Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

DSCR loan closing costs usually fall in the 2% to 5% range of the loan amount, before the down payment. On a $300,000 loan, that means an investor should generally plan for $6,000 to $15,000 in closing costs, with the final number depending on the lender, property location, loan structure, title costs, appraisal requirements, insurance, escrow setup, and whether the loan includes discount points.

That number is separate from the down payment. If your DSCR loan requires 20% down on a $400,000 rental property, the down payment is $80,000. Closing costs are added on top of that. A deal that looks like an $80,000 cash requirement can quickly become an $88,000 to $96,000 cash-to-close requirement once lender fees, third-party fees, prepaid expenses, tax and insurance escrows, and entity costs are included.

The Loan Estimate shows key mortgage terms and estimated costs after a borrower applies. The Consumer Financial Protection Bureau recommends comparing Loan Estimates across lenders before choosing a loan.

This guide breaks down the cost stack, explains why DSCR loans often cost more to close than conventional loans, and shows where investors have real room to reduce cash due at closing.

Table of Contents

DSCR Loan Closing Costs: Full Cost Breakdown

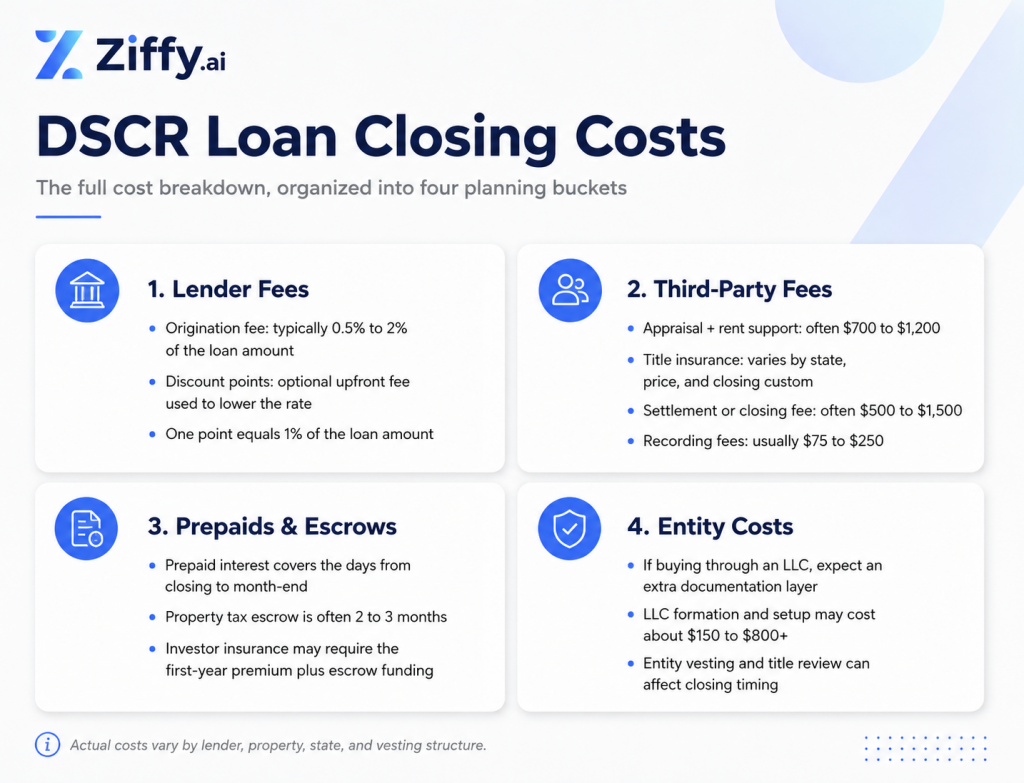

A DSCR loan closing usually includes four major cost groups: lender fees, third-party fees, prepaid expenses, and entity-related costs if the investor is buying through a limited liability company (LLC) or another entity vesting structure.

Lender Fees

1. Origination fee

The origination fee is the lender’s charge for processing, underwriting, and funding the loan. For DSCR loans, origination commonly ranges from 0.5% to 2% of the loan amount, though the exact amount depends on the lender, loan size, borrower profile, property type, and pricing structure.

DSCR loans are non-QM products. They qualify on property rental income rather than borrower W-2s, and they are not sold to Fannie Mae or Freddie Mac. That changes where the capital comes from, and it changes the cost. The Consumer Financial Protection Bureau (CFPB) maintains the official Ability-to-Repay and Qualified Mortgage rule resources that define the QM framework for residential mortgage lending.

