Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

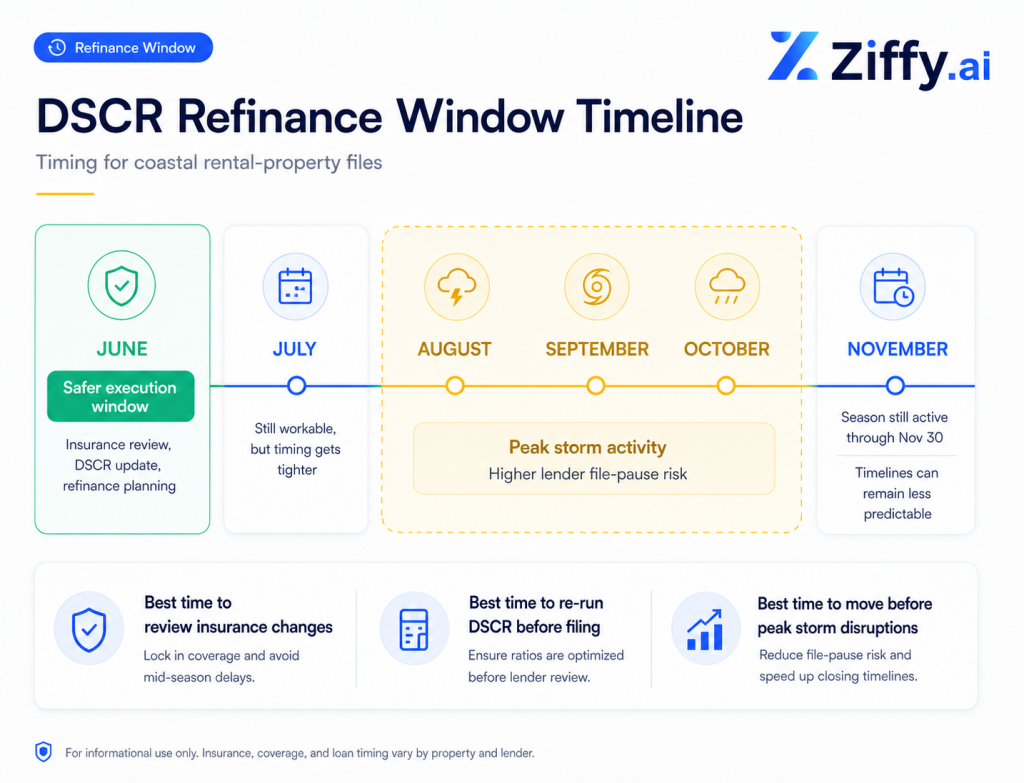

NOAA’s 2026 Atlantic hurricane outlook gives the season a 55% chance of below-normal activity, but the agency still forecasts 8 to 14 named storms, 3 to 6 hurricanes, and 1 to 3 major hurricanes. Rental owners should use June to review insurance coverage, flood-policy timing, wind mitigation paperwork, tenant communication, and the DSCR (debt service coverage ratio) impact of any insurance increase, since insurance is part of PITIA, which includes principal, interest, taxes, insurance, and association dues.

The 2026 Atlantic hurricane season opened on June 1 with a calmer outlook than many coastal investors have seen in recent years. NOAA expects most of this year’s activity to occur during August, September, and October, which leaves June as the practical review window for rental owners who still need to clean up insurance, documentation, and refinance timing before the season becomes harder to manage.

Hurricane Ian is still the example many Florida investors remember. NOAA’s National Centers for Environmental Information ranks Ian as the third-costliest US hurricane on record, with $119.6 billion in CPI-adjusted total costs, a figure that includes insured and uninsured losses.

For rental owners in Florida, Texas, Georgia, Louisiana, South Carolina, North Carolina, and other storm-exposed markets, the work is not limited to physical prep. A landlord policy can carry the wrong deductible, a flood policy may not be active yet, and a higher insurance premium may already have changed the property’s DSCR. That does not affect every owner the same way, but it matters for anyone considering a refinance, cash-out, or another rental purchase this year.

Table of Contents

1. Read the declarations page, not just the renewal notice

Start with the full declarations page for the rental property. The renewal notice confirms the policy exists. The declarations page shows the coverage that will matter after a storm.

Begin with dwelling coverage. The amount should reflect the cost to rebuild the property, not the price you paid for it or the current market value. A rental purchased several years ago can be underinsured if the policy has not kept up with construction costs, labor costs, and local rebuilding conditions.

Next, review the deductible structure. Coastal policies often separate standard deductibles from windstorm, hurricane, or named-storm deductibles. Those storm deductibles may be written as a percentage of dwelling coverage instead of a flat dollar amount.

