Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

An investor buys a single-family rental, keeps the homeowners policy the seller had, places a tenant, and assumes the property is covered. Months later, a kitchen fire damages the home. The claim reaches the carrier, the lease comes up during the review, and the carrier denies the claim because the property was being used as a rental.

The investor had insurance, but not the kind a rental property needed.

Investment property insurance protects a rental differently than a standard homeowners policy. It has to account for tenant occupancy, rental income, landlord liability, lender requirements, and location-specific risks such as flood, wind, wildfire, or hail. It also affects financing because insurance is part of PITIA, which stands for principal, interest, taxes, insurance, and association dues. On a debt service coverage ratio loan, usually called a DSCR loan, a higher insurance premium can reduce the property’s qualifying ratio and change how the file is priced, structured, or approved.

For Ziffy Mortgage, insurance is part of the lending review because it sits inside the monthly payment used to qualify the property. A rental can look strong when the analysis uses a rough premium estimate, then become much tighter once the actual quote arrives. That is why investors should not treat insurance as a final-week closing task.

On Ziffy, investors can review rent, projected expenses, PITIA, DSCR, and cash flow before moving too far into a deal. That early view helps separate rentals that work on price and rent alone from rentals that still work after insurance, taxes, reserves, and financing costs are included.

Before making an offer, run the property through the DSCR loan calculator and cash flow calculator, then confirm the insurance quote with a licensed agent.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

Insurance is one of the fastest ways a rental file can change late in the process. A property can look strong with a placeholder premium, then become much tighter once the actual binder arrives. Investors should treat insurance as part of the offer analysis, not something to solve three days before closing.

Why Standard Homeowners Insurance Does Not Cover Rental Properties

A standard homeowners policy is built around owner occupancy. It assumes the person who owns the property lives there, maintains the home, controls daily access, and uses the property as a residence rather than as an income-producing rental.

A tenant-occupied property changes that risk profile. The owner is not living there. Rent is being collected. The carrier is taking on a different liability and property exposure than it priced into an owner-occupied policy. That is where investors can get into trouble if they keep the seller’s homeowners policy or ask for a quote that still assumes owner occupancy.

The Wisconsin Office of the Commissioner of Insurance says that if an owner plans to rent out a home long term or frequently rent out part or all of the home, landlord property insurance or rental coverage may be the better fit. The same guidance says landlord insurance can cover the home, structures, landlord-owned contents, lost rental income due to building damage, legal defense costs, and liability protection.

In a claim, the carrier will usually ask who occupied the property, whether rent was being collected, whether a lease was in place, and whether the policy was written for the correct occupancy. If the home was insured as owner-occupied but was actually tenant-occupied, the carrier may argue that the claim falls outside the policy’s intended use.

Some investors assume a rider will fix the problem. An endorsement can help in certain limited situations, especially when rental use is occasional. It does not automatically solve long-term rental use, short-term rental activity, or a full investment property conversion. Wisconsin insurance guidance also warns that business use can affect liability or property coverage under a homeowners policy.

Once a property will be rented, quote it as a rental. Do not rely on the seller’s homeowners premium, a national estimate, or a quote that assumes owner occupancy.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

What we see often is investors keeping the seller’s homeowners policy through closing because the carrier has not caught the change in occupancy yet. The coverage may still look active, but the next claim is where the problem shows up. Quote the property as a rental from day one, even if closing is only two weeks away.

The 4 Policy Types Every Investor Needs to Know

Investment property insurance is often discussed as “landlord insurance,” but that phrase can hide important differences. Investors should understand the policy form, settlement basis, liability protection, and exclusions before closing.

DP-1: Basic Form

A DP-1 policy is the most limited dwelling policy in this group. It generally covers only named perils listed in the policy, such as fire, lightning, and windstorm. The National Association of Insurance Commissioners defines DP-1 as a basic form that covers the dwelling structure and attached structures against specific named perils.

DP-1 can be cheaper, but the narrower coverage often makes it the wrong starting point for a tenant-occupied rental. Claim settlement may also be based on actual cash value, meaning depreciation can reduce the payout.

A DP-1 may make sense for a vacant or land-banked property where the investor understands the limited coverage. It is rarely the right starting point for a stabilized rental that is expected to support DSCR financing.

DP-2: Broad Form

A DP-2 policy is still a named-peril policy, but it covers more perils than DP-1. NAIC describes DP-2 as covering the perils included in DP-1 plus additional named perils such as falling objects, weight of snow, and vandalism.

DP-2 is a middle option. It can work for certain rentals if replacement cost coverage is available and the lender accepts the form. In practice, many investors skip over DP-2 because the cost difference between DP-2 and stronger coverage may not be large enough to justify the added claim risk.

DP-3: Special Form

A DP-3 policy is the form most long-term rental investors should understand first. NAIC describes DP-3 as providing open-perils coverage for the dwelling and attached structures, except for exclusions specifically listed in the policy, such as flood or earthquake.

