Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Most short-term rental hosts do not find out their insurance is wrong for the property until something happens. A homeowner’s policy can sit in place through dozens of guest stays, multiple peak seasons, and thousands of dollars in bookings without raising a question. Then a guest gets injured, a damage claim is filed, or the carrier asks how the property was being used, and the host learns that the policy was never built for nightly rental activity.

That gap becomes a financing problem when the property is being purchased with a loan.

At Ziffy, we review insurance before closing because the policy has to match the way the property will actually be used. A standard homeowner’s policy, an Airbnb AirCover screenshot, or a Vrbo protection confirmation does not satisfy the insurance requirement for a financed Airbnb or Vrbo investment property. We need a real policy binder from a licensed carrier, with the property address, coverage limits, policy period, and mortgagee clause clearly shown.

The National Association of Insurance Commissioners warns that most homeowners or dwelling policies are not designed to cover accidents tied to short-term rentals, even when the policy does not spell out every possible rental exclusion. For investors, this is not just a claims issue. Insurance affects closing conditions, monthly PITIA, DSCR, and the property’s actual cash flow after the loan is funded.

If you are using a DSCR loan to finance an Airbnb or Vrbo property, insurance needs to be handled early in the deal. The policy has to protect the asset, satisfy underwriting, and still leave enough rental income to support the loan.

Table of Contents

Why Your Homeowner’s Policy Can Fail Once You List on Airbnb

A homeowner’s policy is usually written for personal residential use. Short-term rental activity changes the risk because the property is being used to generate income from rotating guests. A carrier looks at that very differently from a home occupied by the owner or a long-term tenant.

Many standard policies contain language around business use, commercial activity, rental activity, or transient occupancy. The wording varies by carrier and state, but the concern is the same. A property that turns over every few nights has more unknowns. Guests may bring additional people, use amenities differently, damage furniture, create noise complaints, or get injured during a paid stay. The policy has to be written for that use.

Carriers usually do not need a complicated investigation to discover short-term rental activity. Public Airbnb and Vrbo listings, guest reviews, booking records, local permit registrations, neighbor complaints, social media posts, and claim details can all point to how the property was being used. Assuming the carrier will never find out is a bet against the first serious claim, and the first serious claim is usually when the carrier starts asking the hardest questions.

What we see often is an investor who has hosted for a year or more under a standard homeowner’s policy without a problem. They assume that because nothing has gone wrong, the policy must be fine. In reality, the policy simply has not been tested yet.

Lucas Hernandez

Mortgage Loan Originator

Ziffy Mortgage

NMLS #2171747The absence of a claim is not proof of coverage. A lot of short-term rental investors only discover the gap after the carrier reviews how the property was actually being used. By that point, it is no longer a paperwork issue. It can become a denied claim, a delayed closing, or both.

There is also the risk of cancellation or non-renewal if the carrier determines that the property use was not disclosed correctly. Whether a claim is denied, limited, or handled differently depends on the policy, the state, and the facts, but the safest approach is simple: tell the carrier how the property will be used and buy coverage that is actually written for short-term rental activity.

What Airbnb and Vrbo Host Protection Actually Covers

Airbnb and Vrbo both offer built-in host protection programs, and those programs can be helpful. The problem starts when investors treat them like full property insurance.

Airbnb AirCover and Vrbo’s liability protection are tied to the platform and its program terms. A financed investment property needs insurance that follows the property through Airbnb bookings, Vrbo bookings, direct bookings, vacant periods, owner stays, cleaning turnover, maintenance access, and the normal gaps that come with operating a rental.

Airbnb AirCover for Hosts

Airbnb AirCover for Hosts includes $3 million in host damage protection and $1 million in host liability insurance. Airbnb’s host damage protection can reimburse hosts for certain guest-caused damage to the home, belongings, parked vehicles, extra cleaning, and lost income from canceled Airbnb bookings caused by guest damage.

The liability side is separate. Airbnb’s host liability insurance is designed for situations where the host is found legally responsible for certain guest injury or property damage claims during an Airbnb stay.

Those protections can matter, but they do not replace a lender-accepted property insurance policy. A lender is not looking for a platform protection page. The lender needs a policy binder from a licensed carrier showing the subject property, the coverage amounts, the policy period, and the lender’s mortgagee clause.

