Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Quick answer

You can finance a second investment property with another debt service coverage ratio (DSCR) loan while the mortgage on your first rental is still outstanding. The new property must qualify through its own rental income, but the lender will also review what has happened since your first closing: your mortgage payment history, remaining liquidity, credit changes, existing rental obligations, and ownership structure.

Ziffy Mortgage currently offers eligible DSCR purchases at up to 85% loan-to-value, so a minimum down payment of 15% may be available, subject to the full loan review. The highest available leverage is not always the strongest portfolio decision. Your second loan should leave enough cash for both properties to operate and enough borrowing capacity for the next acquisition.

Table of Contents

What Changes After Your First DSCR Loan?

A DSCR loan still qualifies the new rental primarily through property income rather than W-2s, pay stubs, personal tax returns, or a traditional debt-to-income calculation. The second application contains more evidence because you now have an investment mortgage and an operating rental.

Your first mortgage becomes part of the underwriting record

Before the first purchase, the lender reviews your credit, assets, entity documents, and proposed property. After closing, your investment-mortgage payment history can also be evaluated.

Recent late payments, returned payments, unresolved servicing issues, or a sharp credit decline can weaken the next application. A clean history helps show that the first purchase did not create immediate financial stress.

The lender may request an updated mortgage statement, lease, insurance declaration, property tax information, homeowners association dues, and proof of ownership. If the first property is vacant or operating below its original projections, that does not automatically prevent approval, but it changes the broader portfolio review.

Reserve funds now have to support more than one property

The first purchase may have used cash for the down payment, closing costs, repairs, furnishing, or lease-up. The second application starts with what remains.

Ziffy’s published DSCR loan requirements set the baseline, but the final reserve requirement can change with credit, leverage, loan size, DSCR, Property Use, and the number of financed properties.

In our experience, investors are more likely to underestimate post-closing liquidity on the second purchase than the down payment itself. They may have enough to close but not enough acceptable funds left to satisfy underwriting and carry two rentals through a vacancy or major repair.

The Ziffy guide to cash reserves for investment property loans explains how reserve needs can change as a portfolio grows.

Lucas Hernandez

Mortgage Loan Originator

Ziffy Mortgage

NMLS #2171747“f you are scaling, assume the lender will care about more than the property you are buying today.

The second property still has to carry its own payment

Strong performance from the first rental does not compensate for unsupported rent on the new property.

For most residential DSCR loans:

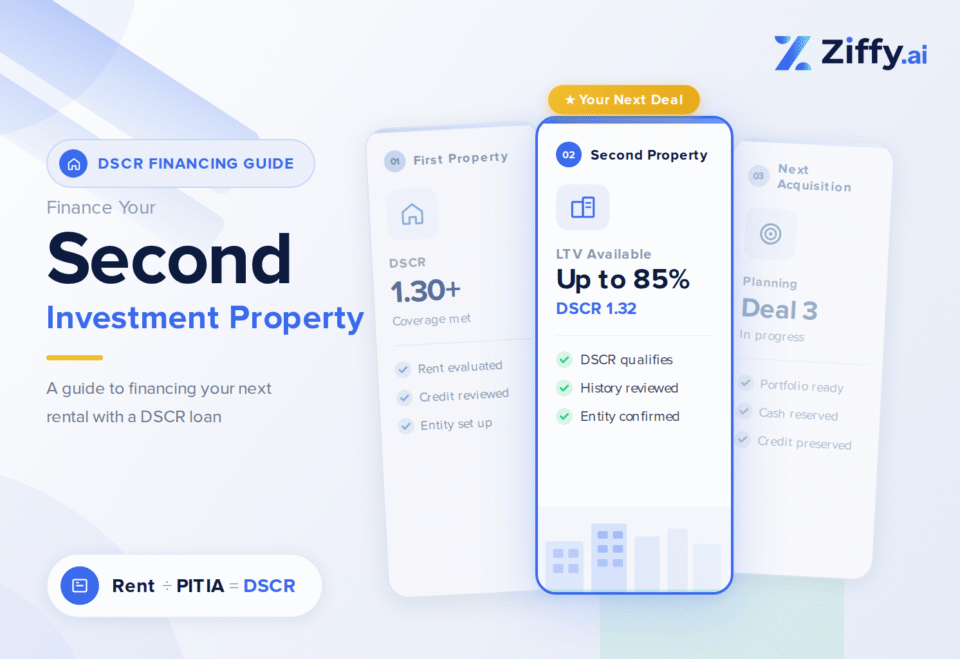

DSCR = Gross monthly rent ÷ Monthly PITIA

PITIA includes principal, interest, property taxes, homeowners insurance, and association dues when applicable. A 1.00 DSCR means supported rent equals the monthly housing obligation.

Use full PITIA when testing the deal. Ziffy’s DSCR loan calculator lets you adjust the purchase price, down payment, interest rate, taxes, insurance, and HOA dues before making an offer.

A Gonzales, TX single-family rental reviewed on Ziffy in June 2026 had estimated monthly rent of $1,331 and estimated PITIA of $1,007, producing a 1.32 DSCR. The figures are specific to the property and the financing assumptions used at the time, not a guarantee of approval or future performance. The example shows how a property with rent coverage above 1.00 can provide more room for changes in taxes, insurance, or other housing costs.

Investment Properties on Sale Today

At Ziffy, we track more than 964,000 active US listings, giving investors a broad base for comparing rent, cash flow, and financing assumptions before narrowing the search to a specific property.