That open-perils structure is why DP-3 is common for occupied long-term rentals. Instead of depending only on a list of named covered perils, the policy generally starts from broader coverage and then applies exclusions. The policy language still matters, but DP-3 is usually a cleaner fit for a tenant-occupied single-family rental than DP-1 or DP-2.

Most DSCR lenders want a policy that adequately protects the dwelling, names the lender correctly, covers the right occupancy, and provides acceptable replacement coverage. A DP-3 or equivalent landlord policy is often the cleanest path.

Landlord Policy

A landlord policy is usually built around dwelling protection, but it may also include liability coverage, loss of rents, and protection for landlord-owned items such as appliances. For many buy-and-hold investors, a landlord policy with strong dwelling coverage, liability, and loss of rents is more practical than trying to assemble coverage piece by piece.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

The policy label matters less than the actual coverage behind it. We see investors under-insure properties because they use purchase price as the coverage target. Rebuild cost is a different number. If the structure is badly damaged and the replacement coverage is short, the loan may be protected better than the investor’s equity.

When investors compare properties on Ziffy, insurance belongs in the same analysis as rent, taxes, debt service, reserves, and projected cash flow. A low premium estimate is not useful if it does not match the actual property use.

What Landlord Insurance Actually Covers

A landlord policy protects the owner’s interest in an income-producing property. Coverage varies by carrier and state, but most policies are built around three areas: property, liability, and rental income protection.

Property Coverage

Property coverage protects the dwelling structure. Depending on the policy, it may also cover detached structures such as garages, sheds, fences, or other improvements.

The dwelling limit should be based on the cost to rebuild the structure, not the purchase price or the outstanding loan balance. In some markets, the purchase price includes land value that does not need to be insured. In other markets, especially older housing stock or high-construction-cost areas, the rebuild cost can exceed what the investor paid.

Tenant belongings are not covered by the landlord’s property coverage. Tenants need renters insurance for their own personal property and liability. The South Carolina Department of Insurance explains that renters insurance does not cover the building or structure, which is usually the landlord’s responsibility.

Flood and earthquake are usually excluded from standard property policies. CFPB guidance says flood insurance is typically separate from standard homeowners insurance, and properties in Special Flood Hazard Areas generally require flood insurance when financed with a mortgage.

Liability Coverage

Liability coverage protects the landlord if someone claims they were injured because of the property or the landlord’s negligence. A tenant slips on an unrepaired step. A guest is injured by a loose handrail. A delivery person falls on an icy walkway. These are the kinds of claims landlord liability coverage is meant to address.

Many investors still think of $300,000 as a normal liability limit because that figure was common years ago. For rental owners, $1 million is a more realistic baseline to discuss with an insurance agent. Investors with multiple rentals, higher net worth, short-term rentals, pools, older buildings, or higher-risk features should also ask about umbrella coverage.

Dog bites are another area to review carefully. Some policies exclude certain breeds or animal liability altogether. Do not assume coverage exists just because the policy has a liability section.

Lucas Hernandez

Mortgage Loan Originator

Ziffy Mortgage

NMLS #2171747When clients ask me how much liability coverage to carry, I tell them to think about portfolio size, not just this one property. A single $1 million policy is a starting point. Once you have three or more rentals, an umbrella policy is usually cleaner than trying to raise each underlying limit separately.

Loss of Rents or Fair Rental Value

Loss of rents is one of the most overlooked coverages in investment property insurance. It may also be called fair rental value or rental income protection.

This coverage can reimburse lost rental income if the property becomes uninhabitable because of a covered loss. For investors, that is direct cash flow protection. Without loss of rents coverage, a fire, storm, or major covered loss can create two problems at once: repair costs and no rent.

Loss of rents coverage does not pay for every vacancy. It generally applies when a covered loss makes the property uninhabitable. Investors should confirm the covered period, waiting period, documentation requirements, and whether the policy pays based on actual lease income or market rent.

