Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Quick answer

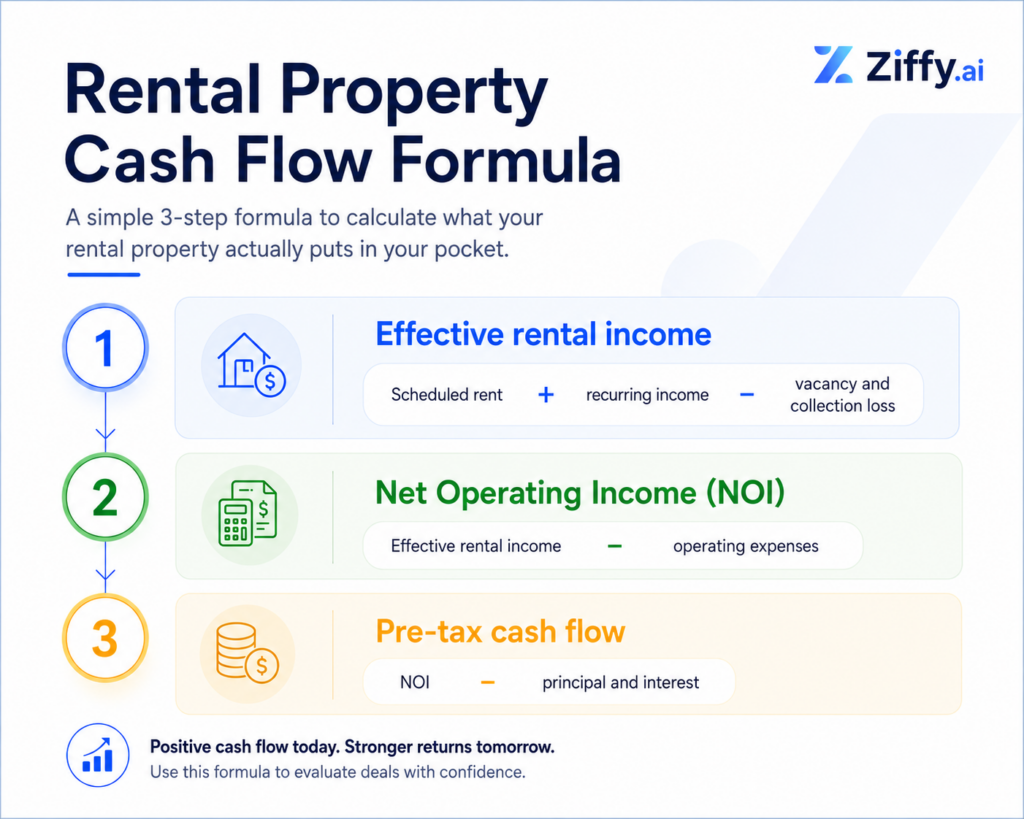

Rental property cash flow is the money left after collected rental income pays the property’s operating expenses and mortgage obligation.Monthly cash flow = effective rental income - operating expenses - debt service

A reliable calculation includes vacancy, property taxes, insurance, association dues, management, repairs, owner-paid utilities, leasing costs, and capital reserves.

The rental property calculator walks through a complete deal model. This article focuses on whether the rent, expenses, financing, and vacancy assumptions behind that result can withstand closer review.

Table of Contents

What Rental Property Cash Flow Tells You

Positive cash flow puts money into the property account. Break-even leaves almost no margin, so one repair or missed rent payment can put the owner out of pocket. Negative cash flow requires the investor to contribute money to hold the asset, which calls for a funded carrying plan before closing.

Cash flow is not the same as taxable rental income. The IRS explains rental income, expenses, and depreciation in Publication 527. Depreciation can reduce taxable rental income without reducing the cash held in the property’s operating account.

Investors should review depreciation, deductible expenses, passive-activity limitations, and other tax matters with a qualified tax professional.

Rental Property Cash Flow Formula

Principal, Interest, Taxes, Insurance, and Association dues are commonly grouped as PITIA. Fannie Mae’s Selling Guide includes these charges in the subject property’s monthly housing expense.

