Editorial Integrity

Making sound real estate investment decisions begins with reliable, data-driven insights. At Ziffy.ai, we offer an AI-native real estate investing, proprietary data-driven trend analysis, investment mortgage programs like DSCR loans, and a network of over 500 investor-friendly real estate agents to deliver the expertise needed for informed decisions. Our content is crafted by experienced real estate professionals and backed by real-time market data, ensuring you receive accurate and actionable information. Through a rigorous editorial process, we strive to empower your investment journey with trustworthy and up-to-date guidance.

Quick Answer:

A bridge loan is usually the better choice when you need fast, short-term capital to acquire, renovate, or reposition an investment property. It fits deals where timing matters, the property is not ready for permanent financing, or the exit strategy is a sale or refinance.

A HELOC can make sense when you already have an open line of credit, available equity, a slower acquisition timeline, and a clear plan to repay the line. The tradeoff is that the property securing the HELOC is exposed if repayment becomes difficult.

For many rental investors, the stronger path is to use a bridge loan for the acquisition or stabilization phase, then refinance into a DSCR loan once the property is rent-ready and the rental income can support the long-term debt.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Table of Contents

Bridge Loan vs HELOC: The Core Difference

A bridge loan and a HELOC both create access to capital, but they put different assets at risk and solve different timing problems.

A bridge loan is short-term financing used to bridge the gap between an immediate funding need and a future exit. Investors often use bridge loans to buy a property quickly, renovate a property, acquire before another property sells, or stabilize a rental before refinancing.

A HELOC, or home equity line of credit, is a revolving credit line secured by a property you already own. The Consumer Financial Protection Bureau defines a HELOC as an open-end line of credit that lets you borrow repeatedly against your home equity.

The distinction is collateral. A bridge loan is usually tied to the investment deal or transition plan. A HELOC is tied to the property securing the line, which may be your primary residence or another property in your portfolio.

- Use a bridge loan when the new deal needs short-term acquisition or transition financing.

- Use a HELOC when you want to tap existing equity and are comfortable putting the property securing the line behind the borrowing.

In our experience, investors get into trouble when they treat those two options as if they are only rate comparisons. The structure matters just as much as the cost.

What Is a Bridge Loan?

A bridge loan is a short-term real estate loan used when an investor needs capital before a property is ready for its next financing stage. That next stage may be a sale, a DSCR refinance, a rate-and-term refinance, a cash-out refinance, or payoff from another planned source.

At Ziffy Mortgage, the bridge loan program is designed for real estate investors who need quick, interim financing for investment properties. Current bridge loan features include:

Program note: Bridge loan terms shown reflect current Ziffy Mortgage program guidelines as of May 2026. Rates, terms, LTVs, loan amounts, approval timing, and eligibility requirements are subject to change without notice. Final approval depends on borrower qualifications, property type, appraisal, title, credit profile, leverage, exit strategy, reserves, and underwriting review.

Bridge Loan Feature | Ziffy Bridge Loan Terms |

|---|---|

Minimum credit score | 650 |

Down payment | 25% |

Loan term | 6 to 24 months |

Loan amount | $100K to $10M |

Purchase LTV | Up to 75% |

Rate-and-term refinance LTV | Up to 70% |

Cash-out refinance LTV | Up to 65% |

Core requirements | Property equity, exit strategy, property appraisal |

Approval time | Within 15 days |

Bridge loans are commonly used for auction purchases, fix and flip projects, fast acquisitions, buy-before-sell situations, properties needing repairs before long-term financing, vacant rentals needing lease-up, and properties that may later refinance into DSCR financing.

The defining feature is not only speed. It is the fact that the loan is tied to a short-term plan. A bridge loan should have a clear exit before you close.

What Is a HELOC?

A HELOC is a home equity line of credit. It lets a homeowner borrow against available equity in a property they already own.

Unlike a closed-end loan, where the borrower receives one lump sum and repays it on a fixed schedule, a HELOC works more like a revolving line. The borrower can draw, repay, and draw again during the draw period, depending on the lender’s terms.