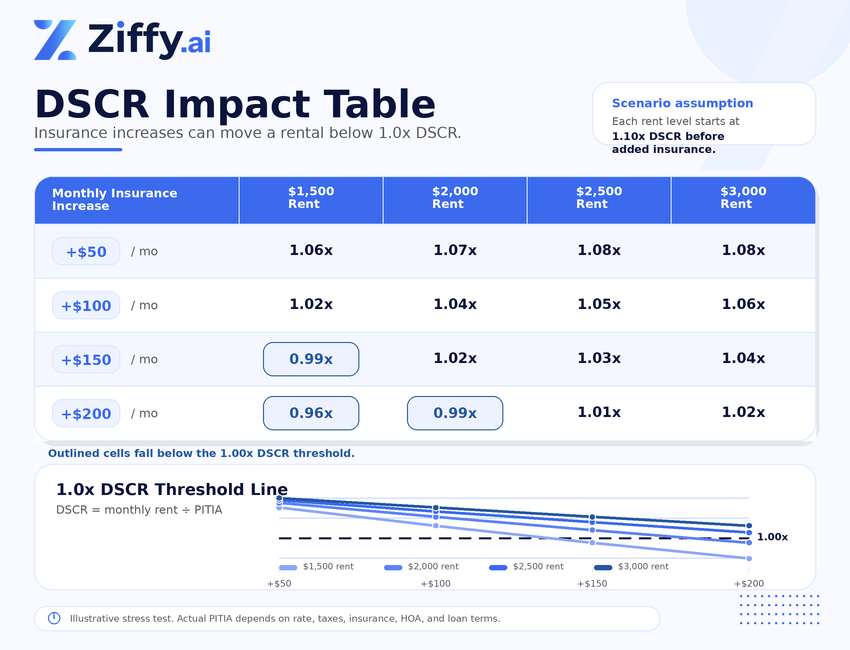

How Insurance Costs Affect Your DSCR and Loan Qualification

Insurance is part of PITIA, which stands for principal, interest, taxes, insurance, and association dues. On a DSCR loan, the lender compares the property’s qualifying rental income with the monthly housing expense.

The formula is:

DSCR = Gross Monthly Rent ÷ PITIA

A property with $1,800 in monthly rent and $1,400 in PITIA has a DSCR of 1.29. If the PITIA is only $1,200 because insurance is lower, the DSCR rises to 1.50. The rent is identical in both scenarios, but the insurance number changes the qualifying profile.

Ziffy Mortgage generally prefers a 1.0 DSCR or higher, with program variants available for files that fall below that level. Current DSCR program terms include purchase financing up to 80% loan-to-value, cash-out refinance up to 75% loan-to-value, a $100,000 minimum loan size, a 620 minimum credit score, and two months of reserves on many files, subject to underwriting and program eligibility. Investors can review the full financing framework in our guide to DSCR loan requirements.

Item | Lower Insurance Scenario | Higher Insurance Scenario |

|---|---|---|

Monthly rent | $1,800 | $1,800 |

Principal and interest | $1,000 | $1,000 |

Taxes | $200 | $200 |

Insurance | $100 | $300 |

Association dues | $0 | $0 |

Total PITIA | $1,300 | $1,500 |

DSCR | 1.38 | 1.20 |

Both scenarios may still qualify, but the higher insurance premium reduces the margin. On a tighter property, the same increase could lead to pricing changes, lower leverage, additional reserves, or a different program structure.

Insurance can also affect cash needed at closing, especially if the file requires stronger reserves or escrow deposits. See how much cash you actually need before closing a rental loan.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

At the pre-qualification stage, the file that creates problems later is the one using placeholder insurance. We tell investors to get an actual quote from a licensed insurance agent before submitting the full loan package. A real quote prevents the mid-process DSCR surprise that can slow down closing.

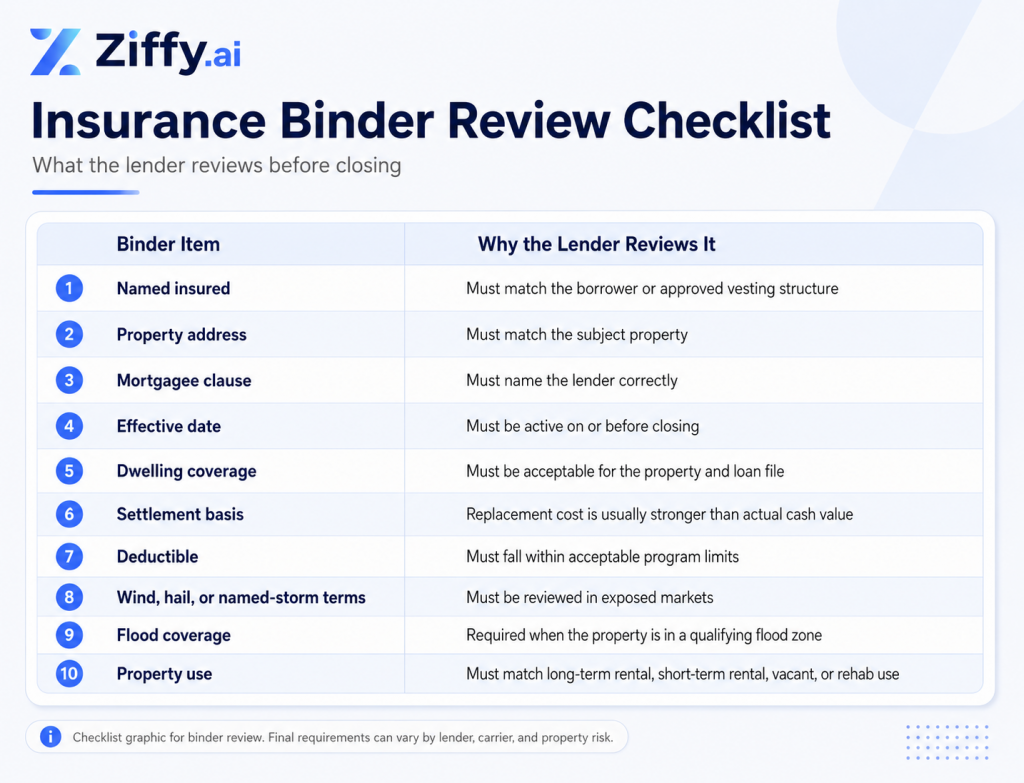

How Lenders Actually Treat Your Insurance Binder

A lender is reviewing more than proof that a policy exists. The binder has to match the loan file closely enough for underwriting to clear it before closing.