The clean way to think about it is this: AirCover follows the Airbnb booking. Property insurance follows the property. A financed investment property needs the second one.

Vrbo’s Liability Insurance

Vrbo’s $1 million liability insurance program gives added protection for eligible reservations processed online through Vrbo checkout, and Vrbo says the program works with the owner’s current liability policy.

That last part is the detail investors should pay attention to. Vrbo protection can supplement coverage, but it does not replace a standalone short-term rental insurance policy. It also does not give a DSCR lender the binder it needs before closing.

For an investor, the practical answer is not to ignore Airbnb AirCover or Vrbo protection. Keep them in place, understand what they do, and treat them as supplemental. Your primary protection should still come from a real short-term rental or vacation rental policy that matches the property’s use.

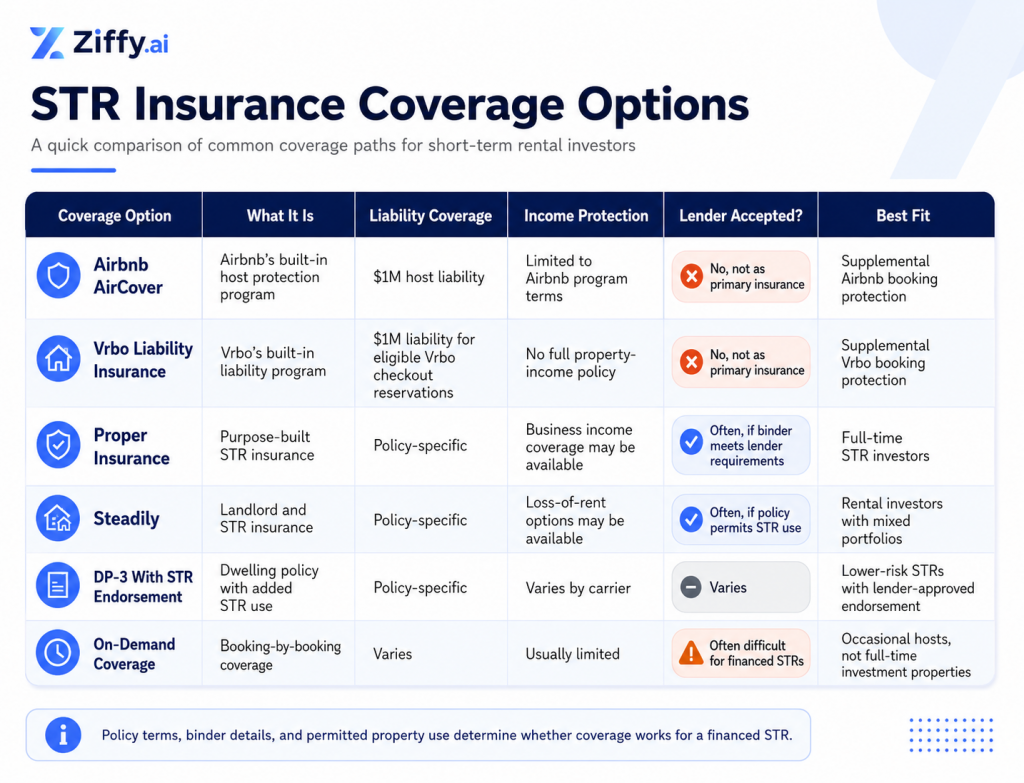

STR-Specific Insurance: The Policies That Actually Work

Short-term rental insurance, also called vacation rental insurance or STR insurance, is built for properties used as paid lodging. A properly structured policy should account for guest stays, owner stays, vacant periods, cleaning turnover, maintenance access, direct bookings, and income loss if a covered event takes the property offline.

There is no single policy structure that works for every property. The right answer depends on the location, guest capacity, amenities, carrier appetite, and how often the property will be rented. From a lending perspective, the binder has to show that the property is covered for the use being underwritten.

Proper Insurance

Proper Insurance is one of the best-known providers in the short-term rental space, and its policies are built around vacation rental use rather than standard owner occupancy. For a full-time Airbnb or Vrbo investment property, this type of structure is often cleaner for underwriting because the policy is not trying to stretch a homeowner’s form into a business-use situation.