In our experience, investors who ask for both a point and a no-point quote upfront close with fewer surprises at the Loan Estimate stage because the tradeoff is visible before the file is too far along to restructure.

2. Discount points

Discount points are optional upfront fees paid to reduce the interest rate. One point equals 1% of the loan amount. On a $300,000 DSCR loan, one point costs $3,000.

Points show up more often on DSCR loans because investors are often solving for monthly cash flow, not just the lowest upfront cost. A lower rate can improve PITIA, which means principal, interest, taxes, insurance, and association dues. That can help the DSCR ratio and monthly cash flow. But points only make sense if the monthly savings justify the upfront cost over your expected hold period.

A long-term rental investor who plans to hold for seven to ten years may view points very differently from an investor who expects to refinance or sell within two years.

Third-Party Fees

1. Appraisal and rent schedule

A DSCR appraisal usually costs more than a standard owner-occupied appraisal because the lender needs both a property value and a market rent opinion. For many single-family investment properties, that means the appraiser completes a comparable rent schedule in addition to the valuation report.

Fannie Mae’s appraisal guidance states that the Single-Family Comparable Rent Schedule, Form 1007, is required when the property is a one-unit investment property and the borrower is using rental income to qualify. While DSCR loans are not agency loans, the same rent-schedule concept is central to DSCR underwriting because the loan depends on the property’s rental income.

For planning purposes, many investors should budget $700 to $1,200 for a DSCR appraisal with rent support. The actual fee depends on the market, property type, appraiser availability, and whether additional complexity is involved.

Lucas Hernandez

Mortgage Loan Originator

Ziffy Mortgage

NMLS #2171747What we see often is investors budgeting for a conventional appraisal and getting surprised when the DSCR appraisal comes in higher. The rental schedule is not just an add-on. It supports the rent number used in the DSCR calculation, so it becomes part of the underwriting file.

2. Title insurance

Title costs usually include a lender’s title policy and, in many transactions, an owner’s title policy. The lender’s policy protects the lender’s lien position. The owner’s policy protects the buyer’s ownership interest if a covered title issue appears later.

Title costs vary widely by state, purchase price, loan amount, and local closing customs. Some states rely more heavily on attorneys. Others use title or escrow companies as the main settlement party. Because title is so state-specific, investors should review this line on the Loan Estimate instead of assuming the same cost from a previous closing in another market.

3. Settlement, escrow, or closing fee

This is the fee charged by the settlement agent, escrow company, title company, or closing attorney handling the transaction. It covers the administrative work of preparing documents, collecting funds, coordinating signatures, disbursing money, and recording the transaction.

A reasonable planning range is $500 to $1,500, though higher-cost markets or more complex entity transactions may run above that.

4. Recording fees

Recording fees are charged by the county or local recording office to record the deed, mortgage, and related documents. These are usually smaller than the other closing costs, often in the $75 to $250 range, but they vary by jurisdiction.

Prepaid Expenses and Escrows

1. Prepaid interest

Prepaid interest covers the interest owed from the day the loan closes through the end of that month. If you close early in the month, you pay more prepaid interest at closing. If you close near the end of the month, you pay fewer days of interest upfront.

For example, a $300,000 loan at an 8% annual rate creates about $65.75 in daily interest:

$300,000 × 8% ÷ 365 = $65.75 per day

Closing with 25 days left in the month would create roughly $1,644 in prepaid interest. Closing with five days left would create roughly $329. The payment timing changes later, but the cash-to-close difference can matter when you are trying to keep funds available for reserves, repairs, or leasing.

2. Property tax escrow

Many DSCR lenders require an escrow account for taxes and insurance. At closing, the borrower funds the escrow account so the servicer has enough money to pay future property tax bills.

The amount depends on the property’s tax bill, the closing month, and when the next tax payment is due. A common planning range is two to three months of property taxes, but some files require more because of the local tax calendar.

3. Investor property insurance

Rental properties generally require landlord insurance rather than a standard owner-occupied homeowner policy. Depending on the property and use, the policy may be structured as a DP3, or dwelling fire policy, or a similar landlord policy.

Investor insurance can cost more than owner-occupied coverage because the risk profile is different. Tenant occupancy, vacancy exposure, liability, property condition, local weather risk, and potential loss-of-rent coverage can all affect the premium.

One thing that surprises investors is how much investor insurance can vary by state and property type. Location, vacancy exposure, and insurer assumptions can move the premium enough to change both cash-to-close and DSCR because insurance is part of PITIA.

At closing, investors may need to pay the first full year of insurance upfront, plus additional months into escrow. This is one of the most common cash-to-close surprises because buyers often model monthly insurance but forget the upfront premium requirement.

