Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

If you are financing an investment property with a DSCR loan, the file starts with the asset. It does not start with your salary, your tax returns, or your personal debt-to-income ratio.

It starts with one question: does the property produce enough rental income to support the payment?

That is why DSCR loans work so well for many investors. With our DSCR loan program, we qualify investors primarily on the property’s rental income rather than personal income, W-2s, pay stubs, or tax returns. We are also an AI-native real estate investing platform built for investors who want to discover rentals, analyze ROI metrics, and move into financing inside the same ecosystem.

That does not make DSCR loose underwriting. Credit score, down payment, reserves, property type, taxes, and HOA also matter. The difference is that the property’s income strength carries much more weight than it would in a conventional mortgage file. We see that same logic reflected on our live listings, which flag whether a property appears to meet our 1.0+ standard DSCR threshold, comfortably qualifies, or falls below the standard lane.

This guide explains our DSCR loan terms, how those requirements work in practice, what lenders actually watch inside a file, and what separates a property that only qualifies on paper from one that is strong enough to finance with confidence.

Table of Contents

Quick answer: What are the DSCR loan requirements in 2026?

With Ziffy Mortgage’s DSCR loan program, investors can qualify with a minimum 620 credit score, a DSCR of 1.0 or higher for our best terms, and No Ratio DSCR options in eligible scenarios. Our program allows up to 85% LTV for purchases, up to 80% for rate and term refinances, and up to 75% for cash-out refinances, with loan amounts from $100,000 to $10 million and 2 months of cash reserves.

We finance investment properties, and because qualification is based on the property’s rental income, W-2s, pay stubs, and tax returns are not required for DSCR loans.

Ziffy Mortgage DSCR Loan Requirements

Requirement | Ziffy Mortgage DSCR Loan Terms |

|---|---|

Minimum credit score (FICO) | 620 |

DSCR ratio | Best terms typically apply at DSCR ≥ 1.0. If DSCR is below 1.0, the loan may still be eligible with a higher down payment. Our No-Ratio DSCR option (DSCR 0 to 1) can support investors buying properties with clear income upside, even when the property’s rent does not fully cover the monthly payment. |

LTV | Up to 85% (Purchase) |

Cash reserves | 2 months |

Loan amount | $100K – $10M |

Property use | Investment properties, residential and commercial |

Those terms tell you where a deal fits inside our DSCR program. They do not tell you whether the file is strong. A borrower at the minimum score with aggressive leverage and tight reserves is very different from a borrower with more equity, more liquidity, and a property that comfortably covers its payment. Both may have a path. One usually closes with a lot less friction.

How a DSCR Loan Actually Works

DSCR, or debt service coverage ratio can be calculated with a very simple formula:

DSCR = Gross Monthly Rent ÷ PITIA* *PITIA = Principal + Interest + Taxes + Insurance + Association Dues

A DSCR loan qualifies primarily on the property’s rental income rather than the investor’s personal income or DTI, and PITIA includes principal, interest, taxes, insurance, and HOA dues when applicable.

Let us understand this with the help of an example:

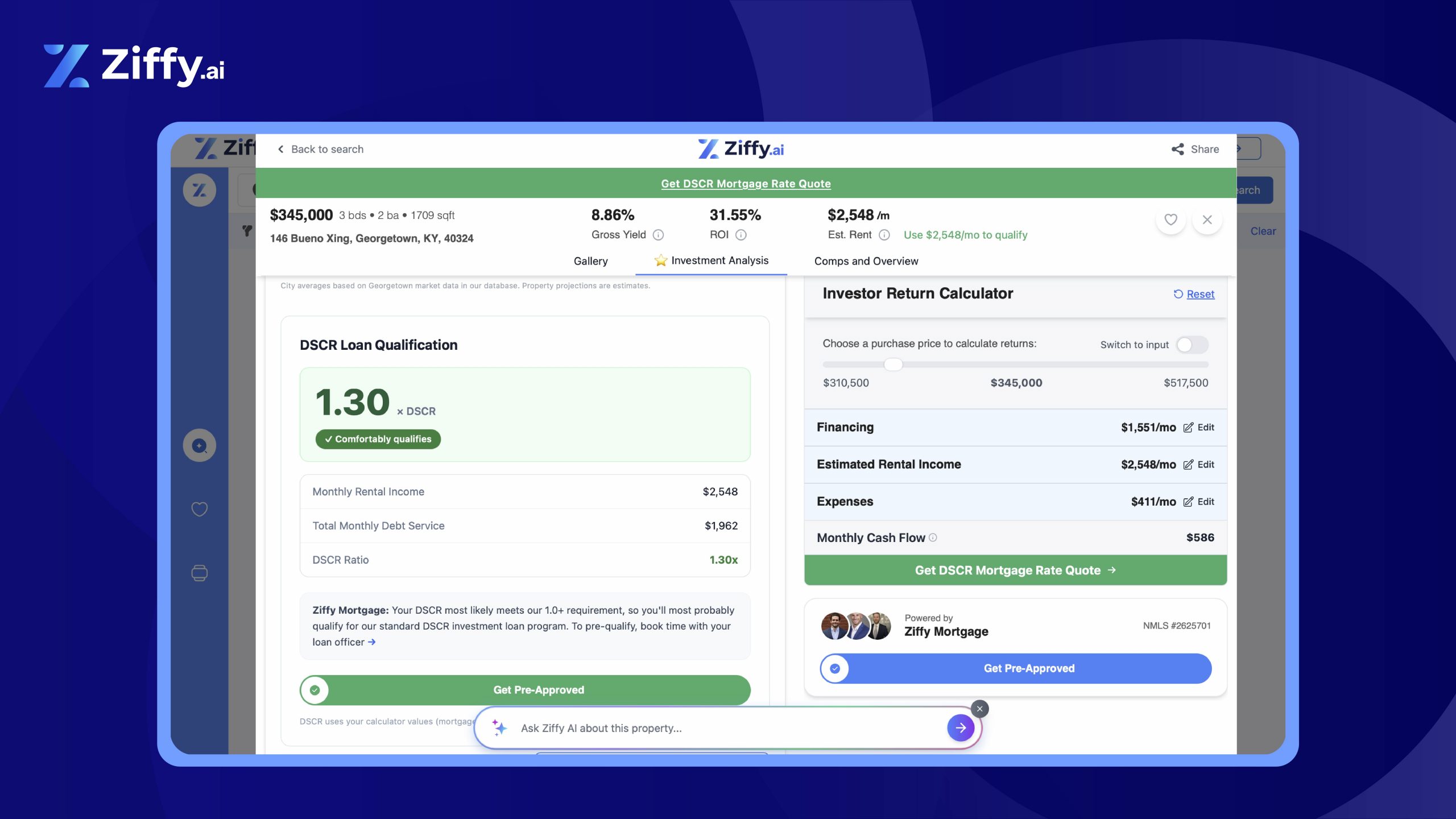

One rental property listing on our Ziffy.ai platform in Georgetown, Kentucky is estimated at $2,548 in monthly rent with $1,962 in total monthly debt service, which works out to a 1.30 DSCR. In other words, the property is projected to generate about 30% more income than it needs to cover the monthly payment, which is why it falls into a comfortably qualifying range for a standard DSCR loan.

A DSCR of 1.00 is roughly breakeven. Below that point, the property is no longer fully covering the payment, which is where loan terms usually get tighter or the structure may need to change.

If you do not want to do all the calculation manually, you can use Ziffy’s in-built DSCR loan calculator.

“DSCR loan is underwriting that starts with the property’s income.” That is exactly the heart of the product. When the rent supports the payment, the borrower’s personal income paperwork becomes much less central to the approval path.

