Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

At Ziffy, we look at the short-term rental vs. long-term rental decision through two lenses: what the property can earn and how that income will be reviewed in a debt service coverage ratio loan file.

A short-term rental may show stronger projected revenue, but that income can require more documentation in underwriting. Long-term rent is often easier to support because the income source, either a lease or appraiser-supported market rent, is standardized and directly comparable to the monthly payment.

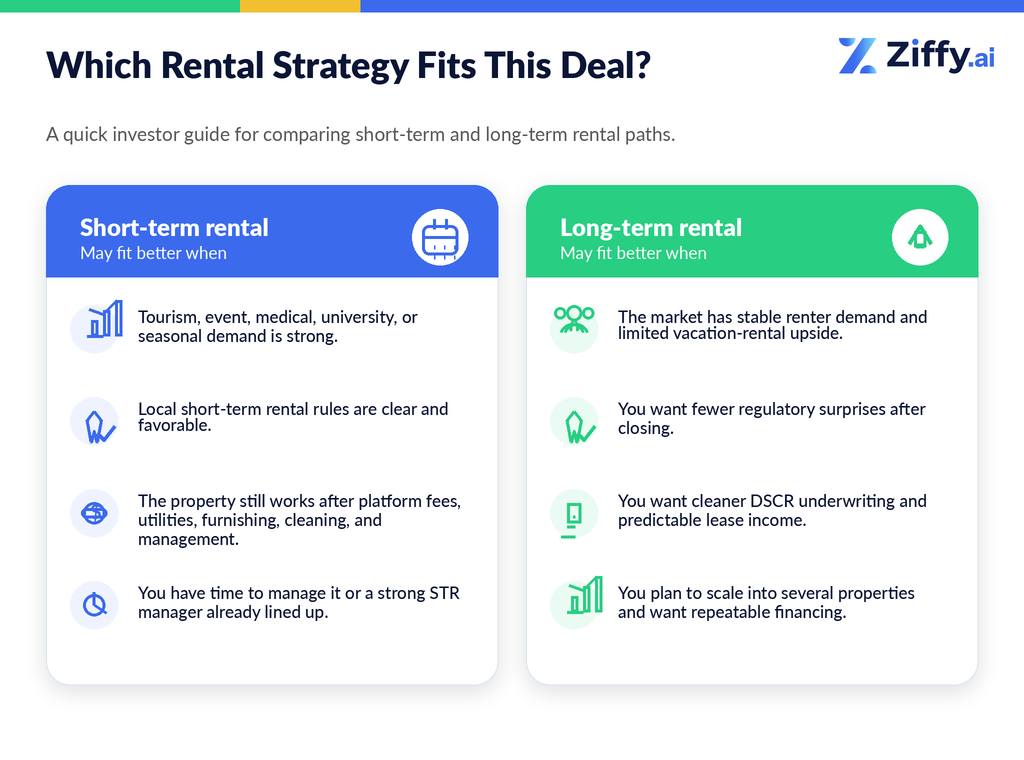

A short-term rental works best when the property is in a strong visitor market, local rules allow the strategy, and the investor is prepared for a higher-management operating model. A long-term rental works better when the investor wants predictable monthly rent, cleaner documentation, and a strategy that is easier to repeat across multiple properties.

On Ziffy, investors can compare estimated rent, cash flow, yield, return on investment, and debt service coverage ratio on live listings before making an offer. That makes the decision property-specific. You are not asking which strategy is better in general. You are asking which strategy works for this property, in this market, with this financing structure.

The scenario section below walks through how those conditions apply to different investor profiles.

- How Short-Term Rental and Long-Term Rental Income Actually Compares

- Ziffy Property Example: Why the DSCR View Changes the Decision

- The Management Reality: What Each Strategy Actually Costs You

- Regulations, Risk, and What Investors Get Wrong About Both

- How STR vs. LTR Affects Your DSCR Loan Qualification

- Scenario-Based Recommendations: Which Model Fits Your Situation

- What If the Strategy Needs to Change After Closing?

- Final Takeaway

- FAQs

How Short-Term Rental and Long-Term Rental Income Actually Compares

Short-term rental income often looks stronger because the gross revenue number is bigger. A property that rents for $2,100 per month as a long-term rental might show $4,000 per month in projected short-term rental revenue in the right market. That spread catches attention fast.

