Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Quick Answer: What Changed on June 17, 2026

The June 17 Fed decision did not lower borrowing costs for DSCR investors. The Fed held rates steady, but the updated dot plot and Warsh’s press conference pushed the market conversation toward higher-for-longer financing risk. The most important signals after this meeting are lender pricing and the 10-year Treasury. Both will show whether the June dot plot is already moving investor loan quotes.

Table of Contents

Post-Decision Update

The Federal Reserve held the federal funds target range at 3.50% to 3.75% on June 17, 2026, with a 12–0 vote. The more important shift for real estate investors came from the updated Summary of Economic Projections and Chair Kevin Warsh’s first post-meeting press conference as Fed Chair.

The June dot plot moved in a more restrictive direction. The median projected federal funds rate for the end of 2026 rose to 3.8%, up from 3.4% in the March projections. The distribution also changed meaningfully: nine participants projected a rate above the current midpoint, eight projected the current midpoint, and one projected a lower rate. In plain terms, the Fed did not hike at this meeting, but the committee’s projections no longer look like a clean path toward lower rates.

The inflation update explains the shift. The Fed’s median 2026 PCE inflation projection rose to 3.6%, compared with 2.7% in March. Core PCE inflation moved to 3.3%, also up from 2.7% in March. The statement said inflation remains elevated relative to the Fed’s 2% goal, partly because supply shocks have pushed prices higher in certain sectors, including energy.

For DSCR investors, the answer is direct: underwrite at today’s rate and do not build the deal around a rate cut. Underwrite at today’s rate and confirm the rent supports PITIA even if taxes, insurance, or vacancy run higher than the initial estimate.

How the June 17 Decision Affects Rental Property Financing

The Fed held rates, but the meeting shifted the rate narrative. The dot plot and Warsh’s press conference both pointed toward higher-for-longer rather than toward cuts.

Going into the decision, many investors were watching for a possible easing signal from Chair Kevin Warsh. Instead, the June statement was shorter and more explicitly focused on inflation control. The committee described solid economic activity and steady job growth, and said nothing that reads like a setup for rate cuts. Nothing in that language reads like a Fed preparing to cut rates.

The statement also removed the kind of forward guidance investors often look for after a Fed meeting. Between now and the July 28–29 meeting, incoming inflation data, jobs reports, and Treasury-market movement carry more weight than usual.

For DSCR borrowers, the Fed funds rate is not the mortgage rate. DSCR loan pricing usually moves with broader credit conditions, Treasury yields, mortgage-backed securities, lender appetite, and investor demand for rental-property loans. Still, the Fed influences all of those channels. A Fed that sounds comfortable holding rates steady, or even hiking later, can keep long-term yields elevated and make investor mortgage pricing harder to predict.

The Rate Decision: No Cut, No Hike, No Immediate Relief

The Fed maintained the target range for the federal funds rate at 3.50% to 3.75%. The vote was unanimous at 12–0.

The unanimous vote is notable: no formal dissent pushed for a cut or a hike in the actual decision. The disagreement showed up in the projections instead. The dot plot is where the split became visible.