- For example, if a property is insured for $400,000 and the hurricane deductible is 2%, the owner would pay $8,000 before coverage begins. That example is only meant to show how the deductible works. The actual amount depends on the policy.

Loss-of-rents coverage deserves the same review. If the property becomes uninhabitable after covered damage, this is the part of the landlord policy that can help protect rental income while repairs are underway. Look at the coverage amount, the duration, and the conditions that apply before assuming the rent stream is protected.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

The files that worry me are not always the highest-loan-amount files. They are often the ones where the investor has not opened the declarations page in a year. The premium changed, the deductible changed, or the rent-loss coverage is thinner than they assumed. By the time they find out, they are already trying to refinance or respond to a claim.

2. Confirm flood coverage before the waiting period cuts into the season

FEMA’s National Flood Insurance Program states that most homeowners and renters insurance policies do not cover flood damage, and NFIP coverage generally takes effect 30 days after purchase unless one of the listed exceptions applies.

A flood policy purchased after a storm threat is already visible may not be active in time. Ask your insurance professional these questions before the season gets busier:

- Is flood insurance active on the property?

- What is the building coverage limit?

- Is contents coverage included for owner-owned appliances, furnishings, or equipment?

- When does the policy become effective?

- Does the coverage match the property’s actual use?

That last question is especially relevant for short-term rentals. A furnished vacation rental, a long-term rental, and an owner-used second home can create different insurance conversations. The safer move is to confirm the use directly with the carrier or insurance professional instead of assuming the policy fits because the premium was accepted.

For a broader breakdown of what a landlord policy covers, what flood insurance handles separately, and where rental owners often misunderstand coverage, see our Investment Property Insurance guide.

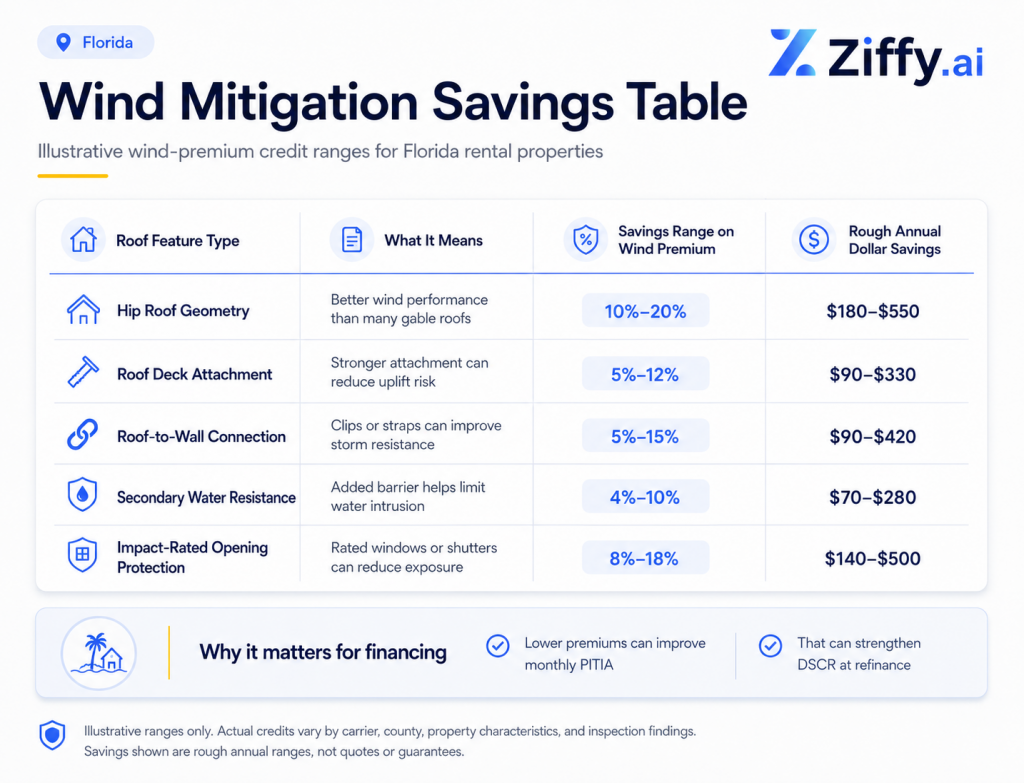

3. For Florida rentals, review the wind mitigation form

Florida rental owners should check whether their wind mitigation inspection is current. The state’s Uniform Mitigation Verification Inspection Form, OIR-B1-1802, is valid for up to five years as long as no material changes have been made to the structure and no inaccuracies are found on the form.