Watch for double-counting when taxes and insurance are escrowed. If they are listed separately as operating expenses and then included again in the full mortgage payment, the final cash flow result will understate the property’s actual performance.

How to Calculate Rental Property Cash Flow

1. Verify the rent

Use the current lease when the property is occupied. For a vacant acquisition, compare recently leased homes with similar square footage, condition, location, parking, amenities, and lease terms.

The Ziffy platform is tracking 964,477 active US residential listings, up 23.5% year over year. More inventory gives investors more properties to consider, but it also makes disciplined screening more valuable.

HUD Fair Market Rents can provide regional context. They are designed for federal housing programs, however, and should not replace property-level rental comps or appraisal-supported market rent.

Lease concessions must also be reflected in the income figure. A $2,000 monthly lease with one free month produces $22,000 during the first year. That equals an effective average of about $1,833 per month before vacancy or collection loss.

2. Account for vacancy and collection loss

The US rental vacancy rate was 7.3% in the first quarter of 2026, according to the US Census Bureau. That figure provides national context, not the correct vacancy allowance for every property.

Review local vacancy, average days to lease, turnover frequency, make-ready time, and the property’s operating history. A stable rental in a supply-constrained neighborhood may perform better than the national rate. A seasonal, high-turnover, or newly delivered property may need a larger allowance.

In our experience, optimistic rent assumptions distort more first-pass analyses than complicated formulas do.

The rent estimate has to survive the appraisal and lease review. If the supported figure comes in lower, we rebuild the payment and cash flow before treating the deal as workable.

3. Build expenses from real documents

Verify property taxes, local reassessment rules, landlord insurance, flood coverage, and association dues. Then add management, routine maintenance, owner-paid utilities, licensing, leasing fees, landscaping, pest control, and other recurring services.

Keep routine repairs separate from capital replacements. A plumbing service call is a current operating expense. A future roof, heating and cooling system, water heater, or major appliance belongs in a capital expenditure reserve.

I include a management cost even when an investor plans to self-manage. A property that only works because the owner’s time is treated as free has less room than the spreadsheet suggests.

4. Use the actual financing structure

Use the payment tied to the expected loan amount, interest rate, term, property taxes, insurance, and association dues. Principal and interest alone do not show the complete monthly housing obligation.