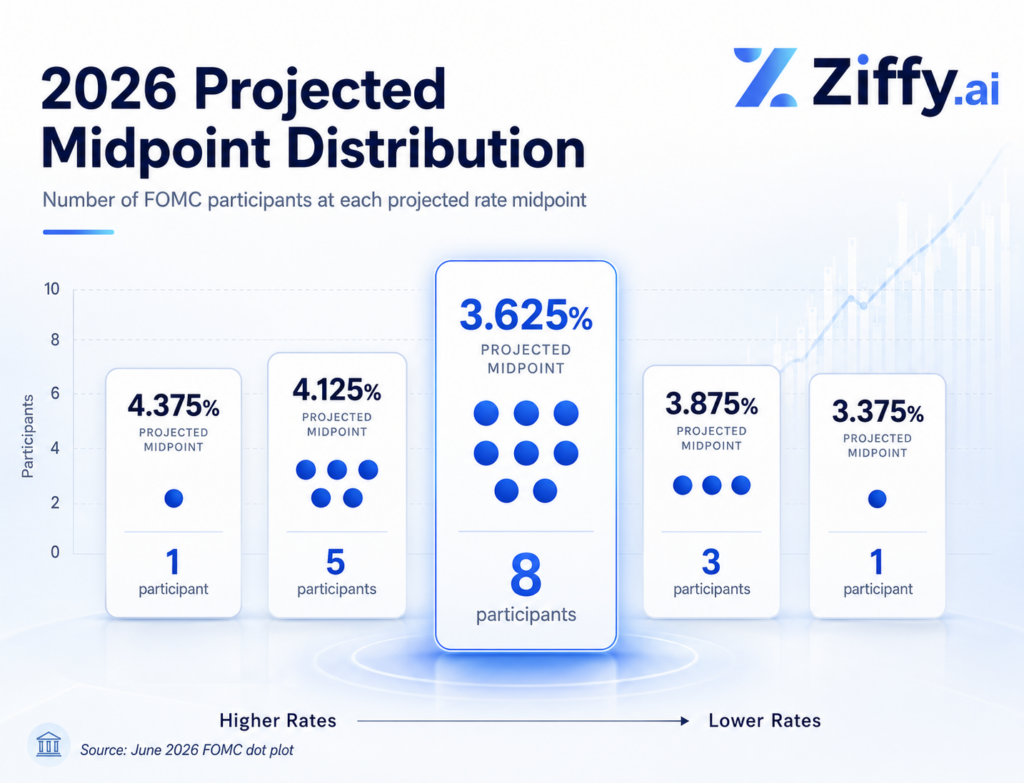

The current target range has a midpoint of 3.625%. In the June projections:

Half of the submitting participants projected a higher year-end rate than the current midpoint. Eight projected no change from the current midpoint. Only one projected a lower year-end rate.

The Fed may not have moved in June, but the committee is not sending a broad-based “cuts are coming” message.

The June Dot Plot: What Changed and What It Signals

The dot plot does not set DSCR rates, but it shapes expectations around the rate path, and those expectations flow into how markets price investor loans.

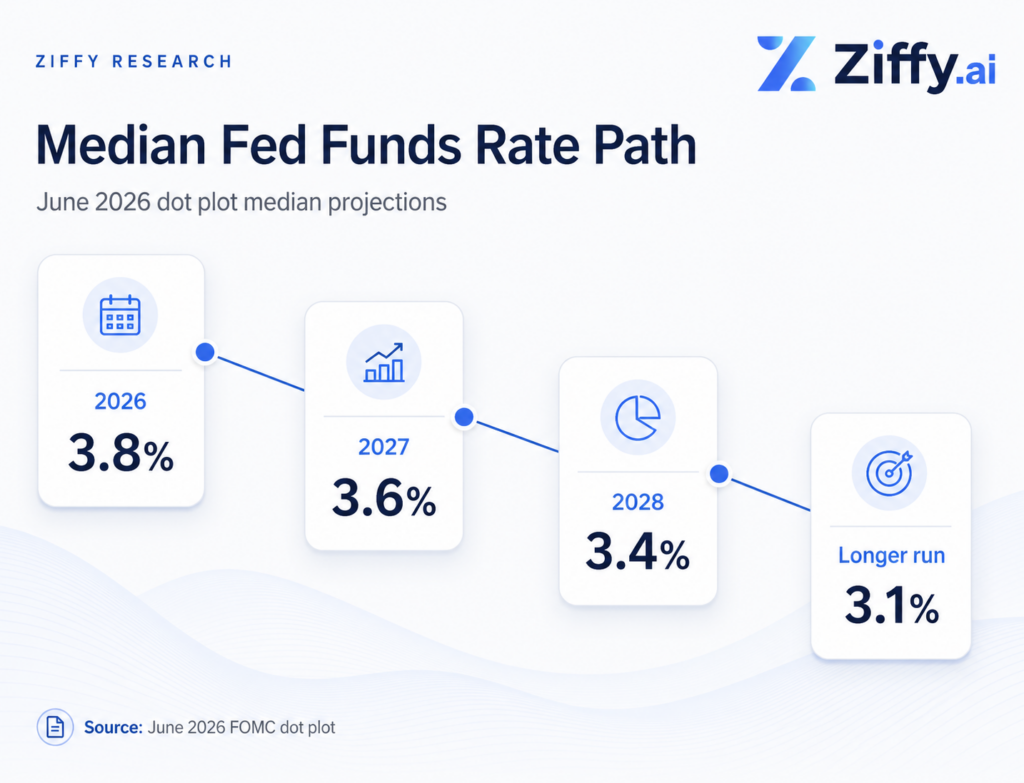

The June projections now show a median federal funds rate of:

The March projection for 2026 was 3.4%. The June projection at 3.8% is a clear upward revision.

