A Chicago real estate investor used a DSCR cash-out refinance to move from short-term hard money debt into longer-term rental financing after completing a rehab-to-rent project.

The borrower vested through an LLC and purchased a single-family rental in Chicago, IL for $145,000. The acquisition was funded with a hard money loan, which helped the investor move through the purchase and rehab phase.

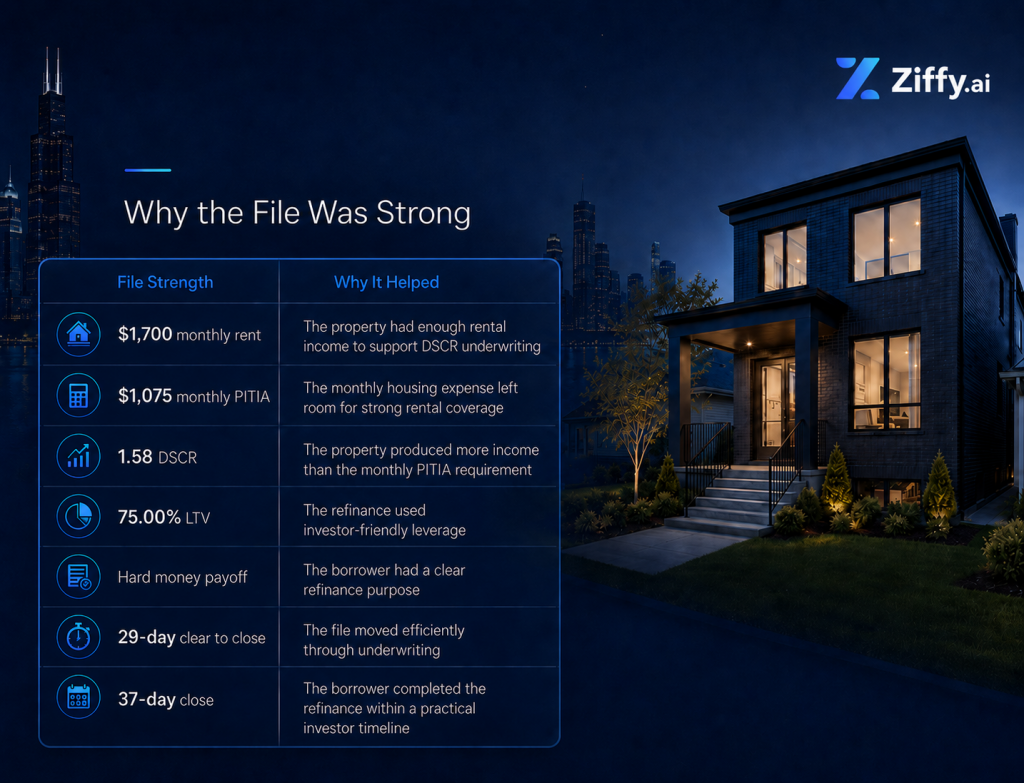

Once the property was ready for rental use, the borrower refinanced with a DSCR cash-out refinance. The new loan helped pay off the original hard money debt, supported by $1,700 in monthly rent, $1,075 in monthly PITIA, and a strong 1.58 DSCR.

The file reached clear to close in 29 days and closed in 37 days.

Table of Contents

Investment Highlights

Loan Details

Approved loan amount: $123,750

Loan type: Cash-out refinance

DSCR: 1.58

LTV: 75.00%

Property Details

Property address: Chicago, IL 60628

Property type: Single Family Rental

Purchase price: $145,000

The Investor’s Situation

The borrower was a domestic investor entity that had already completed the first part of the strategy: buying a Chicago single-family residence with hard money financing and preparing it for rental use.

That type of capital can be useful during the acquisition and rehab stage. It gives investors room to buy, improve, and stabilize a property before moving into a longer-term loan structure. But once the property is rent-ready, hard money is usually not where investors want to stay.

This file was about the next step in this journey.