Short-term rental revenue also carries more operating costs, and most of them arrive before any profit is visible. Platform fees, furnishing, cleaning, utilities, supplies, guest turnover, management, and seasonal vacancy all sit between gross revenue and actual cash flow.

Airbnb states that most hosts using the split-fee structure pay a 3% host service fee, although some hosts pay more depending on location and fee structure. Vrbo’s pay-per-booking model includes a 5% commission fee and a 3% payment processing fee in many cases. Those fees come before management, repairs, utilities, and turnover costs are included.

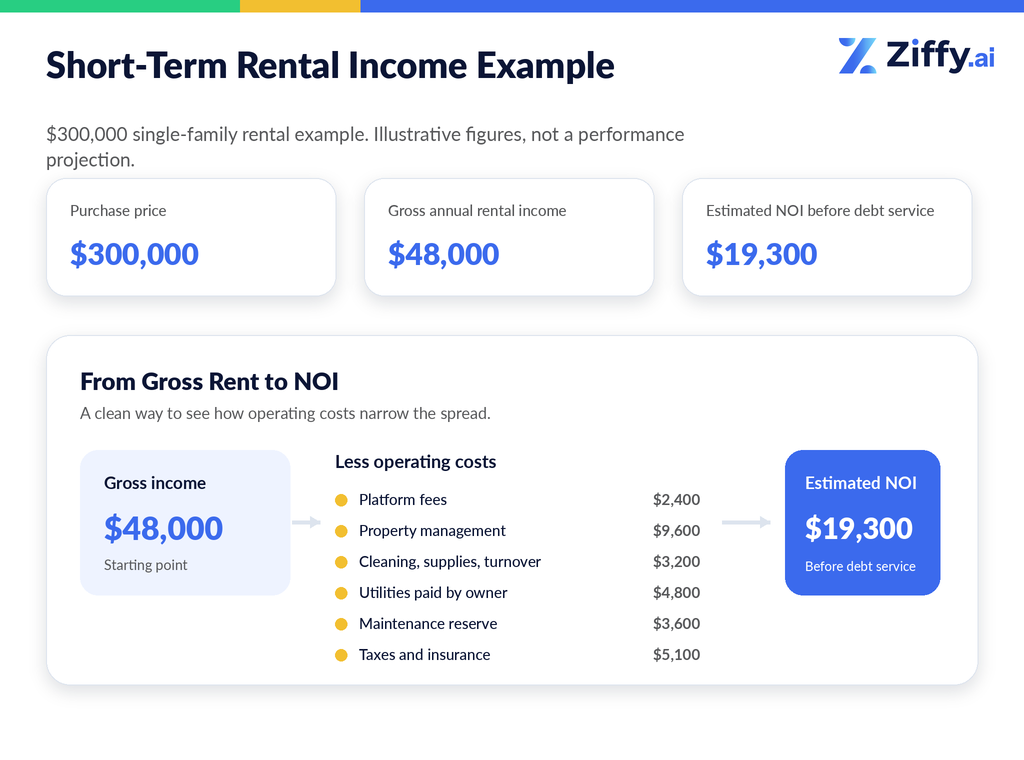

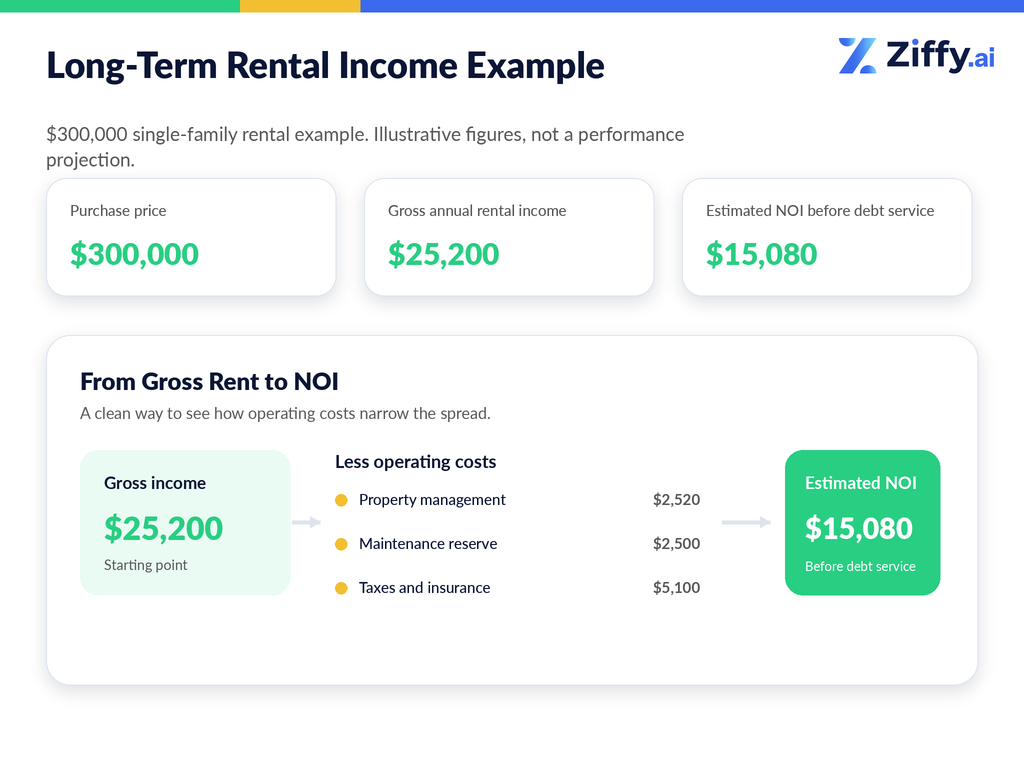

Here is a simple example using the same $300,000 single-family rental in a mid-tier short-term rental market. The numbers are illustrative, not a performance projection.

The short-term rental still produces more net operating income in this example, but the spread is much narrower than the gross rent comparison suggests. The buy-based-on-gross-revenue mistake is the expensive one in short-term rental underwriting. By the time the investor realizes furnishing, management, utilities, and slow months are larger than expected, the offer is already accepted.

Short-term rental management fees are also heavier than long-term rental management fees. AirDNA states that most Airbnb management companies charge between 15% and 25% of rental income, with some fees going higher depending on market and service scope. A 20% management assumption on a $48,000 short-term rental is $9,600 per year. A 10% long-term rental management assumption on $25,200 of rent is $2,520 per year.

On Ziffy, you can pull a live listing and compare projected income, cash flow, yield, return on investment, and debt service coverage ratio before making an offer. The difference between projected short-term rental income and long-term rent is only the first number to stress-test. The better question is what remains after the property is operated like the model actually requires.

Use Ziffy’s Airbnb/STR calculator and cash flow calculator to test the income side of the decision before you move into financing. The calculator shows projected gross revenue, estimated operating costs, and net cash flow side-by-side so you can test whether the STR premium is large enough to justify the extra operating work.