Actual cash value and replacement cost can lead to very different claim outcomes. The California Department of Insurance explains that replacement cost is the amount needed to replace damaged property with new property of similar kind and quality without deducting for depreciation, while actual cash value reflects current market value after depreciation.

That difference can affect the investor’s real loss after a claim. It can also affect lender comfort with the collateral. If a policy has actual cash value roof settlement, a high wind deductible, excluded rental use, or a mismatch between the insured party and borrower, the file can stall even when the investor has technically purchased insurance.

When we review the binder, we are looking for alignment. The insured name, property address, property use, mortgagee clause, coverage amount, deductible, and effective date all need to match the file. One small mismatch can delay the closing disclosure or force the investor back to the agent for a revised binder.

Insurance Costs by Property Type and Market

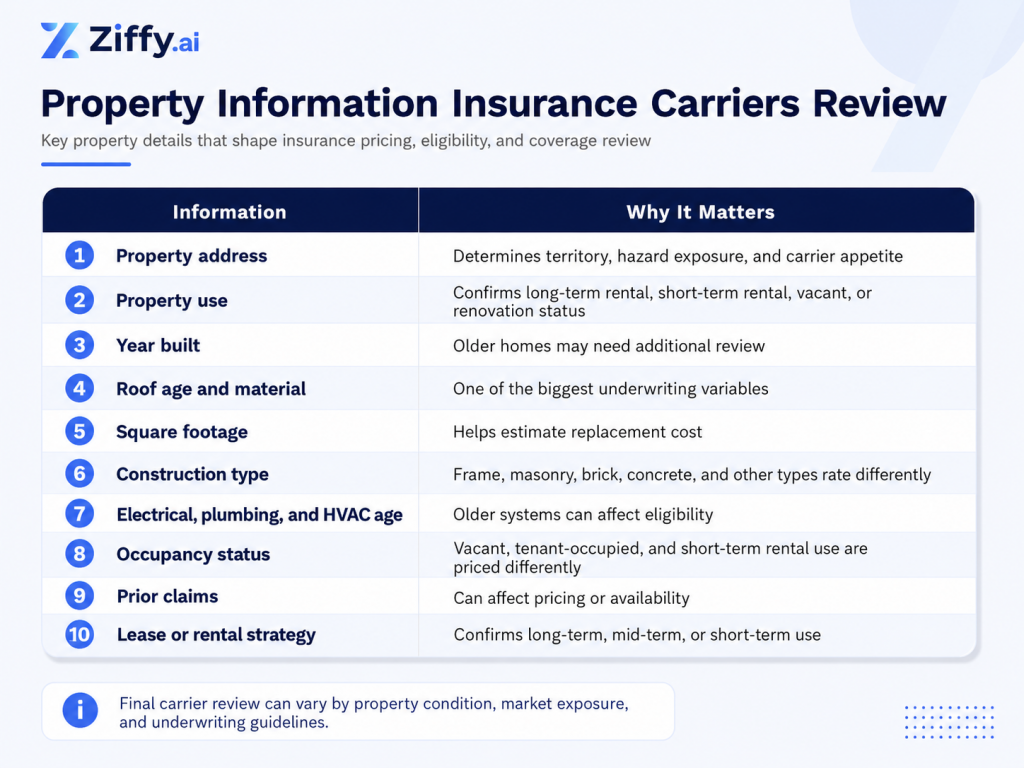

Insurance costs vary widely by property type, age, construction, roof condition, claim history, replacement cost, occupancy, and location. The same investor may see a manageable premium on an inland Midwest rental and a much higher premium on a coastal property with wind exposure.

Single-Family Long-Term Rentals

Single-family long-term rentals are usually the simplest investment properties to insure when they are occupied, in good condition, and outside high-risk zones. A clean DP-3 or landlord policy is commonly available for stabilized rentals.

For planning purposes, investors often see annual landlord insurance quotes in the low four figures for lower-risk single-family rentals. The number can move quickly once the property has an older roof, prior claims, coastal exposure, wildfire risk, older electrical systems, or higher rebuild cost.

A lower purchase price does not guarantee lower insurance. A $140,000 rental with old plumbing, old wiring, and deferred maintenance can be harder to insure than a newer $300,000 rental in a lower-risk market.

Short-Term Rentals

Short-term rentals need extra care. A standard DP-3 or long-term landlord policy may not cover nightly or weekly guest use. Platform coverage is also not a replacement for a dedicated short-term rental policy.

A property used for short-term rentals has a different risk profile from a long-term rental. There are more guests, more turnover, more access points, and often a different liability exposure. Investors should tell the insurance agent exactly how the property will be used, including direct bookings, Airbnb, Vrbo, mid-term stays, or mixed rental use.