Rent support still has to be real. Even outside the DSCR world, lenders and appraisers rely on documented rental evidence. Fannie Mae’s selling guide points to Form 1007 for one-unit investment properties and Form 1025 for two- to four-unit properties when market rent is being used, and its rental-income guidance applies a vacancy and maintenance factor rather than treating gross rent as fully collectible.

We are not underwriting a conventional loan here, but the broader lesson still applies: the rent number has to be supportable, not hopeful.

How we actually read a DSCR file

Our DSCR loan terms give you the starting point, but real underwriting does not happen one line item at a time. We do not look at credit score, leverage, reserves, and DSCR as separate boxes. We look at how they work together inside the same file.

That matters because two borrowers can both meet the minimum terms and still present very different risk profiles. A file with stronger credit, lower leverage, and more liquidity after closing usually gives us more room to work with. A file with thin reserves, higher leverage, and a ratio that only barely clears breakeven may still have a path, but it is not the same type of file.

File characteristic | Cleaner lane | Tighter lane | What it usually means |

|---|---|---|---|

Credit profile | Stronger score bands | Lower score bands | Cleaner credit usually gives the file more flexibility |

Leverage | Lower LTV | Higher LTV | More leverage raises the payment and can weaken DSCR quickly |

DSCR | Clear cushion above breakeven | Thin margin near breakeven | The thinner the ratio, the less room there is for expense changes |

Reserves | More cash left after closing | Minimum reserves only | More liquidity usually makes the file more durable |

Property profile | Straightforward rental | Higher-expense or more complex asset | Certain property types can make the same ratio feel very different |

This is where a lot of investors get tripped up. They focus on whether a deal technically fits the guidelines, but that is not the same thing as having a strong file. A property can qualify and still feel tight once real taxes, insurance, HOA dues, and post-closing liquidity are taken seriously.

Steven Glick,

Director of Mortgage Sales

What Most DSCR Guides Don’t Mention

Most DSCR guides explain the formula correctly but stop too early. The formula is not usually the part that breaks. The inputs are.

One issue we see often is a gap between the rent the investor expects and the rent the file can actually support. If the deal only works at the most optimistic rent number, the file is already thinner than it looks. That is why we pay close attention to how the rent is supported before the loan goes deeper into underwriting.

Another issue is expense timing. Taxes, insurance, and HOA dues are often treated like fixed background numbers when investors first screen a deal. In real underwriting, they are moving parts. A property can look fine at offer stage and then feel much tighter once the full payment is built with current insurance, realistic taxes, and confirmed dues.

The distinction here is that DSCR is not only about whether a property qualifies today. It is about whether the structure is still workable once the clean version of the spreadsheet gives way to the real one.

The Loan Terms That Actually Decide The File

DSCR does the heavy lifting

With our program, 1.0 or higher is where best terms generally apply, and we also offer No Ratio DSCR in eligible cases. That distinction matters. It tells you we are not treating every rental property the same way. There is a standard lane for cleaner coverage, and then there are structured options for files that do not fit the cleanest lane as easily.

In our experience, DSCR is not just an approval threshold. It is a durability test. A file at 1.02 may still have a path, but a file at 1.25 usually feels very different in underwriting and after closing. What we see often is that investors focus on whether the property clears 1.0 and stop there. The stronger question is how much room is left if rent comes in lower, insurance is revised upward, or taxes are higher than the first estimate.

Credit score still matters

Our minimum credit score for DSCR is 620. That is the floor, not a promise that every 620-score file will look equally strong. Credit still affects how the rest of the package is viewed, especially if the ratio is thin or the borrower is pushing leverage.

What we see often is that borrowers hear “qualify on rental income” and assume their own credit profile barely matters. In practice, it still shapes how the rest of the file is read. In our experience, cleaner credit gives us more flexibility when a file is otherwise strong. Thin credit usually means the rest of the structure has to work harder.