Ziffy Property Example: Why the DSCR View Changes the Decision

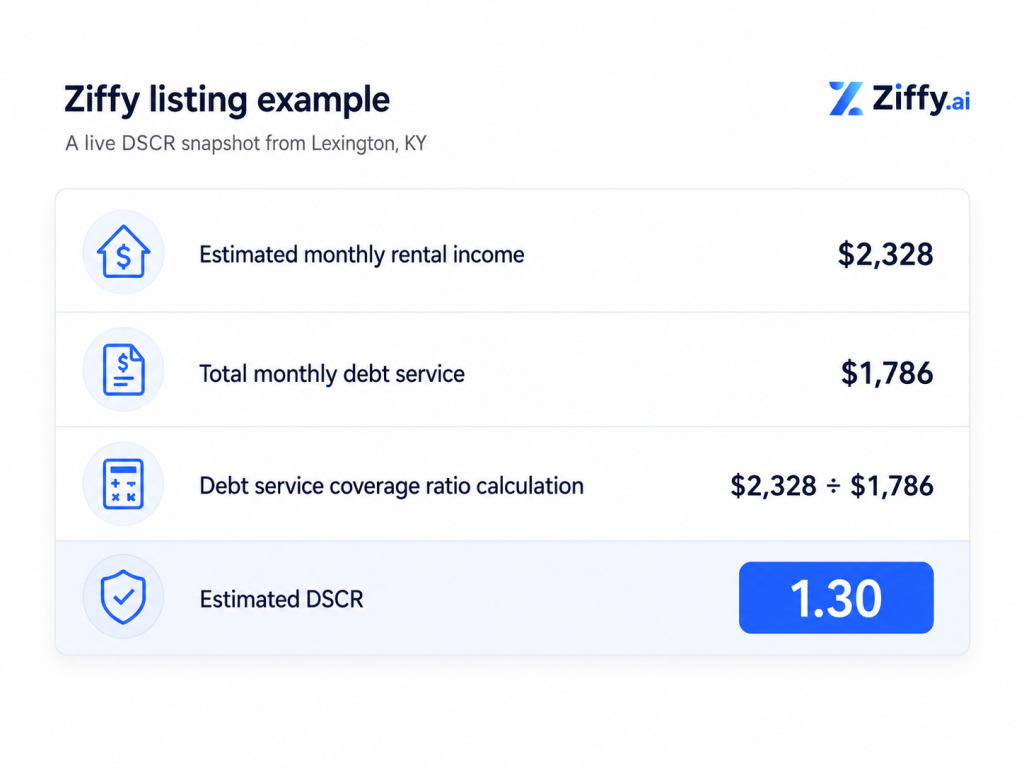

A Ziffy listing for 729 Burgoyne Ct, Lexington, KY, 40505 showed estimated monthly rental income of $2,328, total monthly debt service of $1,786, and a 1.30 debt service coverage ratio. The listing also showed an 8.9% gross yield and 24.53% return on investment, giving investors a cleaner financing view than a revenue-only comparison.

A short-term rental projection that shows higher revenue does not automatically produce a stronger debt service coverage ratio file. The lender still needs to decide which income can be used, how it is documented, and whether the projected revenue needs adjustment.

Reviewing a listing’s projected rent and then discovering mid-underwriting that the income cannot be documented as presented adds time, cost, and risk to a deal that looked clean on paper. Understanding that financing risk early also keeps the management plan realistic, because the operating model and the loan file are not separate decisions.

The Management Reality: What Each Strategy Actually Costs You

Even a good short-term rental needs guest messaging, pricing updates, calendar management, cleaner coordination, platform reviews, supply restocking, maintenance calls, tax tracking, and local rule monitoring. The first year is the heaviest because the investor is still learning pricing, guest expectations, vendor reliability, and the real turnover cost of the property.

A long-term rental runs on a different rhythm altogether: fewer recurring tasks, periodic communication, and operational attention that concentrates around lease-end, maintenance, renewals, and vacancies rather than every guest turnover.

In our experience, the investors who overpay for short-term rentals usually do not miss the revenue estimate. They miss the operating estimate. The projection assumes strong nightly rates, but the actual property needs reliable cleaners, a guest-ready setup, utility coverage, faster maintenance, and enough reserves to absorb slow months. If those numbers are not modeled before the offer, the deal can look stronger than it really is.

Long-term rentals still require discipline. Bad tenant screening, underpriced rent, weak reserves, and poor maintenance planning can all hurt returns. The difference is that the operating model is easier to build on. Each acquisition uses roughly the same income documentation, tenant qualification framework, maintenance response structure, and renewal process. That repeatability is why debt service coverage ratio financing often works more predictably across a portfolio of long-term rentals than across a portfolio of individually managed short-term rentals with different income histories.