Airbnb’s AirCover for Hosts includes host liability insurance and host damage protection, but Airbnb states that host damage protection has terms, conditions, and exclusions and is not an insurance policy. Vrbo’s liability insurance applies to reservations processed through Vrbo checkout, and Vrbo states that bookings processed or paid outside Vrbo checkout are not covered by that program. Direct bookings, off-platform stays, and mid-term leases need their own insurance review.

A lot of short-term rental investors assume platform coverage replaces a dedicated policy. It does not. Underwriting wants to see a policy that names short-term rental use specifically. Otherwise, the file can stall while we sort out the right binder.

Investors considering short-term rentals can also review Ziffy’s guide to Airbnb loans before selecting the financing and insurance structure.

Multifamily Properties With 2 to 4 Units

Two-to-four-unit properties may still be financed through residential investment loan programs, but insurance underwriting can be more involved than a single-family rental. The carrier may review unit count, property age, safety features, occupancy, shared systems, and liability exposure.

Once a property reaches five or more units, investors are typically dealing with commercial property insurance rather than a standard residential landlord policy. That can change cost, underwriting, policy language, and timeline.

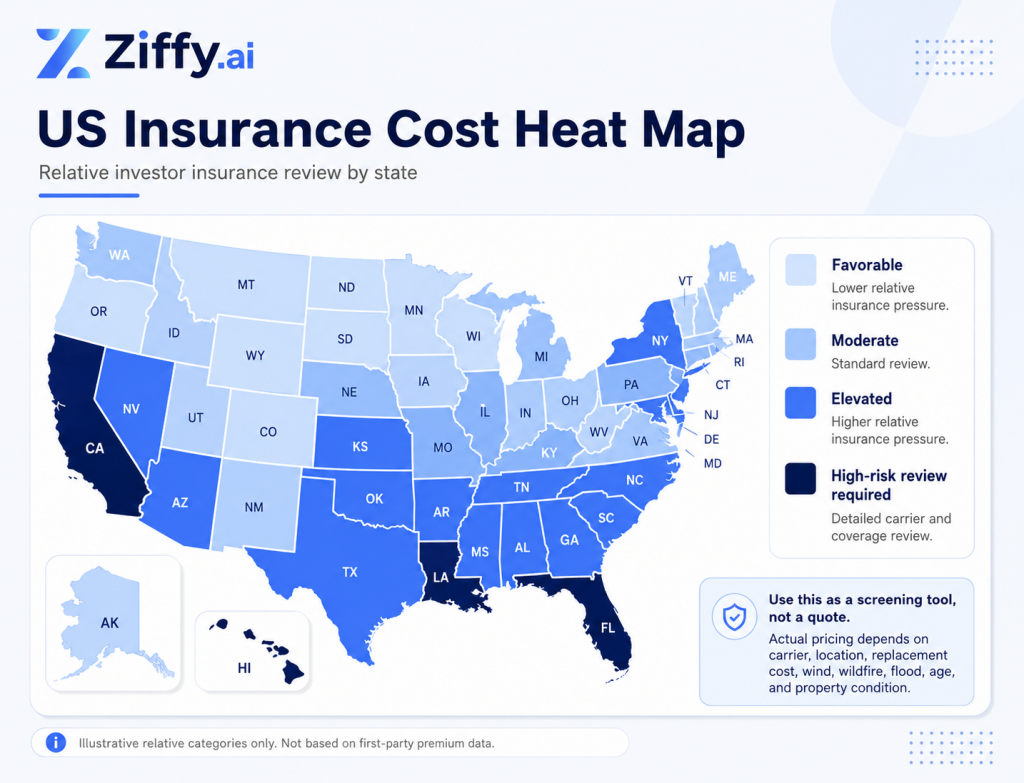

High-Risk Markets

High-risk markets require earlier insurance work. Coastal wind, hail exposure, wildfire risk, flood zones, older roofs, and carrier availability can all affect whether a quote comes back quickly and whether the premium still supports the rental math.

In Florida, wind and named-storm exposure can be a major expense, especially for coastal properties. Investors should ask whether the policy has a separate hurricane or named-storm deductible, whether wind is included or excluded, and whether a separate wind policy is required. Investors weighing Florida rentals can review current cash-flow opportunities on the Florida investment property market.

In Texas, hail and wind can materially affect coverage. The Texas Department of Insurance says windstorm insurance pays to repair or rebuild a house damaged by hail or wind from tornadoes, thunderstorms, or hurricanes.

In California, wildfire risk can affect availability and pricing. The California Department of Insurance describes the FAIR Plan as an option for property owners who cannot find coverage in the traditional market.wildfire risk can affect availability and pricing.

In Louisiana and Gulf Coast markets, wind, flood, roof age, and carrier appetite can all affect the quote. A cheap acquisition price means little if the insurance quote pushes PITIA past what rent can support.