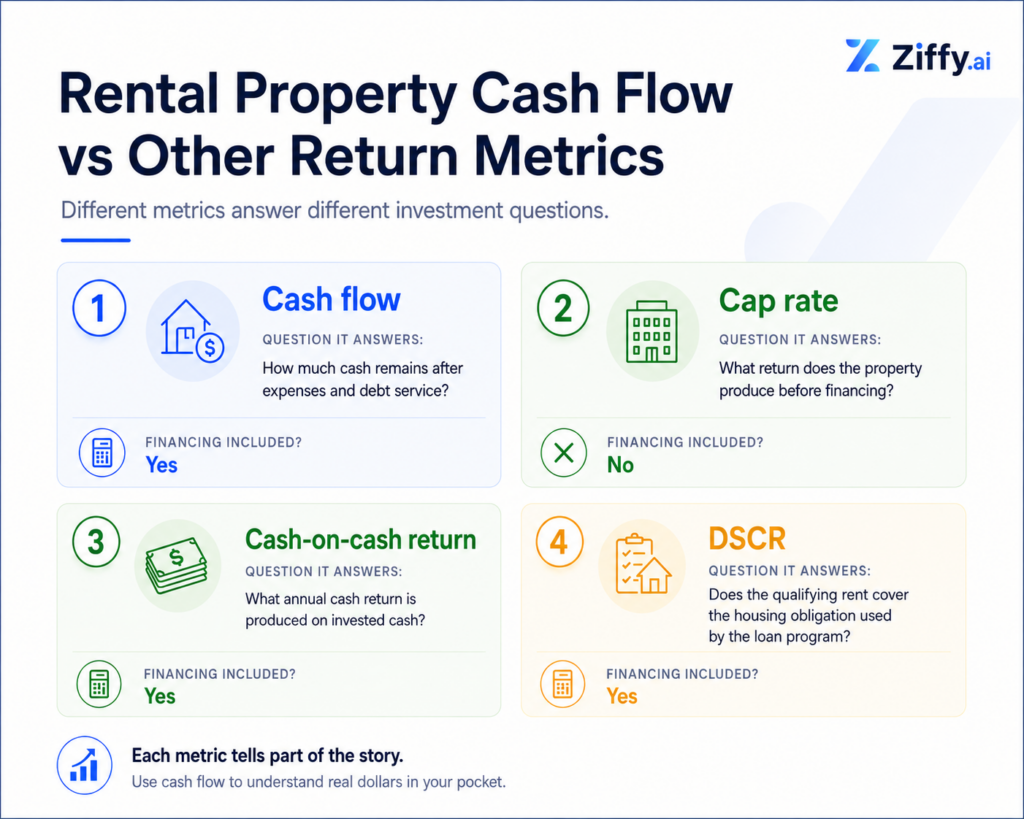

With a Debt Service Coverage Ratio (DSCR) loan, qualification is based mainly on rental income rather than W-2 income, pay stubs, or personal tax returns. DSCR compares the qualifying rent with PITIA.

Full cash flow analysis goes further by including expenses outside PITIA, such as management, repairs, owner-paid utilities, leasing costs, vacancy, and replacement reserves.

Loan availability and terms vary by state, borrower profile, property, leverage, credit, reserves, and loan purpose.

5. Annualize and stress test the result

Multiply a representative monthly cash flow result by 12 to estimate annual cash flow. For an operating property, a trailing 12-month statement is more useful because it captures actual vacancy, repairs, turnover, concessions, and collection patterns.

At Ziffy, we rerun the deal with verified taxes, an insurance quote, a vacancy allowance, and replacement reserves. A positive first-pass result tells us the property deserves a closer look. It does not complete the analysis.