Down payment and LTV shape the whole structure

With our DSCR loan program, we go up to 85% LTV for purchases, up to 80% for rate and term refinances, and up to 75% for cash-out refinances. You need to understand this because leverage changes more than your cash to close. It changes the monthly payment, which changes PITIA, which changes DSCR.

Here is a simple illustration to help you understand this:

Scenario | Loan Amount | Monthly PITIA | Monthly Rent | DSCR |

|---|---|---|---|---|

20% down on a $400,000 purchase | $320,000 | $2,740 | $3,200 | 1.17 |

25% down on the same property | $300,000 | $2,560 | $3,200 | 1.25 |

Nothing changed except leverage. The property and rent are the same. The ratio is materially stronger with more equity in the deal.

This is one of the most common turning points in DSCR structuring. An investor focuses on keeping as much cash as possible on day one, then realizes that the lower down payment is weakening the very math the loan depends on.

Reserves matter because ownership starts after closing

Our cash reserve requirement is 2 months. That can sound modest on paper, but the concept matters more than the number alone. Reserves are how we judge whether the borrower has room to absorb normal ownership friction after closing.

A property can qualify and still run into the real world immediately. Vacancy happens. Insurance renewals rise. Repairs do not wait for the perfect month. Minimum reserves may satisfy the guideline, but they do not automatically mean the property is comfortably capitalized. That is why the strongest files are rarely the ones that solve only for the closing table.

Property type, taxes, insurance, and HOA dues can move the ratio quickly

We finance single-family homes, townhouses, condominiums, and multi-family properties, and we also help with larger multi-family and commercial through our commercial arm. That is useful for investors, but it also means you cannot assume every property behaves the same way in underwriting.

This is where expense discipline matters. Tax Foundation’s 2026 property-tax work shows just how much effective property taxes can vary by state and county, and Treasury’s Federal Insurance Office reported in early 2025 that homeowners insurance is becoming more costly and harder to procure for millions of Americans. Those two inputs land directly inside PITIA. When they move, your DSCR moves with them.

You can learn more about taxes in our Tax guide.

Steven Glick,

Director of Mortgage Sales

How to Evaluate a DSCR Deal Before You Apply

The cleanest way to approach a DSCR loan is to review the file in the same order we do. In our experience, the cleanest DSCR files are usually the ones where the investor underwrites the property almost the same way we do before the file ever reaches full underwriting.

Start with the supported rent, not the rent you hope to get after a perfect lease-up. If the property is occupied, compare the lease to market reality. If it is vacant, use conservative rent comps. The goal is not to find the most flattering number. The goal is to find the number an underwriter can defend.

Then build the real PITIA, not just principal and interest. Taxes may be higher than the seller’s old bill. Insurance may be significantly higher than your early placeholder number. HOA dues can quietly wipe out the cushion in a condo or townhouse deal. This is exactly why our loan officers emphasize validating taxes, insurance, and HOA dues before relying on a DSCR estimate.

Once you have those two numbers, calculate the ratio. Then stress-test it. Reduce rent. Increase insurance. Recheck taxes. If the property still works, the file is sturdier. If it stops working immediately, that tells you something important before you spend time and money on a full loan package.

After the property math works, check the borrower-side terms. Is your credit at or above 620? Are you keeping leverage in a range that still leaves the ratio healthy? Do you still have the required reserves after closing? If this is a refinance, are you inside the right LTV bucket? Is the property type one we actually finance? When those answers are clear up front, the process gets simpler. When they are not, the file usually gets slower, more expensive, or both.

Detailed Case Study: A 28-day DSCR Closing

One recent client from Georgia (Olivia Smith – name changed) bought a single-family rental in Princeton, Texas using a 30-year fixed DSCR loan, with a $240,000 purchase price, 25% down, $180,000 loan amount, 7.250% interest rate, and a 28-day closing time. That translates to a 75% LTV structure, which is exactly the kind of leverage range that tends to give DSCR files more stability than a max-leverage approach.