Before buying in a coastal, hail-prone, or wildfire-exposed market, run the property through Ziffy’s investment analysis and confirm insurance with a licensed agent. A property with rent potential is only half the picture. The full expense stack, insurance included, has to support both the loan and the return target.

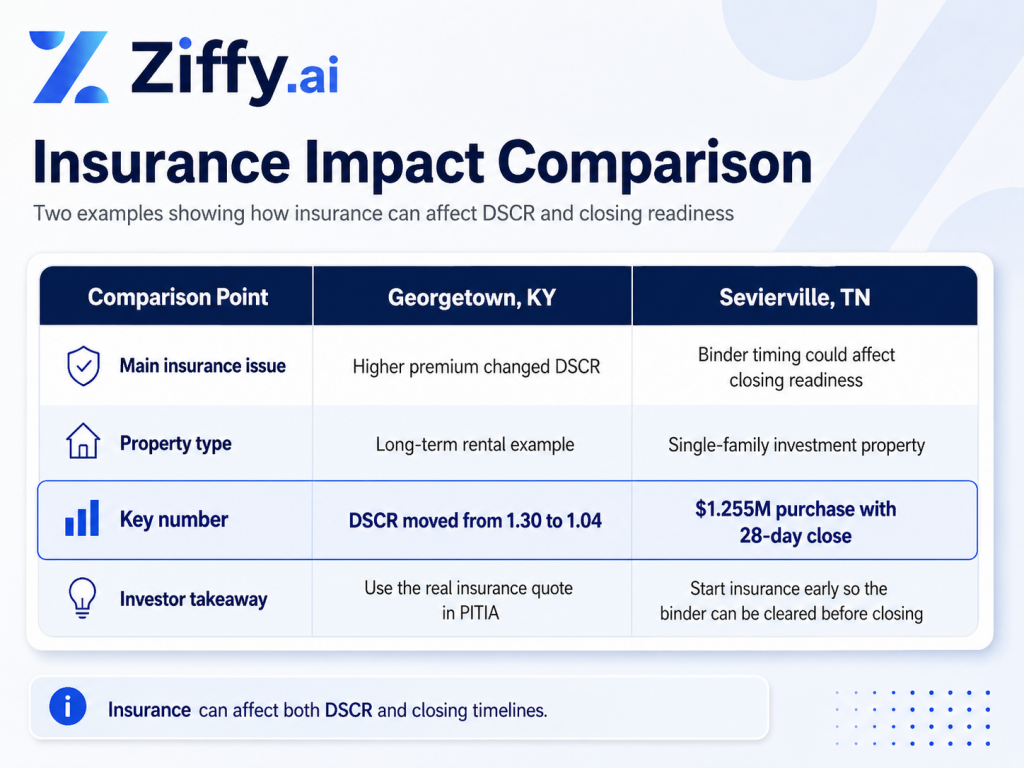

Case Study Comparison: How Insurance Changes DSCR and Closing Risk

Insurance can affect an investment property loan in the monthly numbers and in the closing process. A higher premium raises PITIA, which can tighten DSCR. A late or incorrect binder can also slow the file, even when the loan structure itself is strong.

Example 1: Georgetown, KY

Consider a long-term rental in Georgetown, KY. The first pass uses a placeholder insurance estimate. The second pass uses a property-specific insurance quote.

DSCR Input | Placeholder Insurance | Property-Specific Insurance Quote |

|---|---|---|

Monthly rent | $2,600 | $2,600 |

Principal and interest | $1,650 | $1,650 |

Taxes | $225 | $225 |

Insurance | $125 | $625 |

Association dues | $0 | $0 |

Total PITIA | $2,000 | $2,500 |

DSCR | 1.30 | 1.04 |

With the placeholder estimate, the property looks comfortable. A $2,600 monthly rent against $2,000 in PITIA gives the file an estimated DSCR of 1.30.

Once the actual insurance quote is added, PITIA rises to $2,500. Rent has not changed. Principal and interest have not changed. Taxes have not changed. The insurance line alone brings DSCR down to 1.04.

That is still above the 1.0 line, but it is a very different file. At 1.30 DSCR, the property has a cushion. At 1.04 DSCR, a revised tax figure, higher deductible concern, additional reserve requirement, or another underwriting adjustment can matter more.

This is where placeholder insurance becomes risky. It can make the rental look stronger than it really is. The real test is whether the property still works after the actual insurance quote is included in PITIA.

Example 2: Sevierville, TN

Now look at a higher-priced investment property in Sevierville, TN. This was a single-family investment property purchase with a larger loan amount and a tight closing timeline.

Loan Detail | Sevierville, TN Property |

|---|---|

Purchase price | $1,255,000 |

Approved loan amount | $1,004,000 |

Down payment | 20% |

Loan structure | 30-year full-doc investment property loan |

Closing timeline | 28 days |

This property carries a different kind of insurance risk. On a $1.255 million purchase, the insurance binder is not just another document in the file. The lender still needs to confirm the insured name, property address, coverage amount, deductible, effective date, mortgagee clause, and rental use before closing.