Entity Costs if You Buy Through an LLC

If you’re buying through an LLC, which many DSCR lenders allow or prefer, expect one more documentation layer before closing and one more line item in your cost stack.

1. LLC formation and operating agreement

If the entity already exists, the lender may need the operating agreement, articles of organization, certificate of good standing, EIN documentation, and signing authority information. If the LLC does not exist yet, formation costs depend on the state, attorney involvement, registered agent costs, and filing speed.

A simple planning range is $150 to $800, but attorney-prepared structures or expedited filings can cost more.

2. Entity vesting and title review

When title is vested in an entity, the title company and lender must confirm that the entity is valid, authorized to hold title, and properly represented by the person signing loan documents. The cost is not always large, but the timing matters. A missing operating agreement or unresolved entity issue can delay closing even when the loan itself is approved.

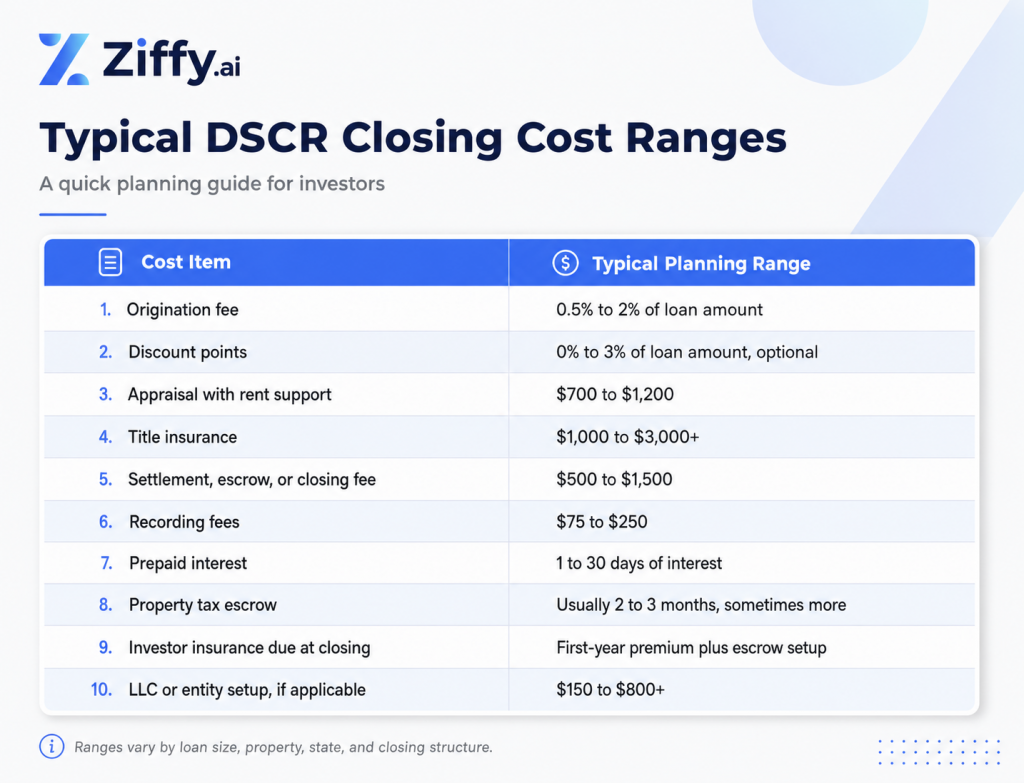

Typical DSCR Loan Closing Cost Ranges

These are planning ranges, not guaranteed quotes. The actual number should come from your Loan Estimate and, before closing, your Closing Disclosure. The CFPB’s Closing Disclosure rule covers the statement of final loan terms and closing costs that borrowers compare against the Loan Estimate.

Why DSCR Closing Costs Can Run Higher Than Conventional Loan Costs

In our experience, the gap between what investors expect to close a DSCR loan and what they actually need to wire usually comes from three areas: the non-QM cost structure, the rental income appraisal, and investor insurance.

A conventional investment property loan is usually evaluated through borrower income, credit, assets, debt-to-income ratio, and agency eligibility rules. A DSCR loan is built around the rental property’s income. The lender looks at whether the property’s rent can support the monthly PITIA payment.

The cost difference starts with the capital structure. DSCR loans are not sold to the agencies. The capital behind them is priced differently, and that shows up through the interest rate, origination fee, and how often points are part of the conversation. The rental income appraisal adds another layer. Investor insurance is also priced against a risk profile that owner-occupant policies do not carry.