A DSCR borrower should not read this as a promise that rates will rise. The Fed’s own projections are conditional, and the path can change if inflation cools faster, labor weakens, or financial conditions tighten. But the June SEP makes one thing harder to justify: assuming a near-term refinance will automatically rescue a thin DSCR file.

Rental investors make this assumption often. An investor sees a property that barely clears DSCR today, assumes rates will fall, and plans to refinance into a better payment later. That can work when the numbers already have room. It becomes risky when the acquisition only makes sense if future rates fall.

At Ziffy, the starting point is today’s rate, not a projected future rate. If rates improve later, the refinance becomes upside. It should not be the only reason the deal works.

How the Fed’s Inflation Projections Moved in June

The Fed’s inflation projections moved up sharply in June.

Projection | March 2026 | June 2026 |

|---|---|---|

2026 PCE inflation | 2.7% | 3.6% |

2026 core PCE inflation | 2.7% | 3.3% |

2027 PCE inflation | 2.2% | 2.3% |

2027 core PCE inflation | 2.2% | 2.5% |

The Fed still projects inflation moving lower in 2027, but the near-term inflation picture is worse than it looked in March. The June statement specifically pointed to supply shocks and energy as contributors to elevated inflation.

If inflation pressure is tied to energy, insurance, repairs, utilities, and operating costs, the impact does not stop at the mortgage rate. It can show up in the property’s actual cash flow.

A rental property can lose margin from both directions at once:

DSCR investors should not only ask, “What is the rate?” They should also ask whether the rent can carry the full monthly housing cost after the property’s most likely expense increases.

What Warsh Said and What He Avoided

Chair Kevin Warsh’s first post-meeting press conference signaled a different communication style. Reuters reported that Warsh said forward guidance is not well suited to the current economic environment and confirmed he did not submit a projection for the dot plot. Reuters also reported that the Fed’s statement was streamlined and that markets responded with higher Treasury yields, a stronger dollar, and modest stock declines after the meeting.

For DSCR investors, the press conference tone matters less for what Warsh predicted and more for what he avoided predicting. A Fed that gives less forward guidance leaves markets to react more directly to inflation data, jobs data, oil prices, Treasury auctions, and risk sentiment.

Less forward guidance means more rate volatility between meetings, not less. Rate locks and underwriting assumptions become harder to time when markets have no clear Fed roadmap to lean on.

What DSCR Investors Should Watch Next

1. The 10-Year Treasury

The 10-year Treasury is not the same thing as a DSCR mortgage rate, but it is one of the cleanest market signals for long-term borrowing costs. When 10-year yields rise, mortgage pricing often feels pressure, especially for investor loans.

A Fed hold does not automatically mean mortgage rates fall. After this meeting, the more relevant question is whether markets believe inflation is moving lower fast enough to prevent another hike.

2. Lender Pricing and Investor Loan Spreads

DSCR loans are business-purpose rental-property loans. Pricing can move differently from owner-occupied conventional mortgages because the loan is evaluated through property income, investor risk, leverage, reserves, and secondary-market appetite.

The Fed sets the backdrop, but the actual DSCR loan still comes down to the file.

3. Rent Support

In a higher-rate environment, rent support becomes the center of the deal. A property with strong rent coverage can absorb more movement in pricing. A property barely clearing DSCR can fall out of range with a modest payment increase.

At Ziffy, DSCR is calculated as:

Monthly rental income ÷ monthly PITIA

PITIA usually includes principal, interest, taxes, insurance, and applicable association dues. If interest, taxes, or insurance increase, the denominator rises. Unless rent rises too, DSCR falls.

4. Insurance and Taxes

Investors often focus on the interest rate because it is the most visible number. Taxes and insurance can do just as much damage to DSCR.

In markets where reassessments, storm risk, or insurance repricing are already running, the impact compounds faster. Before locking in a DSCR loan, investors should confirm the insurance quote, review the tax history, and check whether the purchase could trigger a reassessment.

5. Refinance Assumptions

A future refinance can make sense as upside, but it cannot be the only reason the deal works.