On a 28-day close, there is not much time to fix a late binder, a wrong mortgagee clause, a coverage mismatch, or a premium that changes the cash needed to close. Even when the loan itself is strong, insurance can still become a closing issue if it is handled too late.

For investors, the operating habit is the same in both cases: get the insurance quote early, use the real number in the DSCR calculation, and submit the binder before the file reaches final closing pressure.

The insurance number can look small compared with the purchase price, but it sits inside PITIA every month. On a tight DSCR file, one corrected premium can change how much cushion the property has. That is why we want the real quote before the file gets too far into underwriting.

The Endorsements and Add-Ons Worth Paying For

A basic landlord policy may not be enough. Endorsements can change how a claim is paid and whether the investor has to bring cash into a loss event.

Replacement Cost Coverage

Replacement cost coverage pays based on the cost to repair or replace covered property with new property of like kind and quality, subject to policy terms and limits. Actual cash value coverage accounts for depreciation. That can leave a meaningful gap after a major loss.

Investors should ask whether the policy covers replacement cost or actual cash value, and whether the roof has separate settlement terms.

Guaranteed or Extended Replacement Cost

Guaranteed replacement cost or extended replacement cost can help if rebuild costs rise above the dwelling limit. This can matter after hurricanes, wildfires, or regional disasters, when labor and materials become more expensive.

Not every carrier offers this for rentals, and limits vary. Ask the agent directly during the quote process.

Water and Sewer Backup

Many base policies do not automatically cover water or sewer backup. Older rental housing, finished basements, and properties with mature trees near sewer lines can carry higher exposure. This endorsement is usually worth discussing.

Equipment Breakdown

Equipment breakdown coverage can help with certain mechanical or electrical failures involving systems such as heating, ventilation, air conditioning, boilers, or electrical panels, depending on the policy. For investors holding older rentals, the endorsement can be useful, but it should not be confused with a maintenance plan.

Ordinance or Law Coverage

Ordinance or law coverage can pay for code-required upgrades after a covered loss. This matters in older markets where a partial loss can trigger modern code compliance during repair.

California’s 2026 residential property insurance notice says an open policy of residential property insurance that provides replacement cost coverage must include building code upgrade coverage of at least 10% of dwelling coverage policy limits. Rules vary by state, but code compliance can become a real cost after a covered loss.

Lucas Hernandez

Mortgage Loan Originator

Ziffy Mortgage

NMLS #2171747One thing that surprises investors is how quickly code upgrades can change the economics of a repair. In older markets such as Cleveland, Detroit, Memphis, and Baltimore, a major loss can trigger work that was not part of the original budget. Ordinance or law coverage is the endorsement I want investors to ask about before they assume the base policy is enough.

Umbrella Coverage

An umbrella policy adds liability protection above the limits of the underlying policy. Investors with multiple rentals, higher-value assets, short-term rentals, pools, pets, or higher tenant traffic should ask whether their liability stack is strong enough.

How to Shop for Investment Property Insurance Without Overpaying

The cheapest quote is not always the best quote. The right policy is the one that matches the property’s use, satisfies the lender, protects the investor, and does not inflate PITIA unnecessarily.

An independent insurance broker can be useful for investors comparing properties across different markets. Captive agents represent one carrier. Independent brokers can compare multiple carriers, which matters when the property is older, coastal, vacant, short-term rental eligible, or located in a market where carrier appetite changes quickly.

For coastal properties, ask about a wind mitigation inspection. In some markets, an inspection can lower the premium if the property has roof shape, opening protection, secondary water resistance, or other qualifying features.

For older properties, ask whether a four-point inspection is required. Carriers may want information on roof, electrical, plumbing, and HVAC before binding coverage.

Always compare the details, not just the annual premium.

Lucas Hernandez

Mortgage Loan Originator

Ziffy Mortgage

NMLS #2171747The quote I worry about most is the one that looks cheap because it has a 2% wind deductible. On a $300,000 dwelling limit in a coastal market, that is a $6,000 out-of-pocket number if the wrong storm comes through. The annual premium savings rarely justifies that risk.

The Insurance Timeline Inside a DSCR Loan Closing

The insurance conversation should start the day the offer is accepted.

A clean DSCR closing can move quickly, often within 30 days when the property, title, appraisal, borrower, vesting documents, and insurance are aligned. Insurance can break that timeline if the investor waits until week three.

Closing Stage | Insurance Task |

|---|---|

Day 1 to 2 after offer acceptance | Send property details to insurance agent |

Day 3 to 5 | Get landlord or rental property quote |

Day 5 to 7 | Confirm lender requirements, mortgagee clause, deductible, and replacement cost |

Day 7 to 10 | Submit binder to loan team |

Day 10 to 20 | Resolve wind, flood, roof, vacancy, or carrier questions |

Final week | Confirm paid receipt, escrow setup, and closing disclosure figures |

A binder is proof that coverage will be in force. For lender review, it usually needs to show the borrower or approved vesting structure, property address, coverage amount, effective date, premium, deductible, lender mortgagee clause, and loss payee information where applicable.