Steven Glick,

Director of Mortgage Sales, Ziffy, NMLS#1231769

Regulations, Risk, and What Investors Get Wrong About Both

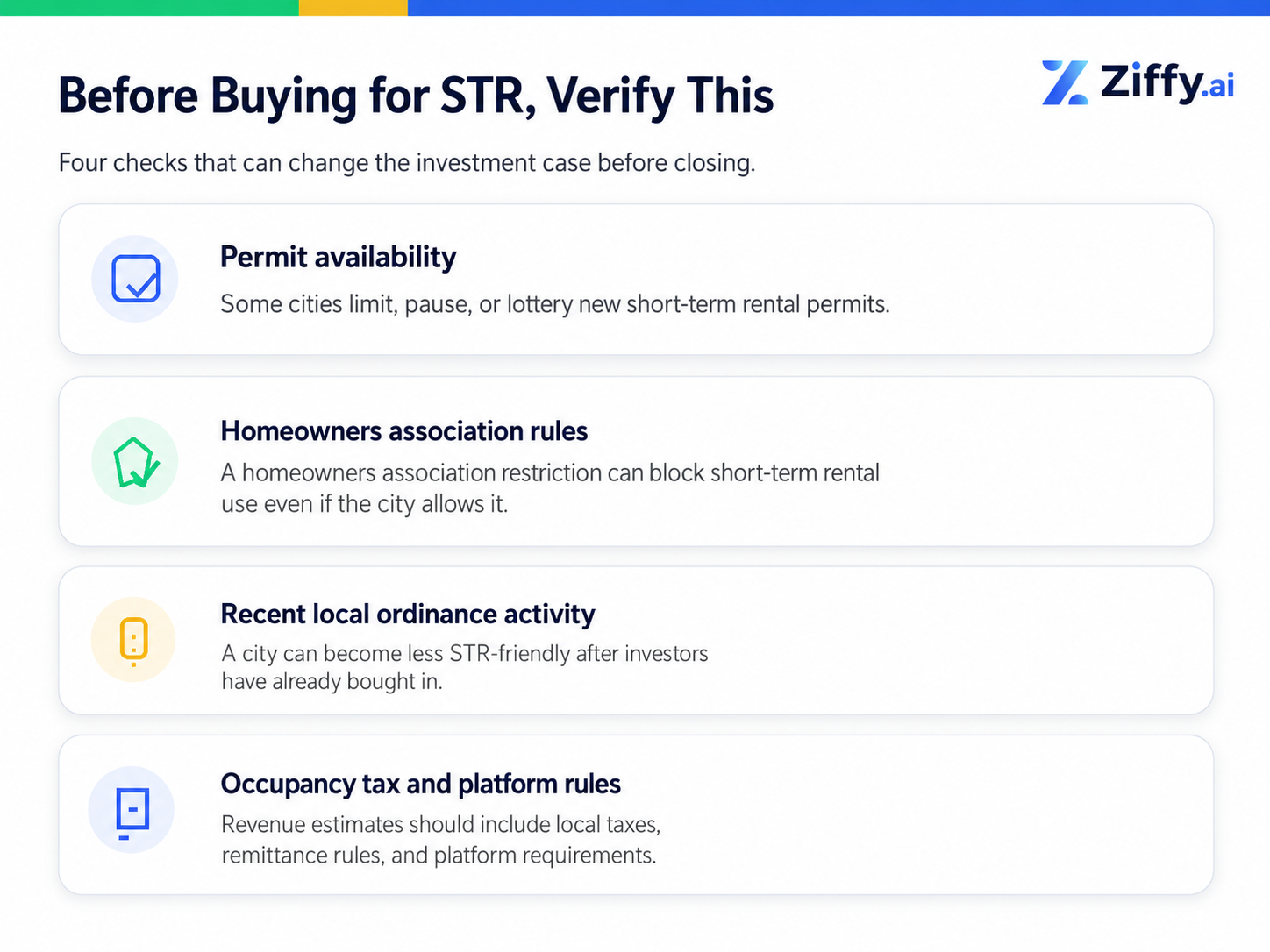

Short-term rental regulations can eliminate the income model before the property even closes. A zoning change, permit denial, or homeowners association restriction mid-ownership does not just reduce returns. It can make the entire acquisition strategy unworkable overnight.

Before buying for short-term rental use, confirm whether the city requires a permit, whether the permit is transferable, whether there is a cap on licenses, whether the homeowners association allows short-term rentals, and whether the local government has recently discussed new restrictions. A market that looks profitable in a calculator can still be a poor purchase if the local rules are unstable.

Long-term rentals carry legal and operational risk too. Investors still need to understand state landlord-tenant law, security deposit rules, eviction timelines, notice requirements, rent control exposure, and local inspection requirements. The difference is that long-term rental demand is tied to the broader housing system, not nightly visitor demand.

In the first quarter of 2026, the Census Bureau reported a 7.3% national rental vacancy rate and a 65.3% homeownership rate, showing that rental housing remains a durable part of the US housing market even when buyer affordability shifts.

STR regulations, zoning rules, occupancy taxes, and homeowners association restrictions vary by municipality. Consult a local real estate attorney before purchasing a short-term rental property.

For market research, start with Ziffy’s top STR markets and short-term rental guide, then verify the rules at the city, county, and homeowners association level before making an offer.

How STR vs. LTR Affects Your DSCR Loan Qualification

A DSCR (debt service coverage ratio) loan is usually the most practical financing path for rental investors because the property’s income can carry the file instead of the borrower having to qualify through traditional personal-income documentation.

At Ziffy, debt service coverage ratio is calculated as gross monthly rent divided by PITIA, which means principal, interest, taxes, insurance, and association dues when applicable. Ziffy Mortgage generally requires a 1.00 or higher debt service coverage ratio for the cleanest file, while some eligible files below 1.00 may be reviewed through a no-ratio DSCR path, where eligible files are evaluated without relying on a minimum coverage ratio requirement.