The Federal Trade Commission explains HELOCs as revolving lines of credit secured by the home. The FTC also notes that HELOCs typically have variable APRs and that borrowers make payments only on the amount they borrow, not the full approved line.

For investors, a HELOC may be used as acquisition capital when the borrower has equity in a primary residence, second home, existing rental property, or paid-off property. The appeal is flexibility. If the line is already open and available, the investor may be able to draw funds quickly for a down payment, repairs, earnest money, or part of the acquisition.

But flexibility does not remove risk. The property securing the HELOC is still collateral. If the borrower cannot repay the line as agreed, that property can be at risk.

Bridge Loan vs HELOC Comparison Table

Factor | Ziffy Bridge Loan | HELOC |

|---|---|---|

Best use | Acquiring, renovating, or repositioning an investment property | Pulling available equity from a property you already own |

Collateral | Usually tied to the investment property or deal structure | The property securing the HELOC |

Speed | Built for fast investment transactions | Fast if already open; slower if a new HELOC must be approved |

Repayment structure | Short-term loan with a defined exit | Revolving line during draw period, then repayment period |

Rate type | Short-term investor-loan pricing | Usually variable-rate pricing |

Exit strategy | Required from the start | Often separate from the new investment deal |

Best fit | Auctions, flips, quick acquisitions, buy-before-sell, delayed refinance | Lower-pressure deals where usable equity is already available |

Main risk | Refinance or sale exit takes longer than expected | Existing property is at risk if repayment fails |

Tax treatment | Depends on loan use and structure | HELOC interest is not automatically deductible |

When a Bridge Loan Is the Better Choice

A bridge loan is usually the better option when the investment deal itself needs specialized short-term financing.

1. The deal needs speed

Speed is one of the biggest reasons investors use bridge loans. Traditional financing can move too slowly for auctions, distressed sellers, price-drop opportunities, or properties where the seller wants a clean and fast closing timeline.

Ziffy’s bridge loan program is built around investor execution, with approval possible within 15 days depending on the file. That matters when the deal will not wait for a long underwriting cycle.

A HELOC can also be fast if the line is already open. But if you still need to apply for a new HELOC, complete valuation, wait for underwriting, and satisfy lender conditions, it may not solve the timing issue.

2. The property is not ready for permanent financing

Some investment properties are attractive because they are not fully stabilized yet. That may include a property that needs repairs before lease-up, a vacant rental that needs renovation, a property with deferred maintenance, a fix and flip opportunity, or a deal where the current condition does not support permanent financing yet.

In that situation, bridge financing can make more sense than trying to force the deal into long-term financing too early. The investor can acquire the property, complete the business plan, then evaluate whether to sell, refinance, or hold.

If the plan is resale, run the project through Ziffy’s Fix and Flip Calculator before committing capital. If the plan is to hold the property as a rental, review long-term performance through the Rental Property ROI Calculator.