Loan Details

Location | Princeton, Texas |

Property Type | SFR (single-family rental) |

Purchase Price | $240,000 |

Down Payment | 25% (60,000) |

Loan Amount | $180,000 |

Interest Rate | 7.250% |

Loan Term | 30 Years |

Loan Type | DSCR Loan |

Closing Time | 28 days |

Loan Timeline

Stage | Date | What Happened |

|---|---|---|

Registration, program selection, and underwriting review | January 15, 2026 | Property and borrower details were submitted, the file was matched to the DSCR loan program, and verification began. |

Final approval and closing | February 12, 2026 | The loan was approved and completed within a month. |

Honestly, I thought this was going to be a lot harder than it was, but the team kept it simple. They told me exactly what they needed, explained each step clearly, and kept things moving. What made the biggest difference for me was that the loan was structured around the property’s rental income instead of the usual paperwork headaches. By the time we got to closing, I felt like I actually understood the process instead of just reacting to it.

Olivia Smith, bought SFR in Princeton, Texas

The reason this case matters is not only the speed, but also the structure. The loan was built around the property’s income rather than the borrower’s US income, and the documentation requirements were clearly defined from the start. The case study itself says the file worked because it was structured around property income, used a 25% down payment aligned with DSCR standards, and paired fixed-rate financing with clear documentation from the outset.

DSCR files move best when the leverage is sensible, the property’s income story is clear, and the documentation is not being invented halfway through the process.

Investment Properties on Sale in Texas Today

Powerful tools to help you identify the most profitable investment opportunities

What Counts as a Good DSCR in Real Life?

A good DSCR is not one magic number. It depends on how much cushion you want in the deal and how sensitive the property is to expense changes.

- A property below 1.0 is not fully covering the payment. That does not always eliminate financing, because we do offer No Ratio DSCR in eligible cases, but it does mean the file is no longer sitting in the cleanest standard lane.

- A property between 1.0 and 1.10 would still qualify, but it is thin. There is very little room for rent softness or expense movement. You can see that logic reflected on our live listings, where a 1.05x file is shown as qualifying, while higher-coverage files are labeled as comfortably qualifying.

- A property between 1.10 and 1.25 is healthier. It is doing more than barely carrying itself.

- A property at 1.25 and above usually feels stronger because it has operating cushion. Our own listings show that difference clearly, with examples around 1.26x, 1.33x, 1.34x, and 1.45x presented as comfortable qualification territory rather than bare-minimum territory.

The real question is not whether the property can get approved. The real question is whether it will still feel like a good investment after taxes, insurance, HOA dues, and normal ownership friction show up.

Common Mistakes That Weaken DSCR Files

Using the most optimistic rent number

One of the most common mistakes we see is investors underwriting to the rent they want rather than the rent the file can actually support. If the property only works at the very top of the rent range, the ratio is already more fragile than it looks.

“A lot of DSCR files do not get weaker because the property is bad. They get weaker because the rent story was too optimistic at the start.” – Steven Glick, Director of Mortgage Sales, Ziffy Mortgage | NMLS# 1231769

Building PITIA with placeholder expenses

Taxes, insurance, and HOA dues are not side notes. They are often what moves the ratio. In our experience, many of the files that tighten after contract do so because the early payment estimate was too loose, not because the property itself changed.

“When a deal looks good early and then feels tight later, it is usually the expenses, not the concept, that changed the file.” – Steven Glick, Director of Mortgage Sales, Ziffy Mortgage | NMLS# 1231769

Treating minimum reserves like comfortable reserves

Meeting the reserve requirement is not the same as being well-positioned to own the property. A file can satisfy the guideline and still leave the borrower with too little room for vacancy, turnover, insurance changes, or repair costs after closing.