For a long-term rental, the income path is more standardized. A lender can review a lease, appraiser-supported market rent, or property-specific rent documentation depending on the file. Fannie Mae’s conventional rental-income guidancereferences Form 1007 for one-unit properties and Form 1025 for two-to-four-unit properties where applicable when rental income is used in a subject-property file. In that conventional context, Fannie Mae’s rental-income worksheet applies a 75% factor to gross monthly rent or market rent, with the remaining 25% accounting for vacancy loss, maintenance, and management expenses.

DSCR loans work differently. At Ziffy, the debt service coverage ratio uses gross monthly rent in the numerator without applying the conventional Fannie Mae 75% vacancy factor.

Short-term rental income is treated differently from standard monthly lease rent. Fannie Mae’s June 2024 Appraiser Update says Form 1007 is intended for indicated monthly market rent and cannot be used to estimate the nightly fee for a short-term rental. The update also explains that short-term rental comparables cannot be used to support Form 1007 monthly market rent because the nightly model can include furnishings, services, vacancy, and business expenses that monthly lease rent does not capture the same way.

A long-term rental may qualify using appraiser-supported monthly market rent. A short-term rental may need a different documentation path, such as operating history, platform statements, third-party market data, or a lender-specific short-term rental income review, depending on program rules.

Based on the debt service coverage ratio files our loan team reviews across both rental models, the most common issue on short-term rental files is not always the revenue number itself. It is the absence of support for that revenue at the point when the investor is ready to move.

The investor runs a short-term rental projection, sees a strong income number, and then underwriting asks what can actually be documented. A property that looked like a 1.40 DSCR deal in a short-term rental model may underwrite closer to break-even once the usable income is reviewed, not because the property is a bad investment, but because projected revenue and supportable revenue are not the same number.

Short-term rental income can qualify for DSCR financing. What determines the outcome is how well the income story is built before the file opens.

Steven Glick,

Director of Mortgage Sales, Ziffy, NMLS#1231769

Before you make an offer, knowing whether your income model can be documented is not a small financing detail. It is part of the deal analysis. Ziffy Mortgage is licensed in 48 states, and our investor-focused loan team works with both short-term and long-term rental scenarios.

Use Ziffy’s DSCR calculator before you apply. If the long-term rent already supports the file, the property has a stronger baseline. If the short-term rental projection is the reason the deal works, speak with a Ziffy loan officer before making the offer so the documentation path is clear upfront.

Scenario-Based Recommendations: Which Model Fits Your Situation

The right rental model depends on which investor situation applies to you, not just which rent estimate looks higher.

For a first-time investor in a market without strong visitor demand, the long-term rental path removes two variables at once: management complexity and documentation friction. The projected rent may be lower, but the property can be evaluated against nearby lease comps, and the debt service coverage ratio file is easier to understand before the offer.

An experienced investor buying in a high-demand vacation market can be a strong short-term rental candidate, especially if the property has existing booking history or the investor already has a property manager lined up. In that situation, the income upside can justify the heavier operations. The file still needs proper short-term rental documentation, but an experienced operator is less likely to underestimate expenses.

For an investor trying to scale to five or more properties, long-term rentals deserve serious weight. The rent is easier to document, the appraisal methodology is more standardized, and the file does not depend on booking history that may not exist yet. A portfolio grows faster when each new acquisition does not require a completely new income story.

Regulatory risk is the scenario where the short-term rental vs. long-term rental decision gets made for you. If the permit path is uncertain or the local rules have recently shifted, the deal should be underwritten on long-term rent from the start. Buying a property that only works as an STR in a city that is actively restricting them is a regulatory bet with real downside.

Converting a primary home into a rental is a different decision than buying a purpose-built investment property. Start with two questions: does the market have enough visitor demand to justify the short-term rental operating model, and does the homeowners association permit it? A home in a suburban neighborhood with no visitor traffic and a restrictive homeowners association has one realistic rental strategy.

Dorian Adams-Walker,

Mortgage Loan Originator, Ziffy, NMLS#2442830

Run both models on the same property before the offer. On Ziffy, that means reviewing projected income, cash flow, return on investment, yield, and debt service coverage ratio on the listing before using that baseline in the financing conversation. A strong short-term rental projection is useful, but the next step is confirming how that income will be reviewed in underwriting.