3. The investment has a BRRRR-style path

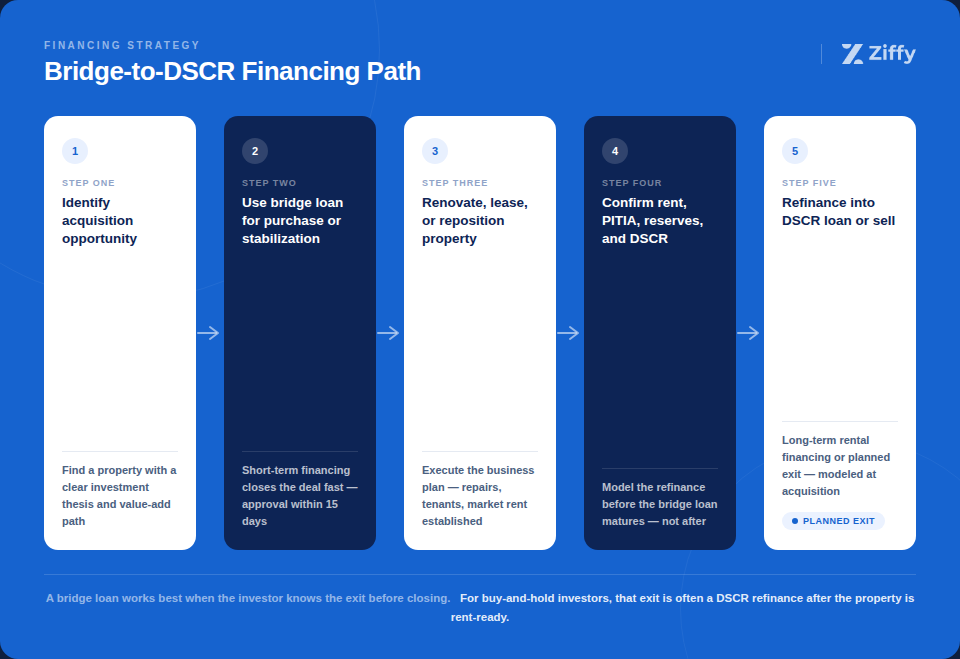

A bridge loan can also make sense when the investor is following a buy, rehab, rent, refinance, repeat strategy. In that structure, short-term financing supports the acquisition and renovation phase, while long-term rental financing becomes the exit.

That is why a bridge-to-DSCR plan often overlaps with the BRRRR method. The bridge loan helps the investor take control of the property before it is fully stabilized. The DSCR refinance comes later, once rent and PITIA can be evaluated.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

4. You want the financing tied to the investment property

A bridge loan is usually structured around the investment opportunity. That can make the risk cleaner because the financing is connected to the asset being acquired or repositioned.

A HELOC may use a different property as collateral. For example, an investor might borrow against a primary residence to buy a rental property. That can work, but the risk shifts away from the new investment and onto the property securing the credit line.

A cleaner way to evaluate the decision is this:

- A bridge loan asks, “Can this investment plan repay the loan?”

- A HELOC asks, “Are you willing to put existing equity behind this new investment decision?”

Those are different risk questions.

5. You already know the exit

Bridge loans work best when the investor can clearly answer one question: how will this loan be paid off? The exit may be a sale after renovation, a refinance into DSCR financing, a refinance after lease-up, the sale of another property, portfolio restructuring, or cash payoff after a planned liquidity event.

If the exit is vague, the bridge loan is not ready. Short-term financing becomes risky when the borrower treats the payoff plan as something to solve later.

When a HELOC Can Make Sense

A HELOC can be useful when the investor understands the risk and the deal does not require the specialized structure of a bridge loan.

1. The line is already open

A HELOC is most useful as acquisition capital when the line is already approved and available. In that case, the investor may be able to draw funds quickly for a down payment, earnest money, repairs, or a cash-style purchase strategy.

The keyword is “available.” A HELOC that still needs approval is different from a HELOC that is already open and ready to draw.

2. The acquisition timeline is not tight

If the seller is flexible, the closing timeline is standard, and the investor does not need a fast asset-based loan, a HELOC may be worth considering.

That said, investors should not assume the HELOC will remain available at the exact amount expected. HELOC access can be affected by lender rules, property value changes, borrower profile changes, and credit-line terms.

3. You are using the HELOC as one part of the capital stack

Using a HELOC for part of the acquisition can be less risky than using it as the whole strategy.

For example, an investor might use a modest draw for repairs or reserves while financing the purchase separately. The danger starts when the HELOC becomes the entire plan, especially if the investment property has uncertain rent, heavy rehab, no clear refinance path, or thin reserves.

4. You have strong liquidity outside the HELOC

HELOC flexibility can create false confidence. Investors should still hold reserves that are not borrowed from the same line.

What we see often is that investors count the available HELOC balance as a backup plan. That is not the same as having cash reserves. A credit line can be reduced, frozen, repriced, or fully drawn at the exact moment the deal needs liquidity.