Vrbo’s own host guidance identifies Proper Insurance as a comprehensive vacation rental option, which is useful context for why purpose-built STR coverage is not interchangeable with a standard homeowner’s policy.

Steadily

Steadily offers landlord and short-term rental insurance for rental property owners and investors. This can make sense for investors who own different types of rentals, such as one long-term rental, one mid-term rental, and one Airbnb property.

The policy still needs to match the use of the specific property being financed. A long-term rental policy with no short-term rental endorsement is not the same as coverage written for nightly or weekly stays.

DP-3 With Short-Term Rental Endorsement

A DP-3 is a dwelling policy commonly used for non-owner-occupied homes. On its own, it may not be enough for short-term rental use. The endorsement is the part that matters because it tells the carrier and the lender that short-term rental activity is permitted under the policy.

A DP-3 with a clear STR endorsement can work in some files if the endorsement allows Airbnb, Vrbo, and direct bookings; covers guest injury claims tied to rental use; includes property damage and loss-of-rents coverage where available; permits the lender’s mortgagee clause; and addresses higher-risk amenities such as pools, hot tubs, decks, fire pits, or docks.

When the agent or carrier gives vague answers to those questions, the policy is not ready for underwriting.

Booking-by-Booking or On-Demand Coverage

On-demand coverage can work for someone who rents a guest room or second home a few weekends a year. It is much harder to use for a financed investment property because the lender needs evidence of insurance that covers the collateral at closing and remains in force after closing.

A booking-by-booking policy may not give the lender the annual structure it needs. For a full-time Airbnb or Vrbo investment, it is usually better to start with a policy designed for short-term rental use and then review whether any platform protection or supplemental coverage adds value.

Short-Term Rental Insurance Comparison

How STR Insurance Affects Your DSCR Loan

Short-term rental insurance belongs near the front of the financing conversation because insurance is part of the monthly housing cost used in underwriting.

For an investment property, Debt Service Coverage Ratio (DSCR) compares qualifying rental income to the property’s monthly debt and operating obligations. At Ziffy, the monthly expense review includes principal, interest, taxes, insurance, and association dues, commonly called PITIA.

Insurance is not a line item to clean up after underwriting, but a part of the underwriting math.

What the Lender Reviews Before Closing

A lender requires proof of insurance before closing because the property is the collateral for the loan. If the property is damaged after closing, the lender needs to know the asset is properly protected.

For a short-term rental, the binder needs to do more than show that some policy exists. It should identify the property address, named insured, mortgagee clause, dwelling coverage, liability coverage, deductible, carrier, effective date, expiration date, and policy period covering the closing date. The file also needs to show that short-term rental use is allowed.

A pattern we have noticed is that investors who line up STR-rated insurance during the offer period tend to move through underwriting more cleanly than those who wait until the lender asks for it. The delay is rarely caused by the quote itself. The issue usually starts when the first binder comes back as a homeowner’s policy, underwriting sends it back, and the borrower has to restart the conversation with the carrier.

Lucas Hernandez

Mortgage Loan Originator

Ziffy Mortgage

NMLS #2171747At the insurance step in a short-term rental file, the thing that slows deals down is usually not the loan structure. It is the wrong insurance document. We need a policy binder from a licensed carrier that shows the property address, coverage amounts, mortgagee clause, and policy period. Getting that sourced in week one instead of week three keeps the file moving.

How Insurance Cost Can Change DSCR

For short-term rental DSCR underwriting, Ziffy uses a conservative income approach that accounts for vacancy and seasonality. If a property is projected to generate $6,000 per month in gross short-term rental income, the underwriting income may be reduced before it is compared against the monthly payment.

Here is a simplified example:

- Gross projected STR income: $6,000/month

- Underwritten income at 75%: $4,500/month

- Principal and interest: $3,000/month

- Property taxes: $600/month

- Association dues: $100/month

Now look at what happens when the insurance quote changes.

Insurance Scenario | Monthly PITIA | DSCR |

|---|---|---|

Insurance at $250/month | $3,950 | 1.14 |

Insurance at $550/month | $4,250 | 1.06 |

Insurance at $850/month | $4,550 | 0.99 |

The rent, purchase price, and loan assumption stayed the same, only the insurance premium moved the file from comfortable to borderline.

