest use of cash.

1. The Hold Period Is Too Short

A short hold weakens the case for paying points. If the investor sells, refinances, or pays off the loan before break-even, the upfront cost may never be recovered.

The investor may buy the property, improve rent, season the asset, then refinance. In that case, the buydown decision should be tied to the actual refinance plan, not the maximum loan term.

2. The Property Has a Cash Flow Problem

Some deals are not tight because of the rate, but because the purchase price is too high, rent is too low, taxes are heavy, insurance is expensive, or HOA dues are eating too much of the margin.

A buydown may soften the payment, but it should not hide the core issue. If the property does not work without points, the investor should revisit the acquisition before spending more cash at closing.

If a deal only works because the borrower bought down the rate, I want to see why. Sometimes points are the right lever. Other times, the better answer is more equity, a lower purchase price, or a property with stronger rent support.

3. The Investor Needs More Cash for Repairs or Reserves

Cash spent on points is cash that cannot be used elsewhere, which is fine for some investors, but for others, the same money is better used for lease-up, property improvements, furnishings, reserves, or another acquisition. The best use of cash depends on the investor’s full portfolio plan.

This also connects to DSCR loan qualification requirements, because the overall file is not judged only by the rate. Credit, loan purpose, down payment, reserves, property type, and rent support all shape the final loan structure.

4. The Same Cash Would Work Better as a Larger Down Payment

A larger down payment can reduce the loan amount, improve the loan-to-value ratio, or LTV, lower monthly payment, and improve DSCR. Points lower the rate, but they do not reduce the principal balance.

Here is the decision frame:

The minimum down payment on a DSCR loan should be reviewed before deciding whether extra cash should go toward points or equity. A buydown can be smart, but a stronger down payment may do more for certain files.

5. The Loan Has a Prepayment Penalty or Likely Early Payoff

If the investor pays points, then also faces a cost to exit the loan early, the break-even analysis should include both items. The CFPB’s Loan Estimate explainer is a useful reminder to review loan terms, projected payments, closing costs, and prepayment penalty disclosures before moving forward.

Discount Points vs. Lender Credits on DSCR Loans

Discount points and lender credits move in opposite directions. With discount points, the investor pays more upfront in exchange for a lower rate. With lender credits, the investor may accept a higher rate in exchange for lower upfront closing costs.

For DSCR investors, lender credits may make sense when cash preservation matters more than the lowest possible rate. This can happen when the property needs repairs, the investor wants stronger reserves, or the hold period is uncertain.

Discount points may make more sense when the investor has enough liquidity, wants the lower payment, and plans to keep the loan well beyond break-even.

Purchase, Refinance, and Cash-Out: How the Buydown Decision Changes

The rate buydown decision changes depending on the loan purpose.

DSCR Purchase Loan

On a purchase, points add to cash needed at closing. The investor is already paying down payment, closing costs, prepaid items, insurance, and possibly reserves. Paying points can still make sense if the lower payment improves DSCR and the investor has enough cash left after closing.

A purchase buydown is strongest when the property is a long-term rental and the investor is not sacrificing liquidity to get the lower rate.

DSCR Rate-and-Term Refinance

A rate-and-term refinance can be a cleaner setting for a buydown if the investor is moving into a long-term hold structure.

The key question is whether the new loan will stay in place long enough to recover the points. If another refinance is likely soon, the investor should be cautious.

DSCR Cash-Out Refinance

Cash-out refinances require the sharpest review because the investor is usually trying to pull capital out of the property.

The CFPB’s discount-points data spotlight found that discount points were especially common among cash-out refinance borrowers in the first three quarters of 2023, with nearly 9 out of 10 paying some amount of discount points.

The CFPB data captures a specific rate environment where borrowers were managing costs aggressively, not a universal case for buying down the rate on a cash-out refinance.

For a DSCR cash-out refinance, the investor should ask: am I paying points to improve the long-term loan, or am I reducing the net cash I needed from the refinance?

If the goal is to fund another down payment, renovation, or reserve plan, points reduce the available cash. The lower payment may still be worth it, but the investor should compare net cash received, DSCR, reserves, and break-even timing before choosing that structure.

Tax Treatment of Points on Rental Property Loans

Tax treatment is one of the most misunderstood parts of discount points on rental property loans.

The IRS Publication 527 on residential rental property covers rental property income and expenses, including mortgage interest and certain expenses connected to obtaining a mortgage. IRS guidance distinguishes between deductible rental expenses and certain mortgage-related costs that may need to be treated differently.

The practical takeaway: do not assume points on a rental property create a simple year-one deduction.

How points are handled can depend on the loan purpose, whether proceeds are used for rental activity, whether the loan is refinanced, and how the cost is characterized. Investors should confirm treatment with a CPA before modeling after-tax returns.

This is especially important if the investor is comparing points with other uses of cash, such as a larger down payment, repairs, or portfolio reserves. Investors who want a broader framework can also review Ziffy’s guide to the tax implications of rental property investing.