The investor needed a refinance path that matched the property’s rental use, supported the payoff of the existing hard money loan, and allowed the borrower to continue holding the asset as an income-producing rental. The property’s rent made that possible.

Why the DSCR Refinance Worked

The property generated $1,700 in monthly rent against $1,075 in monthly PITIA. That produced a 1.58 DSCR, which gave the file strong rental-income coverage.

The DSCR calculation was straightforward:

$1,700 monthly rent ÷ $1,075 monthly PITIA = 1.58 DSCR

For investors, that spread is meaningful. The property was not barely covering the monthly housing expense used in underwriting. It produced enough rental income to show a stronger cushion between rent and PITIA.

In this file, the rental income was about 58% higher than the monthly PITIA payment used for the DSCR calculation.

That helped support the refinance request and gave the file a cleaner path through underwriting.

Loan Structure

The borrower completed a DSCR cash-out refinance with a $123,750 loan amount.

The loan was structured at 75.00% LTV with a 6.625% interest rate. Based on the provided LTV and loan amount, the refinance valuation used for the transaction was approximately $165,000.

That is important because the original purchase price was $145,000, but a refinance is structured around the valuation and underwriting terms used for the refinance transaction. In this case, the new loan helped the investor move out of the original hard money position after the property had been prepared for rental use.

The Refinance Outcome

The DSCR cash-out refinance helped the borrower pay off the hard money loan used for the purchase and rehab phase. That made the deal a clear rehab-to-rent refinance case study:

The investor bought the property with hard money, completed the rehab, positioned the home as a rental, documented monthly rent, and then refinanced into a DSCR loan supported by the property’s income.

The file reached clear to close in 29 days and closed in 37 days.

For a rental investor, that timing matters. A hard money payoff often has urgency because the original loan is not designed to sit on the property forever. The faster the refinance moves, the sooner the borrower can settle into a financing structure that better matches the rental hold strategy.

Dorian Adams-Walker

Mortgage Loan Originator, Ziffy Mortgage

This file shows how DSCR financing can support an investor after the rehab work is done and the property is producing rent. The borrower used hard money for the front end of the project, then refinanced once the rental income could support the new loan. A 1.58 DSCR gave the file strong rental coverage.

What Made This File Strong

The strongest part of this file was the property’s rental coverage. A 1.58 DSCR showed that the rent was comfortably above the monthly PITIA used in underwriting. For a cash-out refinance, that helped support the overall file because the property had enough income to carry the debt.

The deal also had a clear investor purpose. The borrower was not refinancing without a strategy. The refinance solved a specific problem: paying off hard money after the property had moved from rehab stage to rental stage.

Why This Matters for Rental Investors

Hard money and DSCR financing serve different jobs.

Hard money can help investors acquire and rehab a property when speed or property condition matters. DSCR financing is better suited for the rental phase, when the property is stabilized and producing income.

The borrower used hard money to get the project started. Once the property had rental income, the DSCR refinance helped convert the deal into a longer-term rental hold.

For investors building a rental portfolio, this type of refinance can be useful because it allows the property’s income to play a central role in the loan decision. Instead of relying on a traditional income-based mortgage structure, the DSCR loan focuses on whether the rental property can support the payment.

Ziffy’s Takeaway

This case study is a strong example of how DSCR refinancing can help investors move from project-stage debt into rental-stage financing.

The investor had a clear plan, the property had documented rental income, and the DSCR was strong enough to support the refinance. That combination made the file work.

For investors using hard money to buy and rehab rentals, the refinance plan should not be an afterthought. The exit loan matters before the first loan is even paid off. A DSCR refinance can give investors a structured way to move out of short-term debt once the property is leased and the rent supports the numbers.

Ready to Refinance a Rental Property?

Ziffy helps real estate investors review DSCR financing options for rental purchases, rate-and-term refinances, and cash-out refinances.

If your rental property is generating income and you want to refinance out of hard money or another short-term loan, Ziffy can help you evaluate the DSCR, PITIA, LTV, and loan structure before you move forward.