This is why insurance should be part of the deal analysis before the offer goes out. When you use the Ziffy Airbnb and STR Calculator, build in a realistic insurance estimate alongside projected Airbnb revenue, cleaning fees, occupancy, taxes, association dues, and financing costs. You can also compare the same property through the DSCR Loan Calculator to see how different insurance quotes affect the qualifying ratio.

What Coverage Limits Should STR Investors Carry?

The right coverage limit depends on the property, state, carrier, guest capacity, amenities, local rules, and loan requirements. A licensed insurance agent should review the final policy, but investors should understand the main coverage areas before they start comparing quotes.

Liability coverage is usually the first question. Many hosts start with $1 million because that number appears in both Airbnb and Vrbo platform protection programs, but the right amount depends on the property. A condo that sleeps two guests does not carry the same liability profile as a cabin that sleeps twelve guests and has a hot tub, dock, fire pit, and elevated deck.

Steven Glick

Director of Mortgage Sales · Ziffy Mortgage

The mistake I see is treating insurance as a yes-or-no question: does the property have coverage? The real question is whether the coverage matches how the investor plans to operate. A twelve-guest cabin with a hot tub and a dock is not the same liability file as a duplex with two tenants on annual leases, and the premium should reflect that.

Dwelling coverage should also be reviewed carefully because replacement cost is not the same as purchase price. A property may sell for $450,000, but the cost to rebuild the structure after a covered loss could be higher or lower depending on labor, materials, code requirements, location, and property type. Land value, appreciation, and investor demand can push purchase price away from the actual rebuild cost.

Short-term rental investors should also ask about business income or loss-of-rents coverage. If a covered event takes the property offline during peak season, the repair bill may only be part of the loss. The missing rental income can be just as painful, especially in markets where a few strong months carry the year.

Umbrella coverage becomes more relevant as the property gets larger, guest count increases, or the investor grows into multiple rentals. Some investors add $1 million to $5 million above the primary policy, depending on the carrier and the property’s risk profile.

Amenities deserve their own conversation with the insurance agent. Pools, hot tubs, trampolines, fire pits, docks, boats, bicycles, golf carts, decks, and outdoor stairs can help revenue, but they can also increase premiums or create exclusions. A hot tub may raise nightly rates, but that extra revenue has to hold up after insurance, cleaning, maintenance, liability exposure, and financing costs are included.

Use Ziffy’s guide to analyzing a short-term rental before assuming an amenity improves the deal. The revenue premium only helps if the property still works after the full operating cost is included.

What Platform Protection Does Not Solve

Airbnb and Vrbo protection programs can be useful, but they do not solve the main insurance questions a financed investor has to answer.

They do not replace year-round property coverage, direct-booking exposure, vacant-period coverage, owner-stay coverage, replacement-cost dwelling coverage, mortgagee clause requirements, policy binder requirements, local permit insurance rules, business income protection across all channels, amenity-specific underwriting, or umbrella liability planning.

Airbnb AirCover follows Airbnb’s program terms. Vrbo’s liability program follows Vrbo’s program terms. Your investment property needs insurance that follows the property.

Once an investor owns more than one short-term rental, the insurance program is no longer about one binder. It becomes part of the operating model alongside financing, tax planning, and portfolio risk control.

How to Prepare Your Insurance Before Applying for an Airbnb Loan

The best time to solve insurance is before the loan file is under pressure. If you wait until underwriting asks for the binder, a simple issue can turn into a closing delay.

Before you submit an offer or apply for financing, ask an insurance agent for a short-term rental quote based on the property’s actual use. Do not request a standard homeowner’s quote if the property will operate as an Airbnb or Vrbo rental. Tell the agent how the property will be used, how many guests it will sleep, whether you plan to allow direct bookings, whether you will use the property personally, whether the property will be held in a limited liability company, and whether the property has amenities such as a pool, hot tub, deck, dock, fire pit, or other higher-risk features.

The agent should also know if the local market has permit or registration requirements. Some cities and counties have insurance rules tied to short-term rental licensing, and those requirements should be addressed before the binder is issued.