The insurance step slows deals down when it starts too late. If a property comes back in a flood, wind, or wildfire-sensitive area, you may need another week to source the right coverage. Starting that conversation in week one gives the loan team room to fix the issue without pushing the closing date.

[Graphic: DSCR Closing Timeline]

Create a 30-day horizontal timeline. Highlight days 1 to 5 as “Best time to secure quote” and days 15 to 30 as “Insurance danger zone if binder is missing.”

Ziffy’s expert mortgage loan officers target efficient contract-to-close timelines, but that only works when insurance is handled early. Investors who begin with Ziffy can review the financing path, DSCR math, and insurance-sensitive expense assumptions before the file reaches closing pressure.

Common Claims and What to Do When Something Goes Wrong

A claim is easier to manage when the investor has documentation before the damage happens.

Before a tenant moves in, record a video walkthrough of the property. Capture every room, appliances, roof condition if visible, exterior walls, mechanical systems, detached structures, flooring, ceilings, and any existing damage. Store the video with the lease, inspection report, and insurance policy.

After a covered loss, protect the property from additional damage. The California Department of Insurance advises policyholders to make reasonable temporary repairs, keep receipts, and avoid extensive permanent repairs until the adjuster has inspected the damage.

Then call the insurance company or agent. Ask what is covered, how the claim will be processed, whether estimates are needed, and what deductible applies.

For loss of rents, investors should be ready to document the lease, rental amount, occupancy status, cause of loss, and the period the property was uninhabitable. Coverage usually depends on the loss being covered under the policy.

A public adjuster may help if the claim is large, disputed, delayed, or materially under-scoped. Investors should confirm licensing rules and fee structures in the state where the property is located.

Claims can affect future premiums and insurability. A property with repeated water, roof, fire, or liability claims may become more expensive to insure or harder to place with standard carriers. That affects the next refinance, sale, or portfolio loan review.

How Investment Property Insurance Fits Into a Larger Investor Strategy

Insurance belongs in acquisition analysis, cash flow modeling, reserve planning, and exit strategy.

A BRRRR investor may need different coverage during acquisition, renovation, lease-up, and refinance. A vacant property or rehab project may require builder’s risk, vacant property coverage, or a different structure before it becomes eligible for a standard landlord policy. Investors using the BRRRR method should confirm coverage at each phase, not just after stabilization.

A short-term rental investor needs insurance that matches guest use. A long-term rental investor needs strong landlord coverage, loss of rents, and adequate liability. A multifamily investor needs to confirm whether the property still fits residential coverage or requires a commercial policy.

Insurance also affects cash planning. A property with a higher deductible, named-storm exposure, or older systems may need stronger reserves than a lower-risk property. A $10,000 wind deductible is not theoretical if the property is in a storm-prone market.

For DSCR investors, the financing question is direct: does the full PITIA support the loan? A property can have strong rent and still disappoint if insurance compresses DSCR, reduces cash flow, or increases closing cash.

Next Steps: Run the Full PITIA Before You Make the Offer

Investment property insurance should be reviewed before the loan file reaches closing. The right policy protects the property, supports the loan, preserves cash flow, and reduces the risk of a claim denial.

Before making an offer, confirm three numbers: rent, PITIA, and insurance. A rental that works with a placeholder premium can look very different once the actual binder arrives.

FAQs

Do I need insurance before closing on a rental property?

Yes. A lender will typically require acceptable hazard insurance before closing. For an investment property, the policy should match the rental use, name the correct insured party, include the lender’s mortgagee clause, and show coverage that satisfies underwriting requirements. Do not wait until the final week to start.

Will my homeowners insurance cover a tenant?

Usually not if the property is being used as a rental. Homeowners insurance is designed primarily for owner-occupied use, and rental activity can be excluded or limited. State insurance guidance says long-term or frequent rental use may require landlord property insurance or rental coverage.

What is a DP-3 policy?

A DP-3 policy is a special form dwelling policy commonly used for rental properties. NAIC defines DP-3 as open-perils coverage for the dwelling and attached structures, except for exclusions specifically listed in the policy, such as flood or earthquake.

How much liability coverage do I need as a landlord?

Many investors start with at least $1 million in liability coverage, but the right amount depends on the property, tenant profile, rental strategy, net worth, and risk exposure. Investors with multiple properties, short-term rentals, pools, pets, or higher-value assets should ask about umbrella coverage.

Can I deduct landlord insurance premiums?

Rental property insurance premiums are generally treated as rental expenses. The IRS says rental expenses can be deducted from rental income and that rental income and expenses are generally reported on Schedule E. Investors should confirm their own tax treatment with a CPA.

What if my property is in a flood zone?

If the property is in a Special Flood Hazard Area and has a mortgage, flood insurance is generally required. CFPB guidance says flood insurance is typically separate from standard homeowners insurance and that FEMA-designated Special Flood Hazard Areas have at least a one-in-four chance of flooding over a 30-year mortgage.