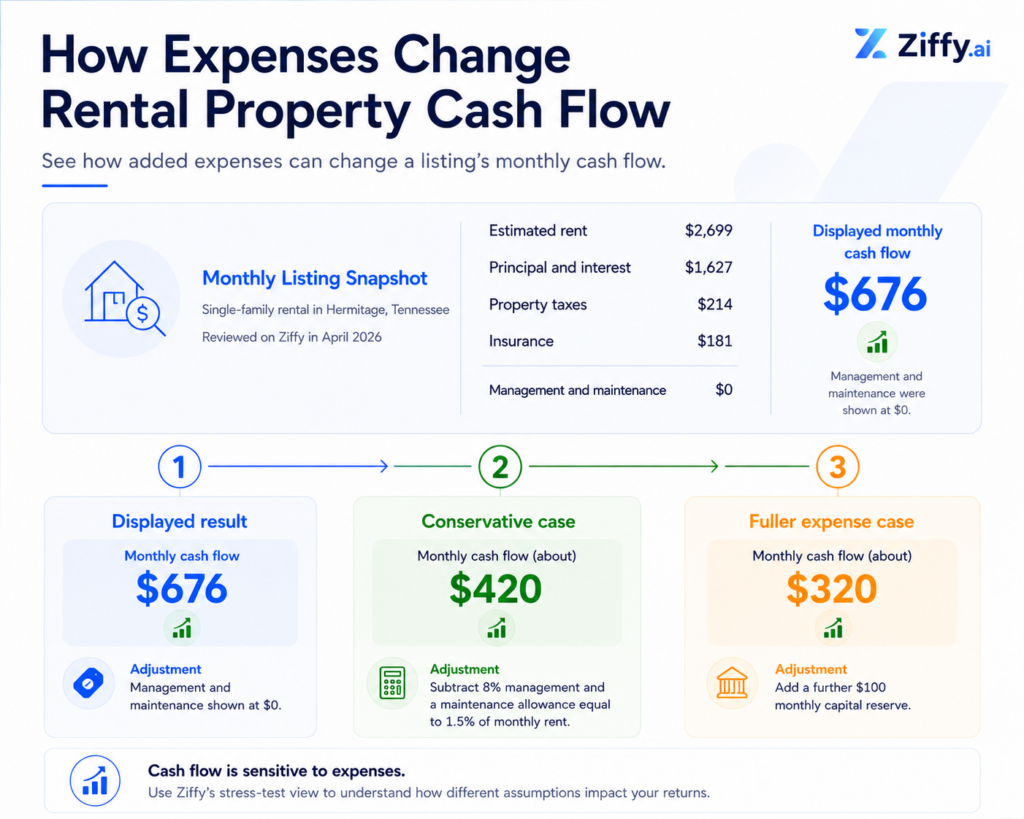

A Ziffy Cash Flow Example

A single-family rental listing in Hermitage, Tennessee, reviewed on Ziffy in April 2026 showed the following estimated figures:

Item | Monthly amount |

|---|---|

Estimated rent | $2,699 |

Principal and interest | $1,627 |

Property taxes | $214 |

Insurance | $181 |

Displayed monthly cash flow | $676 |

Management and maintenance were shown at $0; result will change if we add those expenses.

Scenario | Monthly cash flow | Adjustment |

|---|---|---|

Displayed result | $676 | Management and maintenance shown at $0 |

Conservative case | About $420 | Subtract 8% management and a maintenance allowance equal to 1.5% of monthly rent |

Fuller expense case | About $320 | Add a further $100 monthly capital reserve |

One month without rent would remove $2,699 from annual income before cleaning, repairs, advertising, leasing fees, or other turnover costs.

A pattern we see often is that the initial result looks healthy, but the decision changes once omitted operating expenses are added. In this example, the property remains positive under the fuller expense case, but its margin falls by more than half.

Investment Properties on Sale Today

What is a Good Monthly Cash Flow?

No single monthly target works across every market, purchase price, or property condition. The more useful question is how much financial pressure the margin can absorb.

For an income-focused purchase, cash flow should remain positive after vacancy, management, maintenance, and capital reserves. One practical test is whether annual cash flow could absorb a month without rent. That is an investor sanity check, not a lending requirement.

The amount of capital used to create that cash flow also matters. A larger down payment can improve monthly cash flow while weakening cash-on-cash return if the payment reduction is small relative to the additional equity invested.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

The ratio is only one part of the file. Rent support, leverage, reserves, and cash left after closing determine whether the property has a durable cushion or a narrow approval margin.

How to Improve Rental Property Cash Flow

Negotiate the purchase price

Cash flow problems often begin with the acquisition price. If verified rent cannot support the operating expenses and financing, a lower offer will usually improve the deal more effectively than an optimistic rent-growth assumption.

Raise income with market support

In-unit laundry, usable parking, permitted storage, and properly structured pet fees can raise rent in some submarkets. Review comparable leases before paying for an upgrade. An improvement has not strengthened cash flow until tenants in that market are willing to pay for it.

Reduce avoidable costs

Review insurance before renewal, examine the tax assessment, compare management agreements, and correct water or energy waste. Do not postpone essential maintenance to improve a spreadsheet. Deferred repairs can create larger bills and longer vacancies later.

Rework the financing

Interest rate, leverage, loan term, points, and down payment all affect the monthly obligation. Use Ziffy’s DSCR loan calculator to test how a different structure changes PITIA and rental coverage.

Protect occupancy

Accurate pricing, quick turnovers, responsive maintenance, and early renewal discussions can preserve more income than a small rent increase. Track why tenants leave so the response addresses the actual problem.

Pro Tips From the Loan Desk

- Budget turnover separately from routine maintenance: Cleaning, paint, repairs, leasing costs, and lost rent can arrive during the same vacancy. Combining them under a small general maintenance percentage can understate the cost of replacing a tenant.