What we see often is the same conversation in week three of a file: the borrower forwards an AirCover confirmation, underwriting rejects it, and now the carrier has to issue a new binder before closing can move. The delay almost always traces back to documentation, not the loan structure.

The cleanest STR files start with the investor treating insurance like part of the acquisition analysis, not a closing-week task. If the quote is higher than expected, we need to know early because it can change DSCR, reserves, and the final loan conversation.

If you are using Ziffy for an Airbnb loan, bring the insurance estimate into the loan conversation early. We can help you see how the premium affects projected DSCR and whether the property still supports the financing structure you want.

Next Steps

Short-term rental insurance protects the investment, but it also shapes the loan math.

If projected Airbnb or Vrbo income supports the payment after taxes, insurance, association dues, and seasonality adjustments, a DSCR loan can be a strong financing path. If the insurance quote pushes DSCR too low, you want to know that before the file is deep into underwriting.

Ziffy helps investors look at both sides of the deal: the income potential of the property and the financing structure needed to close.

Start with an Airbnb/STR loan quote, run the numbers through the Airbnb and STR Calculator, and review the full short-term rental investing guide before moving forward.

FAQs

Is Airbnb AirCover the same as landlord insurance?

No. Airbnb AirCover is Airbnb’s built-in host protection program. It includes host damage protection and host liability insurance, but it is not the same as a standalone short-term rental insurance policy.

Landlord insurance or short-term rental insurance is issued by an insurance carrier. For a financed Airbnb property, the lender will usually require a policy binder from a licensed carrier, not an AirCover confirmation.

Do I need STR insurance if I only rent occasionally?

You should speak with your insurance agent before accepting paid guest stays. Some carriers offer limited occasional-rental endorsements, but many standard homeowner’s policies exclude or limit business or rental activity.

Occasional hosting and full-time short-term rental investing are not the same insurance problem. A property operated as a year-round Airbnb or Vrbo investment needs coverage that matches that use.

Will my DSCR lender accept my existing homeowner’s policy?

Usually not if the property is being used as a short-term rental. The lender needs coverage that matches the property’s intended use. A homeowner’s policy is generally designed for owner occupancy, not nightly rental activity.

How much does short-term rental insurance cost?

Cost varies by location, replacement cost, claim history, carrier, guest capacity, amenities, wildfire or storm exposure, liability limits, and income coverage. A cabin with a hot tub in a seasonal mountain market may price very differently from a condo in an urban market.

For investment analysis, use a real quote whenever possible. A rough estimate can make the DSCR look stronger than it really is.

Can I deduct STR insurance premiums?

IRS Publication 527 lists insurance as one of the expenses that may be deductible for rental property, although personal use, prepaid insurance, mixed use, and substantial services can change the tax treatment. Investors should work with a qualified tax professional before deciding how to report rental income, insurance premiums, depreciation, or related expenses.

Foreign investors have additional tax considerations, including the Foreign Investment in Real Property Tax Act (FIRPTA), withholding rules, and treaty-related questions. That is outside the scope of this insurance guide.

Can you guarantee STR insurance will be accepted by underwriting?

We can tell you what the lender needs to see: a licensed carrier, named insured, mortgagee clause, adequate dwelling and liability limits, policy period covering the closing date, and coverage that matches short-term rental use. However, the final approval is still on underwriting, not the loan officer.

A binder showing owner-occupied coverage or a platform confirmation in place of carrier coverage will not work for a financed Airbnb or Vrbo investment property.

Does Ziffy require STR-specific insurance to close an Airbnb loan?

Ziffy requires insurance that matches the property use and satisfies lender requirements. For an Airbnb or Vrbo investment property, platform protection alone is not enough. We need a policy binder from a licensed carrier showing the property address, coverage amounts, policy period, and lender-required details.

Can I use Vrbo’s $1 million liability coverage as my main insurance?

No. Vrbo’s liability program may provide certain protection for eligible claims, but it is not a full property insurance policy. Vrbo states that its $1 million liability program works with the owner’s current liability policy and applies to eligible reservations processed through Vrbo checkout.

What should I do before buying a short-term rental?

Run the numbers with realistic insurance, taxes, utilities, cleaning, maintenance, management, and financing costs. Start with Ziffy’s short-term rental investing guide, then use the Airbnb and STR Calculator to test the deal before making an offer.