The appraisal process carries more weight because rent is central to qualification. The lender is not just confirming value. It also needs a rent figure that can support the DSCR calculation. For a one-unit investment property where rental income is being used, Form 1007 is the recognized comparable rent schedule in agency appraisal guidance, and DSCR lenders often rely on the same type of rent support for underwriting.

Investor insurance is not priced like a primary-residence policy. A rental property has different risk exposure. A vacant investment property, long-term rental, short-term rental, and tenant-occupied single-family home can all produce different insurance quotes. If the insurance number comes in higher than expected, it can affect both cash to close and DSCR because insurance is part of PITIA.

The cost stack on a DSCR loan is not random. The appraisal has to support rent, the insurance has to match investment use, and the pricing reflects the non-QM structure. Investors who understand those pieces early usually have a cleaner closing because the final cash-to-close number does not feel like a surprise.

Where Investors Can Reduce DSCR Closing Costs

The appraisal fee, recording charges, and most title rates are fixed or close to it. You cannot negotiate them down meaningfully. The room is in the lender’s pricing structure and in how you time the close.

Compare rate-and-fee options, not just the interest rate

A DSCR loan with a lower rate may include points. A DSCR loan with fewer upfront costs may come with a higher rate. Neither structure is automatically better.

The right choice depends on your investment plan. If you expect to hold the property for a long time, paying points can make sense if the monthly savings repay the upfront cost. If you expect to refinance or sell within a shorter window, a no-point or lower-cost structure may preserve more cash for reserves and future acquisitions.

Ask for a no-point version of the same quote

If your Loan Estimate includes discount points, ask your loan officer to show the same loan with zero points. Then compare the monthly payment difference.

The break-even math is simple:

Cost of points ÷ monthly payment savings = months to break even

If points cost $6,000 and save $150 per month, the break-even period is 40 months. If you do not expect to keep the loan that long, the upfront cost may not be worth it.

Use lender credits carefully

A lender credit can reduce cash due at closing in exchange for a higher interest rate. This can help when cash-to-close is the main constraint, but it increases the monthly payment and can weaken cash flow.

For investors trying to scale, lender credits can preserve liquidity. For investors buying a long-term hold with stable rent, a lower rate may be more valuable. The tradeoff should be evaluated against cash flow, DSCR, reserves, and hold period.

Time the closing date with prepaid interest in mind

Closing near the end of the month can reduce prepaid interest due at closing. This does not eliminate interest. It changes the timing of when the cost is paid. Still, for investors managing a tight cash-to-close number, the difference can be useful.

Review title and settlement fees early

Title insurance rates are fixed or heavily regulated in many states, but settlement, escrow, courier, wire, and administrative fees can vary by provider. If the contract allows the buyer to select title or settlement services, investors may have room to compare providers.

I usually separate the closing costs into two groups for investors: fixed costs and strategy costs. The appraisal, recording fees, and title rates are fixed. There’s no real room there. Points, lender credits, and timing are where the structure can move. The question I ask is: how long is this investor planning to hold the loan? If it’s a long-term hold, buying the rate down usually makes sense past the 36-month mark. If the investor might refinance in two years, I’d rather keep that cash liquid for the next deal.

How Closing Costs Affect Your DSCR Deal Analysis

Most investors track the down payment carefully and treat closing costs as a number they will figure out after the deal is under contract. By then, the structure is set. Modeling the full cost stack before the Loan Estimate arrives gives you the leverage to adjust, whether that means asking for lender credits, reconsidering the point structure, or confirming the deal still works at the real capital-in number.

Cash-on-cash return should be calculated on total cash invested. That means down payment, closing costs, upfront lender fees, prepaid costs, escrow deposits, and any immediate repair or rent-ready expenses.

The second number is the cleaner number because it reflects the actual cash the investor put into the deal.

At Ziffy, the investor workflow is built around the full deal, not just the purchase price and rent. Before applying, investors can use the DSCR loan calculator to test the rent-to-PITIA ratio, the rental property ROI calculator to estimate return on capital, and the cash flow calculator to see how the monthly numbers look after real expenses.

The strongest DSCR files are not always the ones with the highest rent. They are often the files where the investor has modeled taxes, insurance, closing costs, reserves, and financing terms before the Loan Estimate arrives.

DSCR Closing Costs vs. Cash Reserves

Investors sometimes arrive at the closing table having funded the down payment and the closing costs, with nothing else left over. That is a problem because DSCR lenders verify reserves after closing, not before.

