Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Quick Answer

No, you cannot get a DSCR loan with no down payment. A DSCR loan, or debt service coverage ratio loan, is built for investment properties, and every DSCR purchase requires the borrower to bring equity into the deal.

At Ziffy, eligible DSCR purchase files can go up to 85% loan-to-value (LTV), which means a minimum 15% down payment. Many investors should still expect to put down 20% to 25%, depending on the credit score, rental income, property type, reserve strength, and the DSCR the property produces.

The confusion usually comes from how DSCR loans qualify borrowers. A DSCR loan does not use W-2 employment income documents, pay stubs, tax returns, or personal debt-to-income ratio as the core approval path. However, that flexibility does not remove the need for verified capital.

For investors, the more useful question is how much capital the deal actually needs to close cleanly, and how that down payment affects the property’s ratio.

For a broader breakdown of how DSCR loans work, see our DSCR loan guide.

Table of Contents

DSCR Down Payment Requirements at Ziffy

At Ziffy, the minimum down payment for an eligible DSCR purchase can be as low as 15%. On a $300,000 rental property, that means the investor brings at least $45,000 down before closing costs and reserves.

This example shows how a 15% minimum down payment changes based on the purchase price of an investment property. For a $250,000 property, the investor would need at least $37,500 down, while a $500,000 property would require at least $75,000 down. The remaining 85% becomes the estimated loan amount, before closing costs and reserve requirements.

The down payment is separate from closing costs and post-closing reserves. Ziffy typically requires 2 months of liquid cash reserves after closing, which means the borrower needs enough verified funds to cover the down payment, transaction costs, and reserve requirement.

A borrower with exactly 15% down but limited liquidity may still have a harder file than an investor putting down 20% with clean reserves. DSCR loans are rental-income loans, but they are not low-capital loans.

Down payment also affects the debt service coverage ratio directly. DSCR is calculated by dividing rental income by PITIA, which includes principal, interest, taxes, insurance, and association dues. A larger down payment lowers the loan amount, which can lower the monthly payment and improve the ratio.

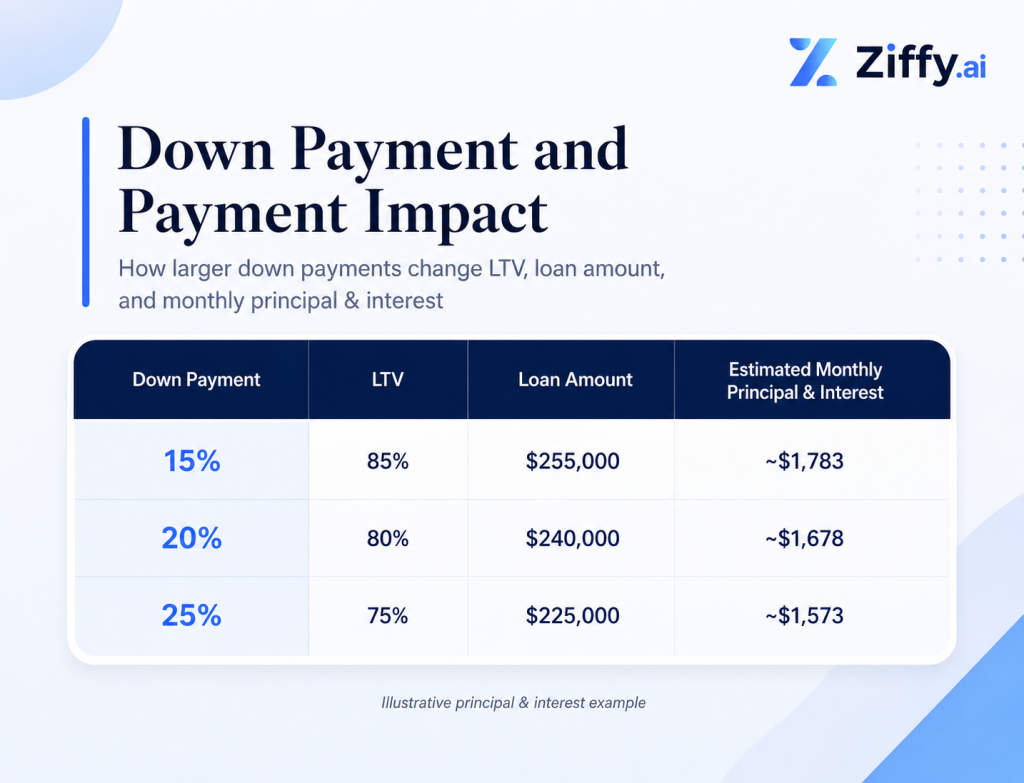

Using a $300,000 purchase price, a 30-year loan term, and a 7.5% illustrative rate, the principal and interest difference looks like this. These figures are examples only and are not quoted loan terms.

This example shows how a larger down payment lowers both the loan amount and the estimated monthly principal and interest payment. On the same purchase scenario, moving from 15% down to 25% down reduces the loan amount from $255,000 to $225,000 and lowers the estimated monthly principal and interest from about $1,783 to about $1,573.

The gap widens once taxes, insurance, and association dues are added to the full PITIA. A property that looks workable at 15% down can become tight after the full PITIA is calculated. A 20% or 25% down payment often gives the file more room, especially in markets where insurance or taxes move quickly.

In our experience, investors often start with the lowest possible down payment because they want to preserve capital for the next property. That strategy can work, but only when the rent comfortably supports the full payment. The files that run into issues are usually the ones where the property barely clears DSCR before the final tax and insurance numbers are added.

What we see often is investors who qualify on the minimum down payment, then realize the full PITIA changes the ratio once taxes and insurance are included. More equity upfront can give the deal room to absorb those adjustments instead of forcing the file to rely on perfect numbers.