Pushing leverage just because the program allows it

Maximum leverage is not always the best structure. In our experience, some of the strongest DSCR files are not the ones using every bit of leverage available. They are the ones where the borrower gives the ratio enough room to stay healthy after the deal closes.

Treating DSCR like a shortcut instead of a fit

DSCR is powerful when the property, leverage, reserves, and ownership plan all line up. It gets messy when investors try to use it to rescue a deal that never really made enough sense in the first place.

Final Thoughts

A DSCR loan is not just a way to skip traditional income paperwork. It is a way to finance investment property based on whether the asset actually supports long-term debt. That makes it a strong fit for many investors, but only when the rent is supportable, the PITIA is real, the leverage is sensible, and the borrower still has room after closing.

That is also why the sequence matters. First find the deal. Then test the rent and the payment. Then decide whether the structure still makes sense. Our platform is built around that investor workflow, from rental discovery and return analysis to investor-friendly financing, and our live mortgage page makes clear that the goal is not just to quote loans, but to help investors move from screening to acquisition with the financing path already aligned to the asset.

FAQs

What credit score do I need for a DSCR loan?

With our DSCR loan program, the minimum credit score is 620. That said, the minimum score is not the same as a strong file. A borrower at 620 with aggressive leverage and thin reserves is very different from a borrower with better credit, more cash left after closing, and a property that comfortably covers its payment. The lower the margin in the deal, the more important the rest of the file becomes.

What DSCR ratio do you look for at Ziffy Mortgage?

For our best terms, we generally look for a DSCR of 1.0 or higher. We also offer No Ratio DSCR in eligible scenarios. The most important thing to understand is that qualifying at 1.0 and qualifying comfortably are not the same thing. A property just above breakeven has much less room for rent softness, insurance changes, or tax adjustments than a property with a stronger ratio.

Can I get a DSCR loan if the property is below a 1.0 DSCR?

In some cases, yes. We offer No Ratio DSCR options for eligible deals. Whether that structure makes sense depends on the property, the leverage, the reserves, the credit profile, and the overall strength of the file. The honest answer is that not every below-1.0 property is a good fit just because there is technically a path. The property still has to make sense as an investment.

How much down payment do I need for a DSCR loan?

For purchases, we allow up to 85% LTV, which means some files may go as low as 15% down. That does not mean the lowest possible down payment is always the best structure. In many DSCR files, putting more money down improves the monthly payment, strengthens the ratio, and gives the deal more room if taxes, insurance, or rent support come in less favorably than expected.

Do I need W-2s, pay stubs, or tax returns?

No. With our DSCR loan program, qualification is based primarily on the property’s rental income, so W-2s, pay stubs, and tax returns are not required. That is one reason DSCR works well for self-employed investors, LLC borrowers, and buyers whose tax returns do not reflect their true borrowing capacity the way a conventional lender would want.

Do you check my debt-to-income ratio for a DSCR loan?

No, traditional personal DTI calculation is not required for our DSCR program. The focus is on whether the property’s rental income can support the monthly housing payment. That is a major difference between DSCR and conventional financing for investment properties.

Can I use a DSCR loan to buy through an LLC?

Yes, DSCR loans are commonly used by investors buying through an LLC. That is one reason the product is attractive for portfolio building and long-term asset planning. The property still has to qualify, and the final structure still depends on the file, but LLC borrowing is a normal part of DSCR lending.

Can I refinance an investment property with a DSCR loan?

Yes. We offer DSCR financing for purchases, rate and term refinances, and cash-out refinances. Our current structure allows up to 80% LTV for rate and term refinances and up to 75% LTV for cash-out refinances. If your goal is to pull equity out of a stabilized rental without documenting personal income the way a conventional lender would require, DSCR can be a strong fit.

How fast can you close on a DSCR loan?

We can often close in 15 to 30 days, depending on the property, the documentation, and the overall file. The deals that move fastest are usually the ones where the rent support, payment structure, reserves, and ownership setup are already clear before the loan goes into full underwriting.