5. You understand the tax treatment

Do not assume HELOC interest is deductible just because the money is being used for real estate.

The IRS home mortgage interest deduction rules say interest on home equity loans and lines of credit is deductible under those rules only if the borrowed funds are used to buy, build, or substantially improve the home that secures the loan, subject to other requirements.

Ziffy Mortgage does not provide tax or legal advice. Consult a licensed tax professional or attorney for guidance on your specific situation before using HELOC funds, bridge financing, or investment debt for a property acquisition.

What Most Guides Don’t Mention About HELOCs and Reserves

What most guides don’t mention is that a HELOC draw can tighten your next refinance file. It does not just add another monthly payment. It can also change how a DSCR lender reads your reserve position, liquidity, and overall risk profile.

If you use a HELOC to fund a down payment, closing costs, repairs, or carry costs, that debt may still show up when you apply for the next loan. If your plan is to refinance into DSCR financing, the lender will look at the full file, including liquidity, reserves, property income, PITIA, credit profile, and other obligations.

That means the same HELOC that helped you close can also tighten your refinance file if it weakens your reserves or adds a monthly obligation that changes the overall risk picture.

This is why the bridge-to-DSCR plan should be modeled before acquisition, not after the renovation is complete. Review the expected rent, taxes, insurance, HOA dues, loan amount, and reserve requirement early. Ziffy’s guide to cash reserves for investment property loans explains why liquidity matters beyond the down payment.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

How the Exit Strategy Should Drive the Decision

The exit strategy should decide the financing structure, not the other way around.

If your exit is resale, compare bridge financing against project profit

For a flip or resale strategy, the investor needs to know whether the acquisition price, rehab budget, holding costs, selling costs, and financing costs still leave enough margin.

This is where investors should review Ziffy’s Fix and Flip Loan Guide and test the numbers in the Fix and Flip Calculator. A bridge loan can help you move quickly, but speed does not fix a weak spread.

If your exit is rental refinance, think bridge-to-DSCR

For a buy-renovate-hold strategy, bridge financing can handle the acquisition and stabilization phase. Once the property is rent-ready and income can be documented, a DSCR refinance may become the long-term structure.

Ziffy’s DSCR Loan Guide explains how DSCR financing qualifies the property mainly around rental income rather than W-2s, pay stubs, tax returns, or personal DTI. Investors who want a deeper breakdown can also review Ziffy’s guide to rental property loans with no tax returns.

Before assuming the refinance will work, run the estimated rent and full PITIA through the DSCR Loan Calculator. If the projected DSCR is tight, the investor may need to adjust leverage, purchase price, rent assumptions, or reserves before closing the bridge loan.

If the investor plans to refinance and pull equity back out after stabilization, Ziffy’s guide to DSCR cash-out refinance should be part of the early planning process.

If your exit depends on another property selling, build in timing risk

Buy-before-sell situations can be practical, but they carry timing risk.

A bridge loan can help an investor acquire before a sale closes, but the exit still depends on the old property selling or refinancing within the expected window.

A HELOC can also be used in this situation, but the investor should be clear about which property secures the line and what happens if the sale takes longer than planned.

If your plan is long-term buy and hold, avoid short-term debt without a refinance path

A bridge loan is not meant to be permanent rental debt. It can be the right tool for acquisition, but only when there is a realistic refinance or sale plan.

A HELOC is also not a substitute for disciplined rental underwriting. If the property cannot support the long-term financing, tapping existing equity does not make the deal stronger. It only changes where the borrowed funds came from.

Use Ziffy’s Cash Flow Calculator, Cash-on-Cash Calculator, and Rental Property ROI Calculator before deciding whether the acquisition is worth financing.

Scenario-Based Recommendations: Which One Fits Your Deal?