For a full look at credit score, reserve, ratio, and property requirements, read our DSCR loan requirements guide.

Why a No-Down DSCR Loan Does Not Exist

A no-down DSCR loan does not fit the structure of property-income lending. With a conventional investment property loan, the lender reviews personal income, tax returns, employment history, and debt-to-income ratio. The borrower’s documented income helps support the payment if the property sits vacant or expenses rise.

A DSCR loan, on the other hand, works differently. The property’s rental income is the primary qualification path, which is why DSCR financing is useful for investors who do not want the loan decision built around personal income documentation. But when the lender is not relying on W-2 income or tax returns, the file has to stand on the property’s rental income, the borrower’s equity, and the reserves available after closing.

The down payment gives the borrower real equity in the asset. It also reduces the loan amount, which can make the property easier to support through rent. Without borrower equity, the file has a weaker risk profile from the start. If the property becomes vacant, insurance increases, or repairs hit early, there is less capital protecting the loan and less borrower exposure to the asset.

That is a structural limit of how property-income lending works, not a gap the market evolved past.

If a property produces a DSCR below 1.0, a No-Ratio DSCR program may still offer a path forward for eligible files, but that does not mean the down payment disappears. In many cases, the opposite happens: the file may need more equity, stronger reserves, or different pricing because the property is not fully covering the payment on paper. For investors comparing a thinner-ratio deal against a stronger one, this distinction matters before they decide how much capital to commit.

How Investors Source the Down Payment Without Draining Reserves

The down payment source matters almost as much as the amount. Underwriting needs to verify where the money came from, whether it belongs to the borrower, and whether it meets program requirements.

Seasoned personal or business funds are usually the cleanest path when documentation is straightforward. Sale proceeds from another property can also work when the closing statement, wire confirmation, and deposit trail are easy to follow. Problems usually appear when large deposits show up late, funds move between accounts without documentation, or borrowed capital is introduced after the file is already in underwriting.

A DSCR cash-out refinance is one of the more practical ways investors fund the next purchase. Ziffy allows eligible DSCR cash-out refinances up to 75% LTV on investment properties. Investors using the BRRRR method, which stands for buy, rehab, rent, refinance, repeat, often use this structure: stabilize one rental, refinance it, season the funds, and redeploy part of the equity into another property.

In our experience, the investors who execute this cleanest are the ones who plan the cash-out at least 60 to 90 days before the next offer. That gives the funds time to season and keeps the reserve trail cleaner when the next file reaches underwriting.

Some investors also use a home equity line of credit on a primary residence. A HELOC can be a valid funding source in certain cases, but it needs to be disclosed early. The balance, monthly obligation, and source of funds may still be reviewed.

Partner equity can work too, but it needs proper structure. If another person is contributing capital, the ownership arrangement, entity documentation, account access, and contribution trail should be reviewed before the file reaches underwriting. Before using a joint venture or co-investor structure, speak with a real estate attorney.

Steven Glick

Director of Mortgage Sales

Ziffy Mortgage

NMLS #1231769The cleanest path I see for investors who want to scale without draining reserves is usually planned equity. They refinance one asset, season the funds, and use that capital for the next purchase. It takes more preparation, but it gives underwriting a much cleaner file.

Run the Numbers Before You Commit Capital

A lower down payment only helps if the property still works after the full monthly cost is included. A higher down payment can improve the file, but it should not leave the investor with too little liquidity after closing.

Before making an offer, compare rent against PITIA at 15%, 20%, and 25% down, and make sure enough cash remains for reserves and early operating costs after closing.

For example, the 146 Bueno Xing listing in Georgetown, KY listed on Ziffy showed an estimated monthly rent of $2,548 against estimated monthly debt service of $1,962, producing a 1.30 DSCR. That kind of cushion gives the file more room than a property sitting close to 1.00.

Investment Properties on Sale Today

A thin ratio does not automatically kill a deal, but it changes the capital conversation. The investor may need more money down, stronger reserves, or a different loan structure. The mistake is treating the minimum down payment as the right down payment before the property’s actual numbers have been tested.

Use the DSCR loan calculator or the cash flow calculator to review the numbers before you commit capital. You can also get pre-qualified to see how your specific property and borrower profile line up with today’s DSCR requirements.

FAQs

Can I get a DSCR loan with no down payment?

No. DSCR loans require a down payment on purchases. At Ziffy, eligible DSCR purchase files can go up to 85% LTV, which means the minimum down payment is 15%. Many files require more depending on the property, credit score, DSCR, reserves, and underwriting review.

Can I get a DSCR loan with 10% down?

No, a 10% down payment creates a higher loan balance, a higher monthly payment, and a thinner DSCR ratio. Once property taxes and insurance are added to PITIA, a file that looked workable at the purchase price can fall below 1.0 before underwriting is complete. If you are looking for a lower-down-payment investment property option and can qualify with personal income documentation, review our guide to investment property loans.

Do reserves count toward the down payment?

No. Reserves are separate from the down payment and closing costs. Ziffy typically requires 2 months of cash reserves after closing, and those funds must still be available after the borrower pays the down payment and transaction costs.

Can I use gift funds for a DSCR down payment?

Gift funds are generally not accepted for DSCR investment property purchases. The down payment and reserves usually need to come from the borrower’s verified funds or another acceptable documented source.

Does No-Ratio DSCR mean I can avoid a down payment?

No. A No-Ratio DSCR option can help eligible investors when the property’s DSCR is below 1.0, but it does not remove the down payment requirement. These files often need stronger equity, reserves, or pricing adjustments because the rental income does not fully cover the payment on paper.