How to Compare DSCR Loan Options With and Without Points

A good comparison should show more than the interest rate. It should show what happens to payment, DSCR, reserves, and break-even.

Item | No-point option | Buydown option |

|---|---|---|

Loan amount | $350,000 | $350,000 |

Discount points | $0 | $3,500 |

Monthly principal and interest | $2,575 | $2,445 |

Monthly taxes, insurance, and HOA | $625 | $625 |

PITIA | $3,200 | $3,070 |

Gross monthly rent | $3,850 | $3,850 |

DSCR | 1.20 | 1.25 |

Monthly payment savings | Not applicable | $130 |

Break-even period | Not applicable | 27 months |

Cash to close | Lower | Higher by $3,500 |

Reserve impact | More cash retained | Less cash retained |

In this sample, the buydown moves the property from a 1.20 DSCR to a 1.25 DSCR and saves $130 per month. If the investor expects to keep the loan for five years or more and still has enough reserves, the buydown may be worth it. If the investor expects to refinance in 18 months, the no-point option may be better.

The investor should also compare how this decision affects cash-on-cash return. A buydown can improve monthly cash flow, but it also increases upfront cash invested. Ziffy’s cash-on-cash return guide is a useful companion when points materially change the cash invested in the deal.

The 7 Questions to Ask Before Paying Points

Before paying points on a DSCR loan, narrow the decision to a few questions.

These questions are also useful when comparing DSCR against other investor financing options. If the borrower is weighing a DSCR loan against a conventional investor loan, the structure should be reviewed through rate, documentation, leverage, reserves, and property-income logic. Ziffy’s DSCR vs. conventional loan comparison can help frame that decision.

Where Ziffy Fits Into the Buydown Decision

At Ziffy, we are not here to tell every investor to buy down their rate. The better conversation is whether the loan structure fits the property and the investment plan.

In practice, that means reviewing the property’s rent support, full PITIA, DSCR, down payment, reserves, loan purpose, and likely hold period together. A rate buydown may be the right move. A larger down payment may be stronger. A no-point option may preserve the cash the investor needs for repairs or another purchase.

Investors can browse cash-flowing rentals on Ziffy, compare deal metrics, test DSCR, and move into financing with the property analysis already in view. The rate decision becomes more useful when it is tied to the deal, not separated from it.

Investment Properties on Sale Today

Final Takeaway

The best DSCR buydown decisions are made before the loan is locked, while the investor can still compare rate, cash to close, reserves, and property strength side by side.

Discount points can pay off when the investor plans to hold the rental beyond break-even, the lower payment improves PITIA and DSCR, and the investor still has enough liquidity after closing. Points are less attractive when the loan may be refinanced soon, the property has weak rental coverage, or the same cash would do more as reserves, repairs, or additional equity.

The practical test is simple: Will paying points make this rental easier to hold, easier to qualify, or more resilient after closing?

If yes, a rate buydown can be a strong long-term financing choice. If not, the investor may be better served by preserving cash, negotiating the purchase price, lowering leverage, or choosing a better rental property.

FAQs

What is a rate buydown on a DSCR loan?

A rate buydown on a DSCR loan usually means the borrower pays discount points at closing in exchange for a lower interest rate. The lower rate can reduce the monthly principal and interest payment, which may improve PITIA, DSCR, and cash flow.

How do discount points work?

One discount point equals 1% of the loan amount. On a $400,000 loan, one point costs $4,000. Points are typically paid at closing and increase upfront costs in exchange for a lower rate.

Do discount points guarantee DSCR loan approval?

No. Points can lower the payment and may improve DSCR, but they do not replace underwriting. Rent support, credit, leverage, reserves, property type, loan purpose, title, insurance, and final documentation still matter.

When do points make sense on a DSCR loan?

Points usually make sense when the investor plans to hold the loan beyond the break-even period, the lower payment improves DSCR, and the investor still has enough cash after closing.

When should investors avoid paying points?

Investors should be cautious if they expect to refinance soon, sell quickly, need more cash for reserves or repairs, or are trying to make a weak property look workable through a lower rate.

Are points better than a larger down payment?

Not always. Points lower the rate. A larger down payment lowers the loan amount, can improve LTV, and may improve DSCR. The investor should compare both options side by side before deciding.

Do points affect cash-on-cash return?

Yes. Points increase upfront cash invested. They may also improve monthly cash flow. Investors should compare both sides because a lower payment does not automatically mean a better return if the upfront cost is too high.

Are discount points tax deductible on rental property loans?

They may be deductible over time depending on the loan purpose and how the points are treated. Investors should review IRS Publication 527 and consult a CPA before assuming a year-one deduction.

Where do points appear in loan documents?

Points should appear on the Loan Estimate and Closing Disclosure. Investors should review the interest rate, annual percentage rate, or APR, monthly payment, estimated cash to close, points, lender credits, and prepayment terms before choosing a loan structure.