- Confirm the post-purchase tax bill: Dorian recommends checking local reassessment rules before finalizing the cash flow model. The seller’s current tax bill may not reflect the expense after the property transfers.

- Separate loan qualification from property performance: A property can meet the minimum DSCR requirement and still produce weak cash flow after management, repairs, utilities, vacancy, and reserves are included.

- Price a refinance against the full cost: Compare the expected payment reduction with discount points, lender charges, title costs, and the remaining holding period. A lower monthly payment does not automatically make a refinance economical.

Common Cash Flow Analysis Mistakes

1. Using asking rent as collected rent

Online estimates, seller projections, and advertised rents are screening tools. The current lease, comparable rentals, and appraisal-supported market rent carry more weight.

2. Leaving management at zero

Self-management does not make the economic cost disappear. A market-rate management line shows whether the property remains workable if the owner’s time or circumstances change.

3. Ignoring the post-purchase tax bill

A reassessment can erase a thin cash flow margin. What we see often is an analysis built around the seller’s historical bill even though the purchase price may reset the taxable value.

4. Treating capital replacements as surprises

Roofs, mechanical systems, flooring, and appliances wear out. A capital reserve turns an inevitable cost into a planned monthly expense rather than an emergency cash request.

5. Comparing rent only with principal and interest

This shortcut leaves out property taxes, insurance, and association dues. DSCR uses PITIA, while a complete cash flow analysis also includes the operating expenses that sit outside PITIA.

Cash Flow Compared With Other Return Metrics

Cap rate leaves the mortgage out of the calculation. Cash flow does not show whether the monthly surplus provides a strong return on the total cash invested. Review the metrics together before making an offer.

Should You Buy a Negative Cash Flow Rental?

A negative result can be intentional when the investor has a funded renovation, lease-up, or long-term appreciation plan and enough liquidity to carry the property.

It becomes difficult to sustain when the plan depends on rent growth the market does not currently support or appreciation that has not occurred.

Calculate the expected shortfall across the intended holding period, then add vacancy, repairs, insurance changes, and financing costs. Keep post-closing reserves outside the acquisition budget.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

Some markets are better long-term holds than immediate income plays. The strategy only works when the investor has modeled the shortfall, protected reserves, and set a realistic carrying period.

Where DSCR Financing Fits

When rental income qualifies the loan in place of W-2s, pay stubs, or personal tax returns, DSCR is usually the best-fit financing structure.

Ziffy Mortgage also reviews credit, leverage, reserves, property use, rent support, and ownership structure. Review current DSCR loan requirements before finalizing the financing assumptions in the cash flow model.

Ziffy’s AI-native real estate investing experience helps investors find cash-flowing properties, review returns, and move into financing with the deal economics already in view.

Analyze the Property Before Requesting the Loan

Use Ziffy’s cash flow calculator to replace listing assumptions with your financing and operating costs. Once the result still works with verified expenses and a realistic stress case, request a DSCR rate quote based on the structure you intend to close.

FAQs

What expenses belong in rental property cash flow?

Include vacancy, property taxes, insurance, association dues, management, maintenance, owner-paid utilities, leasing costs, and capital reserves. Then subtract principal and interest without counting escrowed taxes or insurance twice.

What is the difference between cash flow and NOI?

NOI measures the property’s income after operating expenses but before mortgage principal and interest. Cash flow also subtracts debt service.

Is rental property cash flow calculated before or after the mortgage?

Investor cash flow is generally calculated after debt service whereas NOI is calculated before financing.

Does depreciation increase rental property cash flow?

No. Depreciation may reduce taxable rental income, but it does not add cash to the property’s operating account.

Can a property have a good DSCR and weak cash flow?

Yes. DSCR may exclude management, maintenance, owner-paid utilities, leasing costs, vacancy, and capital reserves included in a complete cash flow analysis.

How often should rental property cash flow be recalculated?

Recalculate it before making an offer, after receiving final tax and insurance figures, whenever the financing changes, and at least annually after closing.