- Use a bridge loan if the property needs speed, repairs, lease-up, or a clear transition period before permanent financing. This is the cleaner structure when the deal depends on acquiring the property first, improving or stabilizing it, and then exiting through a sale or DSCR refinance.

- Use a HELOC if the line is already open, the acquisition is not time-sensitive, and you are using the draw as one part of the capital stack rather than the entire investment plan. The line should not replace reserves, and the property securing the HELOC should not be exposed casually.

- For a fix and flip investor, bridge financing usually fits better because the loan can be tied to the acquisition, rehab, and resale timeline.

- For a BRRRR investor, a bridge loan can work well when the plan is to buy, rehab, rent, and refinance into DSCR financing after stabilization.

- For a rental investor buying a property that is already rent-ready, starting with a DSCR loan may be cleaner than adding short-term debt first.

- For an investor using equity from an existing property, a HELOC can work only when the repayment plan is clear and the collateral risk is acceptable.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Can You Combine a Bridge Loan and a HELOC?

Some investors use more than one source of capital on the same acquisition, but the structure needs to be planned carefully.

A HELOC may be used for part of the capital stack, such as a portion of the down payment, repairs, or liquidity support. A bridge loan may fund the acquisition or stabilization phase. The issue is not whether the two can technically appear in the same investor strategy. The issue is whether the combined debt leaves enough reserves, keeps the exit realistic, and avoids overexposing another property.

If the HELOC is heavily drawn, the investor may have less liquidity available when applying for the DSCR refinance. If the bridge loan has a short maturity date, the investor also needs enough time to renovate, lease, document rent, and complete the refinance. Using both can work, but only when the exit has been modeled before closing.

In our experience, combining short-term debt with revolving credit is where investors need the most discipline. The structure should improve the acquisition plan, not hide weak reserves or make an already tight deal appear stronger.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

Practical Acquisition Scenario

Consider an investor buying a property that needs repairs before it can be rented at full market value.

The investor has two possible paths.

- Path one is using a HELOC secured by an existing property. This may give the investor flexible funds, but it also places the existing property behind the new acquisition decision. If repairs run over budget or the rental refinance is delayed, the pressure does not stay isolated to the new property.

- Path two is using a bridge loan for the acquisition and stabilization phase. This keeps the financing tied more directly to the investment plan. The investor still needs a real exit, but the structure is built around the short-term transition.

Here’s what actually happens in many files: the stronger option is usually the one with the cleaner exit, not the one with the lowest starting cost. If the investor can show a realistic renovation budget, a supportable rent estimate, adequate reserves, and a DSCR refinance path, the bridge loan is easier to evaluate as part of a complete investment plan.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

How Ziffy Looks at Bridge Loan Scenarios

For a bridge loan, the property and the exit strategy carry most of the conversation. We start by looking at the asset itself: what the investor is acquiring, its current condition, the purchase price, the equity position, and whether the appraisal supports the plan. From there, the file becomes a question of execution. A strong bridge scenario should show what changes after closing, whether that means repairs, lease-up, stabilization, resale, refinance, or another defined payoff source.

Liquidity matters here as much as the property story. A borrower who can close but cannot carry the property through delays is taking on more risk than the numbers may show at first glance. Renovation timelines stretch. Insurance can come in higher than expected. Taxes can reset after purchase. Appraisals and rent estimates can change the refinance math. That is why we look for a realistic timeline, enough reserves to handle friction, and a payoff plan that does not depend on everything going perfectly.

The file gets stronger when the investor can show that the bridge loan is not being used to cover a weak deal. It is being used to solve a timing or transition problem. A bridge loan should help you move faster on a strong plan. It should not be used to avoid answering hard questions about resale value, rent, rehab costs, taxes, insurance, or refinance feasibility.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Where DSCR Financing Fits After the Acquisition

A bridge loan can help an investor acquire or stabilize a property. A DSCR loan can help an investor hold the property after it starts functioning as a rental.

That bridge-to-DSCR path is common because the property may not be ready for long-term rental financing on day one. Maybe it needs repairs. Maybe it needs tenants. Maybe rents need to be documented. Maybe the investor is buying at a discount and needs time to execute the plan.