If the roof has been replaced, impact windows were added, opening protection changed, or other major work was completed since the last inspection, ask whether a new inspection should be ordered before renewal.

The form documents roof covering, roof deck attachment, roof-to-wall connection, roof geometry, secondary water resistance, and opening protection. Those details can affect how the carrier evaluates wind risk.

For a rental owner using DSCR financing, any legitimate insurance reduction can also help the loan file. A lower premium reduces the insurance portion of PITIA, which can improve the ratio used at refinance or on the next purchase.

4. Walk the property while there is still time to fix small issues

A June property walk should focus on the problems that become expensive after heavy wind or rain. Start with the roofline, gutters, drainage, trees, exterior structures, shutters, windows, doors, fencing, and any rooftop or exterior HVAC equipment.

Look for loose branches near the structure, clogged gutters, pooling water, damaged flashing, weak fence panels, unsecured outdoor items, and shutters that do not close properly. If the property has a tenant, do not assume they know how to use storm shutters or where utility shutoffs are located.

Document the condition of the property while everything is still intact. Take photos and video of the roofline, exterior walls, windows, doors, ceilings, floors, appliances, electrical panel, HVAC equipment, garage, fencing, and any furnished areas. Store the file somewhere other than your phone.

That record can help if there is a later claim, especially when the carrier needs to separate pre-existing wear from storm-related damage.

5. Send tenants a short hurricane-season notice

Keep the tenant notice short and practical. Before June 30, send one message that covers emergency contact information, how to report damage, where the utility shutoffs are located, what to do with loose outdoor items, how to use shutters if the property has them, and where tenants can find local evacuation guidance.

Review the lease at the same time. Confirm emergency access language, maintenance reporting requirements, and any renters insurance requirement. A landlord policy does not cover the tenant’s personal belongings. If the tenant assumes your policy covers their furniture, electronics, clothing, or temporary housing, correct that before a storm turns the misunderstanding into a claims dispute.

For short-term rentals, add the same information to the guest guide. Guests may not know the local evacuation zone, local alert system, or how quickly travel becomes limited once warnings are issued.

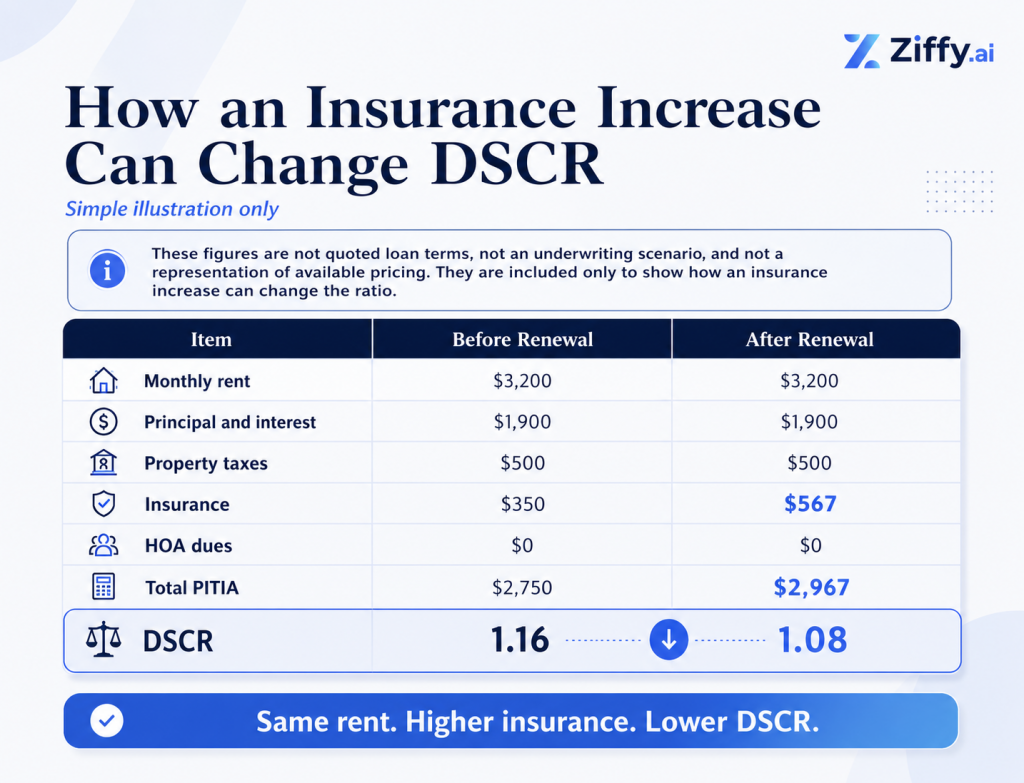

6. Re-run the DSCR calculation with the current insurance premium

Insurance belongs in the loan math, not just the insurance folder.