Closing costs are paid to complete the transaction. Reserves are the funds you still have available after closing. On a DSCR loan, reserves help show that you can carry the property if rent is delayed, repairs come up, or the unit sits vacant for a period.

Ziffy’s DSCR program commonly requires at least two months of PITIA in verified liquid reserves after closing, depending on borrower, property, and loan eligibility. That means an investor should not wire every available dollar into the down payment and closing costs.

For a complete breakdown, read How Much Cash Reserves Do You Need for an Investment Property Loan?

How to Read Your Loan Estimate for DSCR Closing Costs

When you receive a Loan Estimate, review it in layers instead of only looking at the total cash-to-close number.

- Start with lender charges: origination, underwriting, processing, and discount points. These lines tell you how the loan is priced before any third-party cost is added.

- Then review third-party services. Appraisal, credit report, title, settlement, escrow, attorney, recording, and transfer-related charges can sit in different places depending on how the estimate is prepared.

- Next, review prepaid expenses and escrows. This is where investors often miss the real cash requirement. Prepaid interest, the first-year insurance premium, property tax deposits, and insurance escrow deposits can move the final number materially.

- Finally, compare the Loan Estimate to the Closing Disclosure before signing. CFPB forms and samples show how Loan Estimates and Closing Disclosures are structured, and the Closing Disclosure is designed to show final loan terms and closing costs before closing.

If a number moved, ask why it moved. Some changes are normal because title, tax, escrow, and prepaid amounts become more accurate as the closing date approaches. Other changes need a clear explanation before you wire funds.

Next Steps

Closing costs do not disappear because they are not the headline number. The deal should be modeled on total capital deployed: down payment, closing costs, reserves, and any upfront expenses before the Loan Estimate arrives.

For a deeper look at DSCR financing, start with the DSCR Loan Guide. To review eligibility rules, read DSCR Loan Requirements in 2026. If you are comparing loan paths, see DSCR Loan vs. Conventional Loan. For a broader look at investor financing options, review our guide to investment property loans.

To estimate your numbers before applying, use the DSCR loan calculator and model the property with real rent, taxes, insurance, and closing cost assumptions.

FAQs

How much are closing costs on a DSCR loan?

DSCR loan closing costs commonly range from 2% to 5% of the loan amount, before the down payment. On a $300,000 loan, that usually means planning for about $6,000 to $15,000 in closing costs. The final amount depends on lender fees, discount points, appraisal, title, settlement fees, prepaid interest, tax and insurance escrow, and property location.

Can DSCR loan closing costs be rolled into the loan?

On a purchase, closing costs are usually not rolled into the loan because the loan amount is based on the purchase price and eligible loan-to-value limit. The borrower typically brings closing costs in addition to the down payment. On a refinance, some costs may be financed into the new loan amount if the transaction still meets LTV, DSCR, and eligibility requirements.

Are DSCR loan closing costs higher than conventional loan closing costs?

They can be. DSCR loans often include higher lender pricing, appraisal costs with rental income support, investor insurance, and entity documentation if the property is bought through an LLC. Conventional loans follow a different underwriting and pricing structure, especially when they fit agency guidelines.

Why does a DSCR appraisal cost more?

A DSCR appraisal often costs more because the lender needs a rent opinion in addition to a property value. For one-unit investment properties where rental income is used, Fannie Mae’s appraisal guidance identifies Form 1007 as the comparable rent schedule. DSCR lenders rely on rent support because the property’s income drives the loan qualification.

Do I have to pay discount points on a DSCR loan?

No. Discount points are optional, but the rate you choose may include them. Investors should ask for both a point and no-point option so they can compare upfront cost against monthly payment savings. The better choice depends on cash flow, hold period, refinance plans, and available reserves.

Do DSCR loans require cash reserves after closing?

Yes, reserves are commonly required. Ziffy’s DSCR program generally requires at least two months of PITIA in verified liquid reserves after closing, subject to borrower, property, and loan eligibility. Reserves are separate from closing costs. Closing costs are paid to complete the transaction. Reserves are funds left over after closing.

What is the biggest closing cost surprise on DSCR loans?

The biggest surprises are usually appraisal cost, investor insurance, prepaid interest, and escrow deposits. Many investors model the down payment correctly but underestimate the cash needed for the first-year insurance premium, tax escrow, and prepaid interest.

How can I lower cash due at closing on a DSCR loan?

The most realistic options are asking for a no-point quote, considering lender credits, comparing eligible title or settlement providers when allowed, and timing the closing date to reduce prepaid interest. Investors should not assume the appraisal fee can be negotiated because the lender usually orders the appraisal through its approved process.