Once the property is ready, DSCR becomes relevant because the loan is evaluated around the rental income of the property. At Ziffy Mortgage, best terms are generally tied to stronger DSCR performance. A DSCR of 1.00 or above usually creates the cleanest path on a standard file. Eligible lower-ratio files may still be reviewed through a no-ratio DSCR option, depending on the full structure.

Investors should also review Ziffy’s DSCR loan requirements before assuming the refinance will work. The loan amount, rent support, reserves, property type, credit profile, and PITIA all matter. That is why investors should not wait until the bridge loan is about to mature before thinking about DSCR. The refinance should be modeled at acquisition.

Before closing the bridge loan, ask:

- What rent will underwriting likely use?

- What will PITIA look like after refinance?

- Will taxes reset after purchase?

- Is insurance realistic for the property type and location?

- Are HOA dues included?

- Will the property be long-term rental or short-term rental?

- Will the file need stronger reserves?

- Will the refinance work at the expected loan amount?

The investor who answers these questions early has a stronger financing plan than the investor who only focuses on getting the acquisition closed.

Common Mistakes Investors Make When Comparing Bridge Loans and HELOCs

Mistake 1: Comparing only the interest rate

A HELOC may look cheaper at first, especially if the line is already open. But the true comparison is not rate alone. Investors need to compare collateral risk, repayment structure, draw availability, closing certainty, and exit timing. A lower rate does not automatically make a HELOC safer.

Mistake 2: Ignoring variable-rate exposure

Many HELOCs have variable rates. The Federal Reserve’s H.15 release publishes selected interest rates, including the bank prime loan rate. HELOC pricing often moves with prime-rate conditions, so investors should not treat the current payment as fixed unless the HELOC terms clearly say otherwise.

Mistake 3: Using a HELOC as if it were permanent capital

A HELOC can feel like available cash, but it is still secured debt. If the investor uses it to buy a rental property, there still needs to be a repayment plan. That plan might be a refinance, sale, rental cash flow, or paydown from other liquidity. “I’ll figure it out later” is not a plan.

Mistake 4: Taking a bridge loan without a DSCR check

If the planned exit is a DSCR refinance, the investor should review DSCR before closing the bridge loan. Waiting until the property is stabilized can create problems if the refinance loan amount, rent support, taxes, insurance, or reserves do not line up. Use the DSCR Loan Calculator early, then talk through the refinance path before the bridge loan closes.

Lucas Hernandez

Mortgage Loan Originator, NMLS #2171747

Mistake 5: Underestimating reserves

Short-term debt needs liquidity. Renovation delays, tenant delays, permit issues, insurance changes, and appraisal gaps can all create pressure.

A stronger investor does not just have cash to close. They have cash to carry the property if the timeline stretches. Ziffy’s guide to cash reserves for investment property loans explains how reserves support the file beyond the down payment.

Mistake 6: Forgetting financed-property limits in conventional planning

Investors using conventional loans should also understand that financed-property counts can affect eligibility and reserves.

Fannie Mae’s multiple financed properties guidance includes a 10-property limit for second homes and investment properties under Desktop Underwriter. It also explains that mortgages and HELOCs may be used when determining the number of financed properties.

That does not mean every investor should avoid conventional financing. It means active investors need to understand how each new debt obligation may affect the next loan file.

Bridge Loan vs HELOC: Decision Framework

A bridge loan is the better fit when the deal is time-sensitive, the property needs renovation or lease-up, the investor needs short-term financing tied to the investment property, and the payoff plan is already clear. It is especially useful when the exit is a sale, DSCR refinance, or cash-out refinance after stabilization.

A HELOC is more appropriate when the line is already open, the acquisition timeline is not urgent, the investor has liquidity outside the credit line, and the borrower is comfortable with the property securing the HELOC being exposed to the new investment decision.