If the loan only works because the investor assumes rates will drop quickly, the deal is carrying rate-path risk. The June Fed meeting did not remove that risk. If anything, the updated dot plot makes the refinance assumption less comfortable.

A stronger DSCR plan asks:

- Does the property work at today’s rate?

- What happens if the rate is 0.25% to 0.50% higher?

- Does DSCR still clear if insurance rises?

- Are reserves strong enough after closing?

- Is the hold period long enough to justify points or closing costs?

How a Higher Rate Can Change DSCR

A small rate change can move the DSCR more than investors expect.

Let’s understand this using this simple example:

The property may still qualify, depending on program requirements and the rest of the file, but the cushion is thinner. If insurance or taxes also move higher, the deal can get tight quickly.

That is why DSCR investors should treat the Fed decision as a signal to tighten underwriting discipline, not as a reason to pause every acquisition. Strong rental deals can still work. Thin deals need more scrutiny.

What Ziffy Is Watching After the Fed Decision

Ziffy’s view after the June meeting is not that investors should wait for perfect conditions. Waiting for lower rates can mean missing properties where rent coverage and long-term rental demand already justify the acquisition.

For investors using Ziffy, the right starting point is three numbers before getting attached to the property:

- Estimated rent

- PITIA estimate

- DSCR

Ziffy’s AI-native real estate investing experience is built for that workflow. Investors can evaluate rental income, projected cash flow, ROI, and financing fit before treating a listing as a serious acquisition candidate. That matters even more when the Fed is not giving investors a clean path to cheaper debt.

Should DSCR Investors Wait After the June Fed Decision?

Waiting makes sense if the numbers do not work, reserves are thin, or the deal only qualifies under optimistic assumptions. But turning “rates might change” into a reason to pass on every property is a different kind of mistake.

In our experience, the files that hold up best in a choppy rate environment share three qualities: rent well above PITIA, conservative leverage, and reserves that give the investor room if the first year runs hard.

Purchase Loans: Underwriting Before You Negotiate

For DSCR purchase loans, the June Fed decision reinforces the need to underwrite the deal before negotiating emotionally.

Investors should review:

Purchase factor | What to check |

|---|---|

Down payment | Whether the investor has enough equity to support loan-to-value and pricing |

Rent support | Whether lease income, market rent, or short-term rental income supports the file |

PITIA | Whether taxes, insurance, and dues are realistic |

Reserves | Whether the investor can absorb vacancy or repairs after closing |

Exit plan | Whether the deal works without assuming a near-term refinance |

A purchase can still make sense after the Fed holds rates. A deal that breaks on a single pricing change was already fragile.

Cash-Out Refinance: Where the Break-Even Math Gets Harder

Cash-out refinance borrowers should be more careful after this meeting.

A cash-out DSCR refinance increases or restructures debt against an investment property. If the borrower uses proceeds for another acquisition, renovation, reserves, or debt consolidation, the strategy may be reasonable. But the new payment still has to be supported by the rental income.

Cash-out refinances are not automatically off the table after this meeting, but the break-even math needs a harder look than it did before June 17.

Before using cash-out proceeds, investors should compare:

- What is the new PITIA?

- How much cash is being pulled out?

- Will the proceeds produce more income?

- What happens if rates do not fall in 2026?

- Are reserves stronger after closing?

Cash-out works best when the investor has a clear use for the capital and the property still supports the new loan after the higher payment.

Paying Points: When It Helps and When It Doesn’t

The June Fed decision also affects the discount point conversation.

When rates feel high, borrowers often ask whether they should pay points to lower the rate. For DSCR investors, the answer depends on the hold period, break-even point, and whether the lower payment meaningfully improves DSCR.

Paying points is weaker when the investor expects to refinance quickly, sell soon, or use cash that would otherwise serve as reserves.

Investors who pay points first and work out the hold plan later sometimes find the loan refinanced or paid off before break-even. Paying for savings the investor never collects is the most common points mistake.

What DSCR Investors Should Do Now

The Fed did not raise rates on June 17, but the meeting was not dovish. The updated dot plot and higher inflation projections both point to a rate environment where DSCR investors need to underwrite more carefully.

The deals that hold up after this Fed meeting share the same profile: rent well above PITIA, adequate reserves, and a loan structure the property can carry at today’s rate.

For investors using Ziffy, the next step is running the property through the numbers and deciding whether the rental income supports the financing before the deal gets serious.