For investors planning to scale with DSCR financing, our investment property loans guide explains how financing options differ across rental strategies. Our buy-and-hold strategy guide is useful if the long-term plan is to build a repeatable rental portfolio instead of buying one isolated property.

What If the Strategy Needs to Change After Closing?

Converting a long-term rental to short-term rental is possible, but the path has more steps than most investors expect. You need to check city permits, county rules, homeowners association restrictions, insurance coverage, furnishing costs, occupancy tax requirements, platform setup, and local enforcement risk.

Converting a short-term rental into a long-term rental is simpler operationally. You remove the guest-turnover model, sign a lease, and shift to monthly rent. The financing question returns if you later refinance or pursue a cash-out refinance. At that point, the lender may recalculate income based on the current rental model.

Mixed portfolios are also common. An investor may hold long-term rentals for steady baseline income and add a short-term rental in a market with stronger visitor demand. That structure can work, but each property still needs to support its own financing story. The long-term rentals may have cleaner lease-based documentation, while the short-term rental may need stronger operating history or additional income support.

Do not buy a property that only works under one rental strategy unless you are confident that strategy is allowed, financeable, and durable. A stronger acquisition has a primary plan and a backup income path. If the short-term rental plan gets blocked by local rules, the long-term rent should still tell a reasonable story.

Steven Glick,

Director of Mortgage Sales, Ziffy, NMLS#1231769

If your rental strategy shifts after closing, or you want to refinance into better terms, talk to us. We review the income model change as part of the file so you understand how it affects your debt service coverage ratio before you apply.

Final Takeaway

Short-term rentals can work well when the market supports nightly demand, local rules are stable, operations are properly resourced, and the income can be documented in underwriting. Long-term rentals usually give investors a cleaner path when the goal is steady rent and repeatable debt service coverage ratio financing.

Before you make an offer on either type of property, compare both income models on the same listing. Then speak with a loan officer about how that income will be read in underwriting. At Ziffy, those two steps happen in the same conversation.

FAQs

Which makes more money: short-term rental or long-term rental?

Short-term rentals often generate higher gross income, especially in tourism, event, beach, mountain, university, and medical-travel markets. Long-term rentals usually have lower gross income but steadier occupancy, fewer operating expenses, and simpler management. Investors should compare net cash flow after expenses, not gross rent.

Is short-term rental income harder to qualify for a DSCR loan?

Yes, short-term rental income can be harder to document than long-term rental income. A long-term rental file can often rely on a lease or appraiser-supported monthly market rent. A short-term rental file may require booking history, platform statements, third-party market data, or additional lender review, depending on program rules.

Do I need a separate loan for a short-term rental property?

Not necessarily. Eligible short-term rental properties may qualify for a debt service coverage ratio loan, depending on the property, borrower, state, documentation, and income support. At Ziffy, we review the rental strategy as part of the financing conversation so investors understand the documentation path before moving forward.

Can I finance a short-term rental if the property has no rental history?

It may be possible, but a new short-term rental with no booking history needs a careful review before offer. The lender may need appraiser-supported rent, third-party market data, or other documentation depending on the loan program. Investors should speak with a loan officer before buying a property that only works if projected short-term rental income is accepted.

What markets work best for short-term rentals?

Short-term rentals usually work best in markets with durable visitor demand, clear local rules, favorable permit access, and enough nightly-rate strength to cover management, utilities, cleaning, furnishing, and vacancy. A profitable STR market is not just a place where travelers visit. It is a place where the rules, revenue, expenses, and financing can work together.

What markets work best for long-term rentals?

Long-term rentals usually work best in markets with stable employment, renter demand, reasonable price-to-rent ratios, and manageable insurance, tax, and maintenance costs. Investors planning to scale often prefer long-term rentals because lease income is usually easier to document in debt service coverage ratio underwriting.

Is long-term rental better for scaling a rental portfolio?

Long-term rentals often create a cleaner path for scaling a rental portfolio because the income is easier to document and the management burden is lower. That matters when an investor wants to use debt service coverage ratio loans to finance multiple properties.

Can I switch my short-term rental to a long-term rental if regulations change?

Usually, yes, assuming the property can attract a long-term tenant at rent that still supports the investment. Before buying a short-term rental, investors should test the long-term rental backup plan. If the property only works as a short-term rental, local regulation becomes a major underwriting risk.