A DSCR loan compares the property’s rental income with the monthly housing expense. For rental-property financing, that housing expense typically includes principal, interest, taxes, insurance, and association dues. If the insurance premium changed at renewal, the monthly expense changed with it.

Use the current annual premium, divide it by 12, and update the property’s monthly housing expense before reviewing refinance or cash-out options.

When rent and the mortgage payment stay flat but the annual insurance premium increases, the DSCR can still fall. That is why the monthly insurance figure needs to be current before any refinance, cash-out, or next-purchase conversation.

That may not create an immediate problem for an owner who plans to hold the property without touching the debt. It can become a problem if the owner wants to refinance, pull cash out, or use the property’s performance to support the next acquisition.

At Ziffy, this is the review investors should complete before peak storm months. A lower DSCR does not automatically mean the file is dead, but it can change leverage, reserves, pricing, or the structure that makes the most sense.

Use the Ziffy DSCR Calculator with the current insurance premium before starting a refinance conversation.

Investment Property on Sale Today

7. Decide on refinance timing before peak storm months

Coastal rental refinances can close during hurricane season, but the process leaves less room for surprises once storms are active.

If a named storm is tracking toward the subject property, a lender may need to wait for the storm to clear, confirm property condition, review insurance again, or request updated documentation before closing. If that delay runs into the rate-lock deadline, the investor may be dealing with an extension fee or a new lock.

June gives a coastal refinance file more breathing room. The insurance policy can be reviewed before there is urgency. The DSCR can be recalculated with the current premium. If the property needs a condition check, documentation update, or insurance correction, the borrower still has time to handle it before the busiest part of the season.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

A June refinance review gives everyone more room. If the property works, we can move before peak storm season. If the insurance number changed the DSCR, we still have time to talk through structure, reserves, and whether the loan makes sense now or later.

Run the updated DSCR first, then check whether the file still meets DSCR loan requirements and whether the borrower’s reserve position is strong enough under Ziffy’s cash reserves for investment loans guidance.

Hurricane Prep Checklist for Rental Property Owners

Finish these items before June 30:

- Review the full insurance declarations page.

- Confirm dwelling coverage, wind deductible, named-storm deductible, and loss-of-rents coverage.

- Check whether flood insurance is active.

- Confirm the flood policy effective date.

- For Florida rentals, review the OIR-B1-1802 wind mitigation form.

- Walk the roof, gutters, trees, shutters, fencing, drainage, and HVAC equipment.

- Take a full photo and video inventory.

- Send tenants a hurricane-season notice.

- Confirm renters insurance requirements if the lease includes them.

- Recalculate DSCR with the current insurance premium.

- Decide whether a refinance or cash-out review should happen before peak storm months.

Next Steps

If you own a coastal rental property, pull the insurance file before the season gets busier. Review flood coverage, check the wind mitigation form if the property is in Florida, document the property’s condition, and run the DSCR again with the current premium.

If the ratio is lower than expected, or if a refinance is already on the table, Ziffy can review the file before peak storm months make timing harder.

FAQs

When does hurricane season start?

The Atlantic hurricane season runs from June 1 through November 30. NOAA’s 2026 outlook covers that full season window and says most activity is likely during August, September, and October.

What is NOAA forecasting for the 2026 Atlantic hurricane season?

NOAA’s 2026 outlook gives the Atlantic a 55% chance of a below-normal season, a 35% chance of a near-normal season, and a 10% chance of an above-normal season. The agency forecasts 8 to 14 named storms, 3 to 6 hurricanes, and 1 to 3 major hurricanes.

Does a standard landlord policy cover flood damage?

Usually no. FEMA’s NFIP guidance says most homeowners and renters insurance policies do not cover flood damage. Rental property owners should review flood coverage separately with a licensed insurance professional.

Is there a waiting period for flood insurance?

In most cases, yes. NFIP flood insurance coverage generally goes into effect 30 days after purchase, with limited exceptions.

How long is a Florida wind mitigation form valid?

Florida’s OIR-B1-1802 wind mitigation form is valid for up to five years as long as no material changes have been made to the structure and no inaccuracies are found on the form.

Why does insurance affect DSCR?

Insurance is part of the monthly housing expense used in the DSCR calculation. If the annual premium rises and rent does not rise with it, the ratio falls. That can affect refinance proceeds, cash-out eligibility, reserves, pricing, or the loan structure available to the investor.