The first rental should also be recalculated with current expenses. Property taxes may reset after purchase, insurance can rise at renewal, and HOA assessments can change. Those costs do not alter the new property’s DSCR, but they reduce the cash available to support the portfolio.

Credit and entity documents receive another review

DSCR financing removes personal income qualification from the center of the file. It does not remove credit, asset, title, or entity review.

The lender can evaluate your credit score, recent inquiries, new obligations, mortgage history, and source of funds. Financing furniture, vehicles, renovations, or another acquisition immediately after the first closing can change the profile presented on the next application.

A pattern we have seen slow down otherwise workable purchases is a preventable documentation issue: large transfers with no paper trail, a purchasing limited liability company (LLC) that does not match the contract, expired entity records, or title and insurance prepared in different names.

Before submitting the offer, confirm the operating agreement, ownership percentages, employer identification number, signing authority, good-standing status when required, and the entity that will take title.

First DSCR loan versus second DSCR loan

Three Ways to Finance the Second Investment Property

Use another DSCR purchase loan

For a stabilized rental, another DSCR loan is usually the most direct structure. Ziffy’s standard published terms currently include financing of up to 85% loan-to-value on eligible purchases, subject to the full loan review.

A larger down payment may still be the better decision if it improves DSCR, lowers the payment, strengthens pricing, or leaves a safer monthly cash-flow margin. Ziffy’s guide to investment property loans can help you compare the available structures before selecting one.

In one Ziffy-financed Princeton, TX investment purchase, the property closed at $240,000 with 25% down in 28 days. The deal shows why leverage and execution should be matched to the file rather than pushed automatically to the program maximum.

To be clear, DSCR financing may carry higher pricing than a conventional investment-property loan. That is the trade-off for qualifying primarily through property income without relying on personal income documentation. Compare the rate, points, prepayment terms, cash required, and expected hold period rather than judging the options by rate alone.

Use equity from the first rental

A DSCR cash-out refinance can convert part of the first property’s equity into funds for the next down payment, renovation budget, or reserves.

Before refinancing, model the first rental with the proposed new loan amount. Confirm that the revised payment still leaves enough cash flow for repairs, vacancies, and the property’s normal operating costs. Seasoning requirements, closing costs, and any prepayment penalty on the existing mortgage also affect whether the transaction makes sense.

Use bridge financing within a BRRRR strategy

A property needing substantial renovation may not be ready for permanent DSCR financing at purchase. Missing systems, incomplete work, severe deferred maintenance, or rent that cannot yet be supported can make a stabilized rental loan the wrong first step.

A bridge loan can finance the acquisition and renovation period. Once the property is rent-ready and its income can be documented, the investor can refinance into a long-term DSCR loan.

This is the financing sequence behind the buy, renovate, rent, refinance, and repeat (BRRRR) strategy. The complete BRRRR method guide covers the acquisition-to-refinance cycle in more detail.

Where Conventional Financing Begins to Restrict Portfolio Growth

Conventional financing can still work for an investor with strong documented income, an acceptable debt-to-income ratio, and a limited financed-property count.

What many comparisons skip is that the practical constraint can appear before the formal property ceiling. Fannie Mae allows up to 10 financed properties for Desktop Underwriter second-home and investment-property transactions, while additional reserve requirements apply as the financed-property count rises.

Review the current Fannie Mae multiple financed property rules and Ziffy’s DSCR versus conventional loan comparison before deciding which structure protects more future borrowing capacity.

What We Have Seen Derail Second-Property Closings

The second file often slows down for reasons that could have been handled before the property went under contract.

- Unseasoned or unexplained funds: Document transfers, large deposits, and the source of the down payment as they occur.

- Reserves counted twice: Do not use the same dollars for closing and post-closing reserves.

- Old expense assumptions: Recalculate taxes, insurance, and HOA dues instead of reusing the first property’s estimates.

- Entity mismatches: Make sure the contract, title, insurance, bank account, and loan file use the approved vesting structure.

- New consumer debt: Avoid large financed purchases while preparing the next application.

- No portfolio stress test: Check whether you could carry both mortgages through a vacancy, major repair, or insurance increase.

Use Ziffy’s guide to finding cash-flow properties to screen deals before the financing review begins.

Prepare the Second Loan With the Third Purchase in Mind

The financing structure for your second property should close the current deal without consuming the liquidity, credit strength, and leverage you will need for the next acquisition.

Keep the first mortgage current, update its actual operating costs, and test the next property with full PITIA before making an offer. Use Ziffy’s AI-native real estate investing platform to compare rental income, cash flow, return estimates, and financing within the same deal review.

FAQs

Can I get a second DSCR loan soon after closing the first one?

A second purchase may be possible soon after the first closing when you still have sufficient liquidity, acceptable credit, clean mortgage history, and a new property with supportable rent. A separate purchase does not have one universal waiting period, although program rules and lender exposure limits still apply.

Timing becomes more restrictive when the next purchase depends on cash-out proceeds from the first property because refinance seasoning rules vary.

Does the rent from my first property help the second property qualify?

The first rental’s performance can strengthen the overall portfolio review, but it does not replace the second property’s rent requirement. The new property generally must qualify using its own supported rent and PITIA under the applicable DSCR or no-ratio program.

Should I use the same LLC for both investment properties?

The same LLC may be permitted, but the right structure depends on the program, ownership plan, bookkeeping, liability strategy, and future sale plans. Confirm the proposed vesting with Ziffy before finalizing the contract and consult qualified legal and tax professionals for advice specific to your portfolio.