Neither option is a good fit if the property only works with optimistic rent, the rehab budget is not verified, the investor is borrowing reserves instead of holding reserves, or the plan depends on short-term money without a long-term payoff path.

Steven Glick,

Director of Mortgage Sales, NMLS #1231769

Final Takeaway

Bridge loans and HELOCs both give investors access to capital, but they solve different problems.

A bridge loan is built for short-term investment-property execution. It fits acquisitions, renovations, repositioning, buy-before-sell situations, and bridge-to-DSCR strategies where the investor already knows the exit.

A HELOC is a flexible credit line against a property you already own. It can work when the line is already open, the acquisition is not rushed, and the investor is comfortable with the collateral risk.

For most investors comparing the two, the better question is not “Which one is cheaper?” It is “Which one matches the deal, the timeline, the collateral risk, and the exit?”

If the property needs time before it can support permanent debt, start by reviewing Ziffy’s bridge loan option. If the property is already rent-ready, run the numbers through the DSCR Loan Calculator and compare whether a DSCR loan is the cleaner path from the start.

Not sure which path fits your deal? Talk to a Ziffy loan specialist before you commit to the acquisition structure.

FAQs

Is a bridge loan better than a HELOC for buying an investment property?

A bridge loan is usually better when the deal is time-sensitive, the property needs repairs or stabilization, or the investor needs financing tied directly to the acquisition. A HELOC can make sense when the line is already open, the investor has strong equity, and the collateral risk is acceptable.

Can I use a bridge loan and then refinance into a DSCR loan?

Yes. That is often the intended path for a buy-renovate-hold strategy. The bridge loan can help with acquisition or stabilization, and the DSCR refinance can become the longer-term rental loan once the property has supportable rent and meets program requirements. Review Ziffy’s DSCR loan requirements before assuming the refinance will work.

Can I use a HELOC for a down payment on an investment property?

Some investors use HELOC funds for down payments, but the full loan structure matters. The borrowed funds can affect reserves, monthly obligations, collateral risk, and the next underwriting decision. You should also confirm whether the lender for the new property allows the source of funds and how the HELOC payment will be counted.

Is HELOC interest deductible if I use it to buy a rental property?

Do not assume it is deductible under home mortgage interest rules. The IRS says home equity loan and HELOC interest is deductible under those rules only if the funds are used to buy, build, or substantially improve the home securing the loan, subject to other requirements.

If the HELOC is used for investment purposes, ask a CPA how the interest should be treated for your specific situation.

Which option is faster?

A bridge loan is designed for fast investment-property execution. Ziffy bridge loans can be approved within 15 days, depending on the file.

A HELOC may be faster only if it is already open and available. A new HELOC application can take longer because it still needs lender review, property valuation, and line approval.

Should I use a bridge loan for a rental property?

Use a bridge loan for a rental property when the asset needs a short-term transition before it can qualify for permanent financing. That could mean renovation, lease-up, title timing, or a delayed refinance.

If the property is already stabilized and rent-supported, a DSCR loan may be the better starting point.

How should I compare the numbers before choosing?

Start with the actual investment property. Review acquisition cost, rehab, closing costs, projected rent, taxes, insurance, HOA dues, reserves, and exit timing.

Then test the deal through Ziffy’s Rental Property ROI Calculator, Cash Flow Calculator, and DSCR Loan Calculator before deciding whether the financing structure supports the deal.

Can a HELOC hurt my DSCR refinance later?

It can. A HELOC draw may add another monthly obligation, reduce available liquidity, or weaken the reserve picture. If your acquisition strategy depends on refinancing into a DSCR loan, model the refinance before drawing heavily from a HELOC.

Is a bridge loan a good option for BRRRR investors?

A bridge loan can work well for a BRRRR-style strategy when the property needs renovation, lease-up, or stabilization before permanent financing. The key is planning the refinance exit before acquisition. If the stabilized rent will not support the DSCR refinance, the investor should know that before closing on the bridge loan.